On May 1, 2026, Vietnam's new Deposit Insurance Law (Law No. 111/2025/QH15) officially takes effect, replacing the 2012 version entirely.luatvietnam.vn This is a good moment to revisit a widely held assumption: that bank deposits are absolutely safe. The track record of the past 25 years supports that view. But the legal mechanism underneath carries a hard limit that many depositors have not thought through.

How Does Deposit Insurance Actually Work?

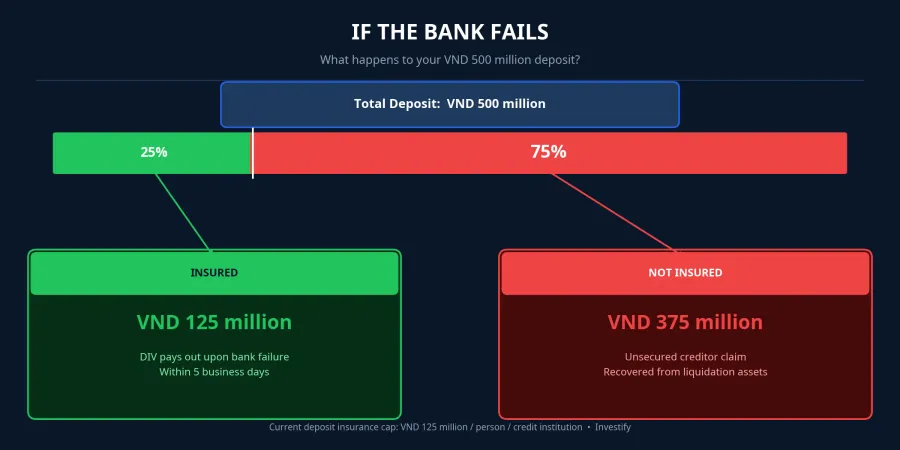

Think of it this way: when you deposit money in a bank, you are a creditor of that bank. If the bank becomes insolvent, the Deposit Insurance of Vietnam (DIV) will pay out a maximum of VND 125 million per person per credit institution, covering both principal and accumulated interest as of the date the obligation arises.thuvienphapluat.vn That payout must happen within 5 business days of receiving complete documentation.

Any amount above VND 125 million is not immediately lost, but it is also no longer insured. That portion becomes an unsecured creditor claim in the bank's liquidation proceedings, ranked alongside ordinary creditors, waiting to be recovered from whatever assets remain. This process can take years, and the recovery rate depends entirely on the actual value of the bank's remaining assets.

One key point: the VND 125 million cap applies per person per credit institution, not per account. If you hold three savings accounts at the same bank totaling VND 300 million, the insurance covers only VND 125 million across all three accounts combined.

Why Has No Depositor Lost Money in 25 Years?

This is an important question, because the answer has nothing to do with the VND 125 million limit. Individual depositors in Vietnam have never had to receive a DIV payout because the State Bank of Vietnam has never allowed a bank to actually go bankrupt. In the cases of CB Bank, OceanBank, GPBank, and DongA Bank, the SBV applied special oversight and then mandatory transfer to a capable bank. All obligations to depositors were assumed by the receiving institution. The VND 125 million payout mechanism has never been triggered.

This approach protected depositors effectively, but it carries costs. The receiving bank has to absorb the failing bank's obligations and bad assets, and these costs spread indirectly across the system. Law 111/2025 does not erase that history, but it introduces a new design: DIV gains an expanded role in supporting the resolution of weak credit institutions, and the triggers for activating deposit insurance payouts no longer depend solely on a formal bankruptcy declaration. Going forward, the scenario in which depositors actually receive exactly VND 125 million from DIV is more plausible by design than it was before.

The Most Significant Change in Law 111/2025

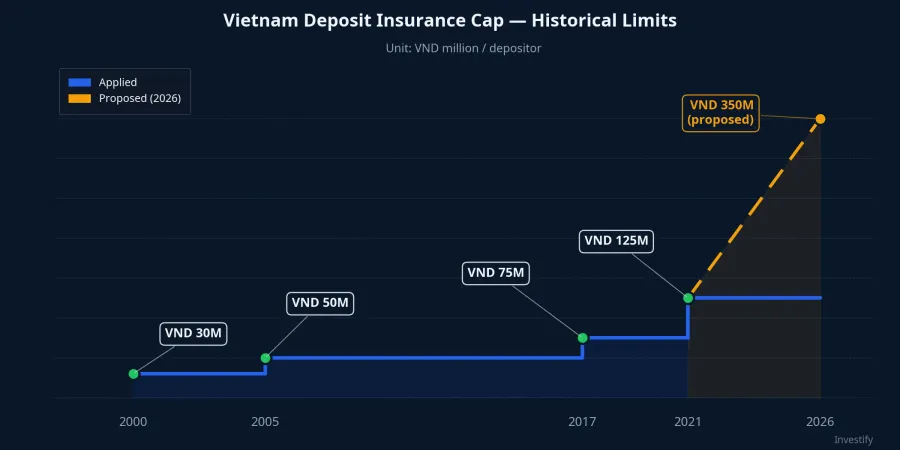

The most important shift is not the VND 125 million figure, nor the expansion of DIV's mandate. It is the power to adjust the coverage limit. Under the 2012 Law, every adjustment to the payout ceiling required a Prime Minister's Decision: a slow and rigid process. Under the 2025 Law, the Governor of the State Bank is empowered to set the coverage limit for each period, based on total deposit volumes, average per-capita income, the fund's financial capacity, and systemic stability requirements.luatvietnam.vn In exceptional circumstances, the limit can be raised to match the full deposit amount.

