In March 2026, Vinh Hoan (VHC) exported VND 413 billion to the US market, up 71% year-on-year. For Q1, consolidated revenue reached VND 2,954 billion (up 11%) and net profit after tax came in at VND 285.9 billion, up 35%.MekongAsean VHC shares closed at VND 61,200 on April 29, having accumulated approximately 9% from the VND 55,900 level seen on March 23.

These are genuinely good numbers. But to assess how durable they are, we need to separate the three distinct contributors to that 71% figure: VHC’s company-specific tax position, the sector-wide recovery cycle, and a low base from the same period last year. Each of these drivers has a different shelf life. Valuing the stock against the wrong driver leads to the wrong conclusion.

Three Sources Behind the 71% Growth

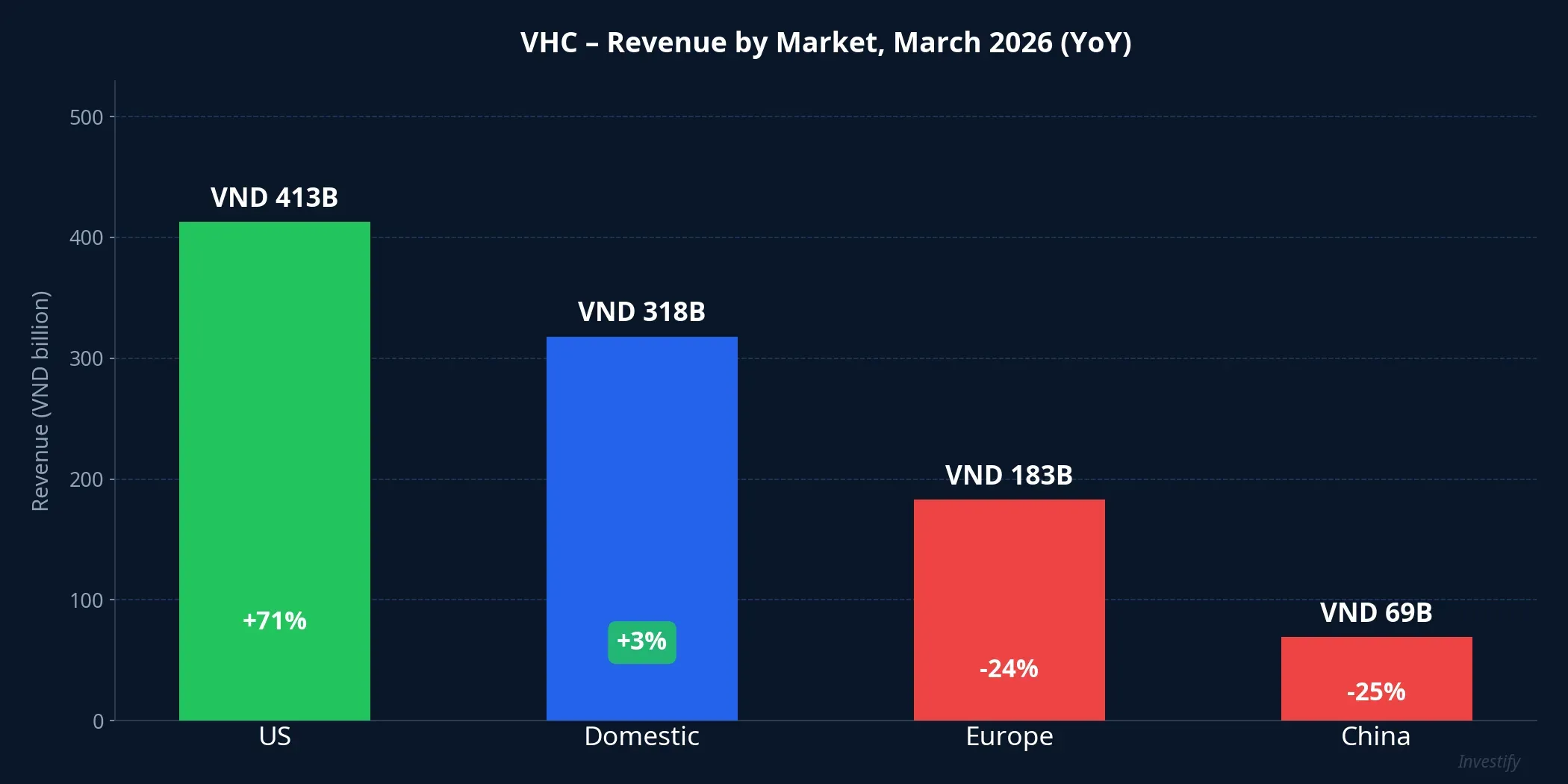

March revenue by market tells the structural story clearly: US VND 413 billion (+71%), domestic VND 318 billion (+3%), Europe VND 183 billion (-24%), China VND 69 billion (-25%). Total March revenue reached VND 1,143 billion, up 12%.MekongAsean The growth is almost entirely US-driven. Europe and China both fell by double digits.

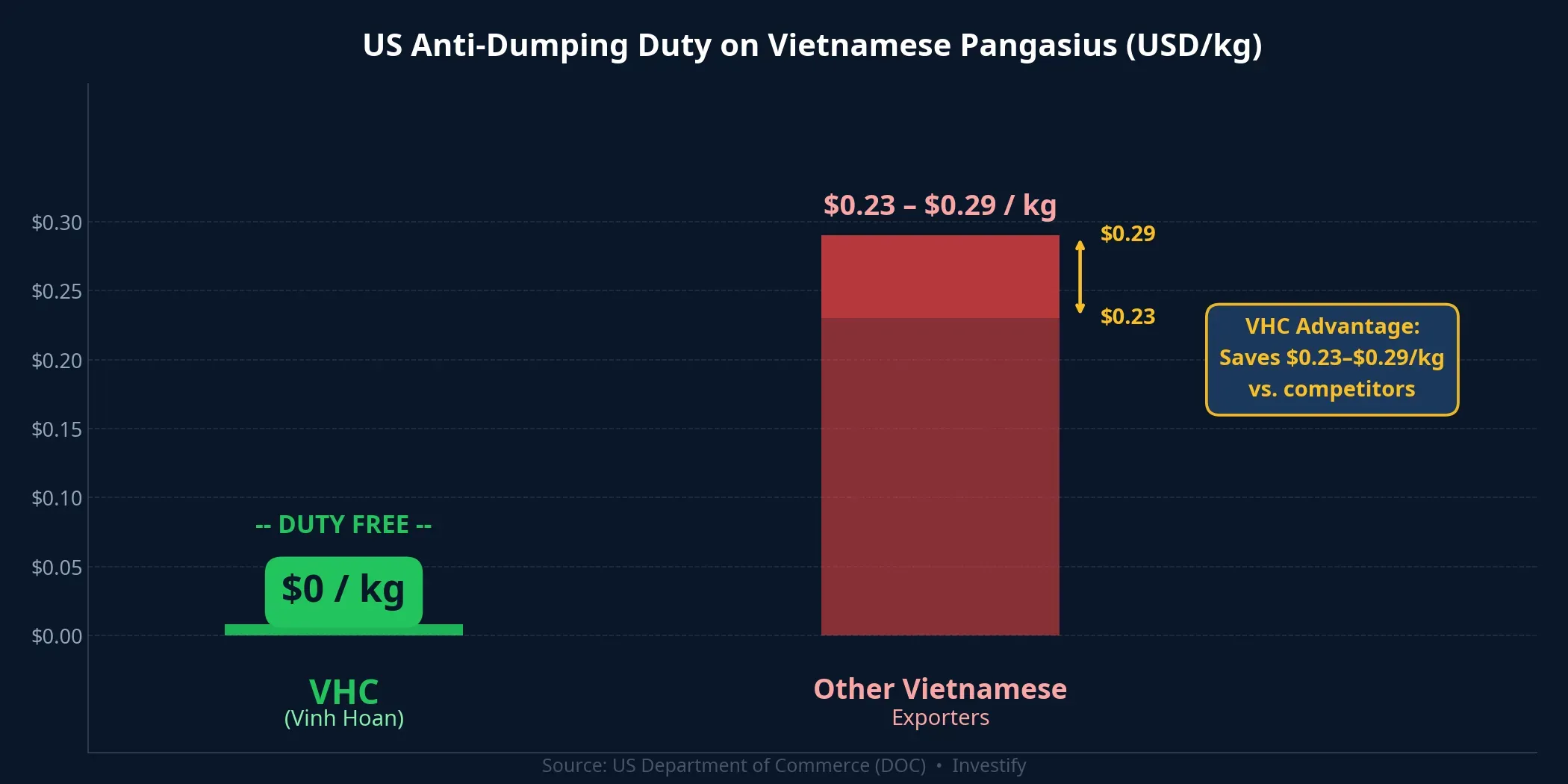

The dominant contributor is VHC’s company-specific tax position. Following the bilateral agreement of January 17, 2025 that resolved the WTO DS536 dispute, VHC was fully relieved of anti-dumping duties with a 0% deposit rate, while most other Vietnamese pangasius exporters still face USD 0.23–0.29 per kilogram.Vietstock This cost gap led US distributors including Walmart, Target, Kroger, and Sysco to shift their sourcing back toward VHC once the new price floor was established in August 2025.

The second contributor is the sector-wide demand recovery. In January 2026, industry-wide pangasius exports to the US grew more than 33% year-on-year. When the sector grows 33% but VHC alone grows 71%, the gap represents VHC’s proprietary “tariff leverage.” Broader demand recovery is a tailwind, but not the primary explanation for the outsized growth.

The third contributor is the low comparison base. In March 2025, after CEO Nguyen Ngo Vi Tam of Vinh Hoan Corporation estimated that US retaliatory tariffs “could negatively impact 15–30% of net profit for 2025,” US orders slowed noticeably.Bao Dau Tu That soft base makes the year-on-year percentage look larger than the absolute growth alone would suggest.

Setting all three side by side: the 71% figure does not reflect structural growth of the US pangasius market. It represents the cumulative effect of a demand recovery cycle combined with a conditional competitive advantage: one tied to the DS536 agreement and the outcome of future administrative review (POR) cycles.

The Tax Advantage: Structural With Conditions

To evaluate the durability of this advantage, a brief look at the 22-year cycle just completed is useful. In 2003, the US Department of Commerce (DOC) imposed anti-dumping duties on Vietnamese pangasius, with a Vietnam-wide rate initially set at 63.88%. Over the following two decades, the order was maintained through annual administrative reviews (POR) and five-year sunset reviews. Vietnam initiated a WTO dispute (DS536) in 2018. By January 2025, a bilateral agreement was reached and VHC’s duties were lifted.

The USD 0.23–0.29/kg gap versus competitors is structural within the scope of the DS536 agreement remaining in effect. However, POR history shows that individual company rates can shift with each review cycle. Furthermore, compliance requirements under the Marine Mammal Protection Act (MMPA) and COA certification standards in the US market continue to tighten. These are variables outside VHC’s control. They warrant monitoring rather than being treated as fixed parameters.

Two Q2 Pressures Building

Not all risks originate in Washington. Two nearer-term pressures are building heading into Q2.

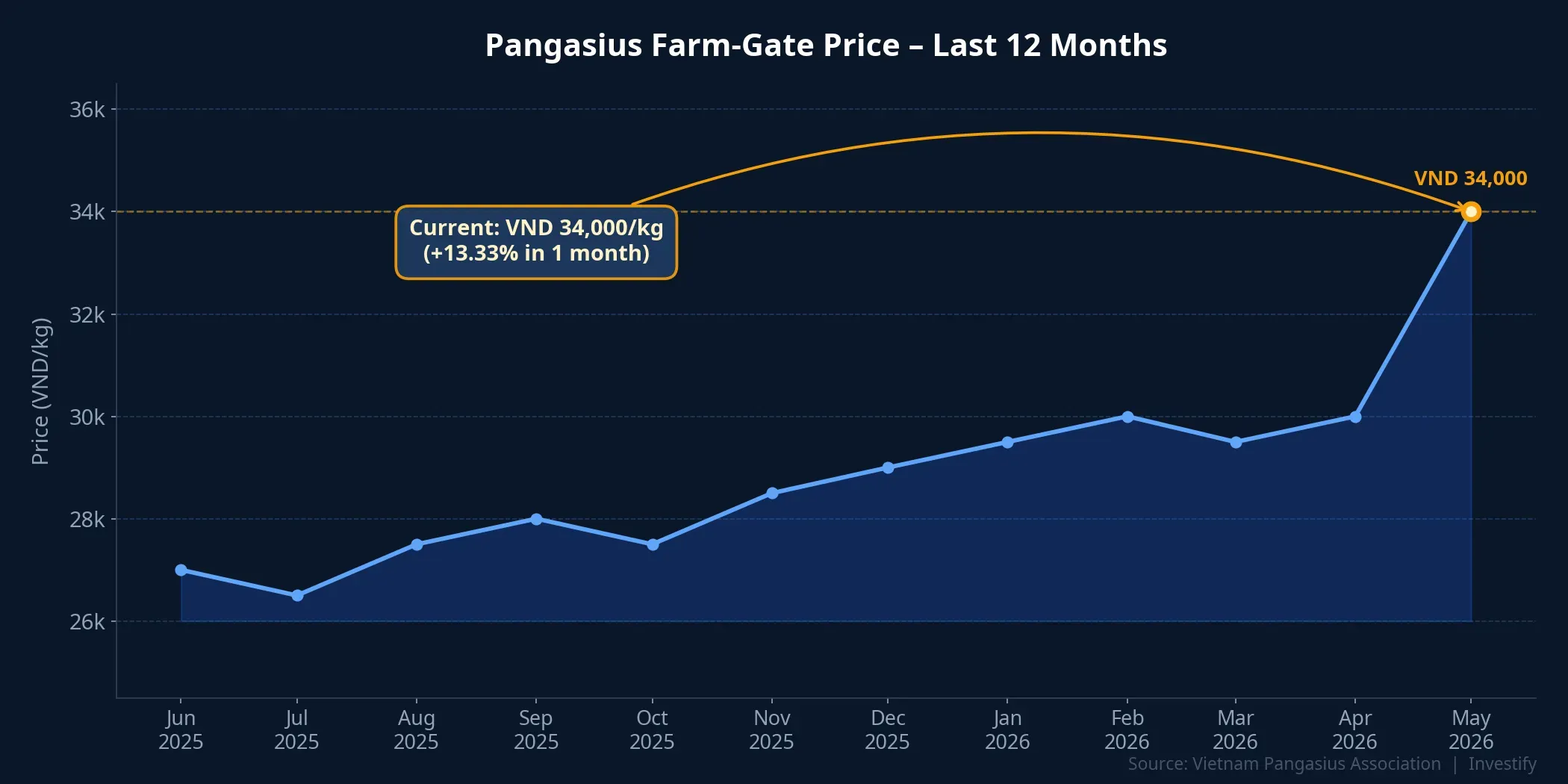

The first is raw material costs. In Dong Thap province, farm-gate pangasius prices have risen to VND 34,000/kg, up 13.33% over one month and 17.24% over three months. A slow restocking cycle has left a shortage of harvest-ready fish, pushing prices sharply higher.

Gross margin for Q1/2026 reached 14.56%, up from 12.69% in Q1/2025.Vietstock What deserves attention is that Q1 margin improvement was recorded before raw material prices surged to current levels. If input costs remain around VND 34,000/kg through Q2 without a corresponding rise in selling prices, gross margin could compress. VHC operates a higher degree of self-supply than most competitors, but is not fully insulated from market-price fluctuations in pangasius.

The second pressure is market concentration risk. The US accounts for roughly 32–34% of VHC’s annual export revenue; for pangasius fillet specifically, the share reportedly reached 54.2% in 2023 according to BVSC data.Bao Dau Tu When a single market accounts for 32–54% of revenue, any shift in US trade policy directly affects profitability. March data shows this dynamic has not changed: the US gained sharply while Europe fell 24% and China dropped 25%.

An Analytical Framework for Reading the Signals

Looking at the numbers, three monitoring axes stand out.

First, distinguish structural from cyclical advantages. VHC’s 0% duty is structural within the scope of the DS536 agreement, provided no POR reversal occurs. The USD 0.23–0.29/kg gap with competitors is cyclical: it will narrow as rivals adjust their rates through future POR cycles. Pricing in cyclical advantages as if they were structural tends not to hold over time.

Second, track the POR schedule and management signals. In May 2026, VHC management signaled an expectation that the tariff environment will “gradually stabilize” and that the distribution network is adjusting to the new price level.Vietstock A reversal signal from this same source — if one emerges — would likely surface ahead of the broader market.

Third, monitor diversification speed relative to concentration pace. With the US up 71% while Europe fell 24% and China fell 25%, the pace of market diversification is lagging behind the pace of US market concentration. Monthly VHC revenue reports by geography are worth tracking. The goal is not to time entries or exits but to observe whether the revenue distribution structure is improving or deteriorating.

2026 Target Progress and Conclusion

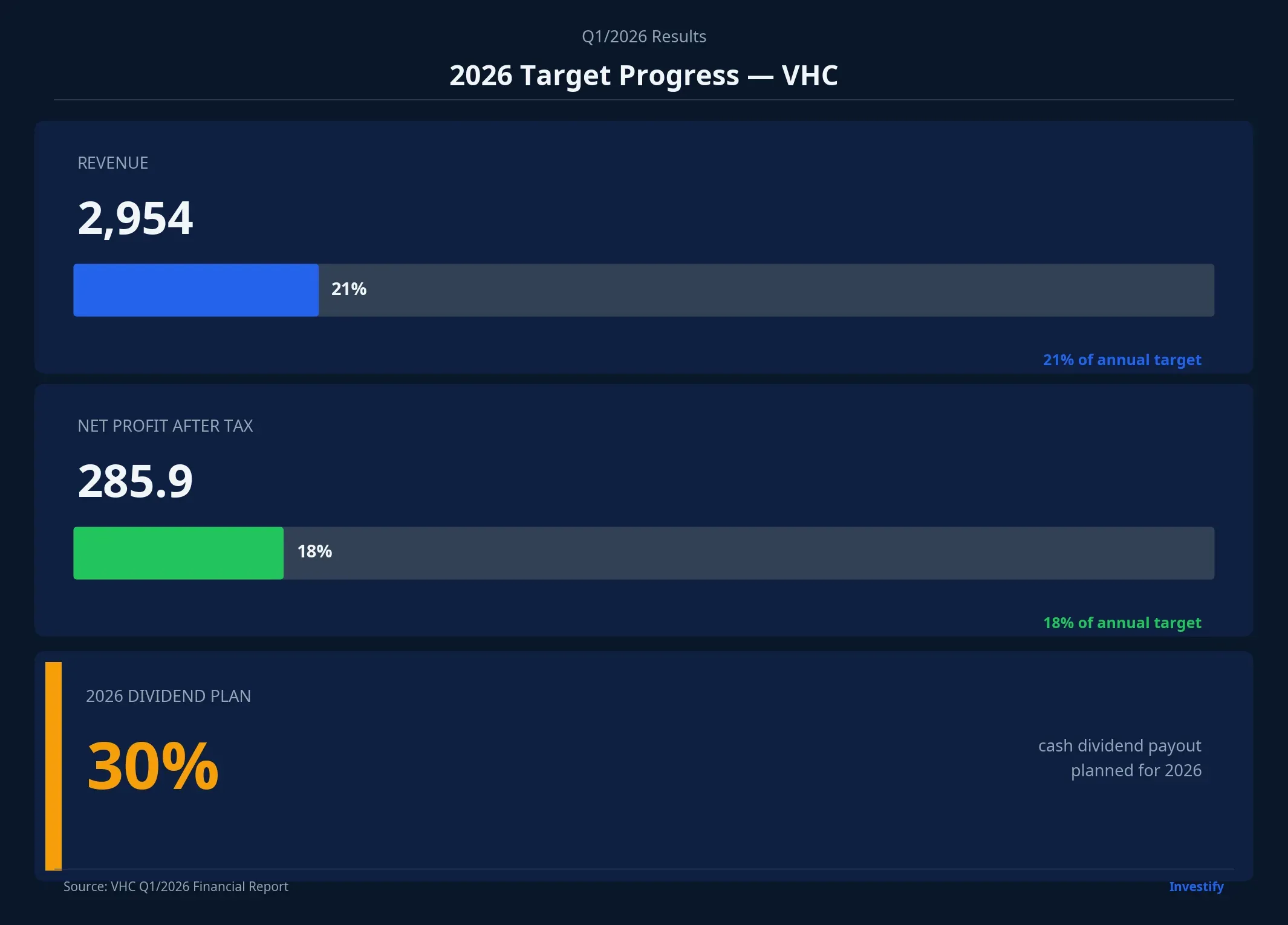

VHC’s full-year 2026 targets are revenue of VND 14,000 billion, net profit after tax of VND 1,600 billion, and a 30% cash dividend.Tin Nhanh Chung Khoan After Q1, the company has completed approximately 21% of its revenue target and around 18% of its profit target. The remaining three quarters will be the real test.

Looking at the data, VHC’s competitive position is currently favorable: zero anti-dumping duty, growing US market share, improved gross margin year-on-year. But the three sources behind the 71% figure carry different time horizons. The DS536 tax advantage will persist as long as POR cycles do not reverse it. The sector recovery cycle will normalize as the industry catches up. The low-base effect was a one-time contribution.

The April revenue report and Q2 results will begin to separate these contributors. The key question is whether US market momentum is sufficient to offset the pressure from rising raw material costs and still-slow diversification into other markets.