Speed of response is the most valuable asset any deposit insurance system can have in a crisis. The collapse of Silicon Valley Bank in March 2023 showed that regulators need to make decisions in hours, not weeks. Vietnam has now equipped itself with the same type of rapid-response tool.

The VND 350 Million Proposal: Where Does It Stand?

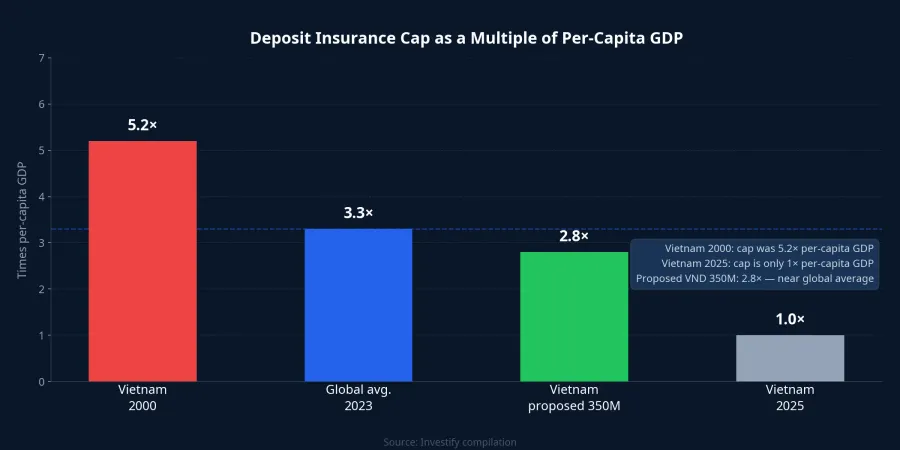

The Deposit Insurance of Vietnam has formally recommended raising the payout cap from VND 125 million to VND 350 million, a 2.8-fold increase.vietnamplus.vn The core argument: between 2000 and 2025, the insurance cap increased 4.16-fold (from VND 30 million to VND 125 million), while per-capita GDP grew roughly 22-fold over the same period. The ratio of the cap to per-capita GDP fell from 5.2 times in 2000 to just 1.0 time in 2025, compared to a global average of 3.3 times in 2023. Raising the cap to VND 350 million would bring that ratio to approximately 2.8 times, closer to international norms.

Currently, according to DIV's analysis, approximately 93.68% of depositors in the system are fully covered by the existing limit.thanhnien.vn However, the share of total deposit value that is fully insured is only around 19.06%. Most depositors are already protected; the gap is in deposit value, concentrated among higher-balance depositors. Raising the cap addresses precisely this gap.

VND 350 million is a proposal, not a final decision. The key difference from all previous cap adjustments: the path forward no longer runs through the National Assembly. Now that Law 111/2025 has delegated the authority to the SBV Governor, the remaining question is when the DIV fund is ready to absorb the higher potential liability.

Where Vietnam Stands Regionally

For context: the US Federal Deposit Insurance Corporation (FDIC) covers up to USD 250,000 (approximately VND 6.25 billion) per account. Singapore insures up to SGD 75,000 (approximately VND 1.4 billion). Thailand covers up to THB 1 million (approximately VND 720 million). Vietnam currently sits at VND 125 million, equivalent to roughly USD 4,750.

The absolute gap looks large, but the fair comparison is the cap as a multiple of per-capita GDP in each country. By that measure, Vietnam currently sits at the bottom of the group shown.

How Should You Think About Allocating Your Savings?

Understanding the actual mechanics leads to more grounded decisions than relying on a general sense of safety.

If your total savings at a single bank are below VND 125 million, the current insurance system covers you fully. You can choose a bank based purely on interest rates, app quality, or convenience.

If your total savings fall between VND 125 million and a few hundred million, spreading deposits across multiple banks so that each institution holds less than the cap is a straightforward hedge. Interest rates on the same tenor tend not to vary dramatically between state-owned commercial banks, so splitting accounts does not meaningfully reduce your interest income.

If your savings run into the billions of dong, spreading across banks is still necessary but not sufficient. At that scale, it makes sense to consider allocating a portion to asset classes with different risk structures: government bond funds, fixed-income products. The goal is not to avoid banks, but to avoid having your entire wealth dependent on the health of any single financial institution.

One more layer worth noting: deposit safety is not only a question about bank failure risk. At current savings rates, the real return after inflation is relatively thin. Bank deposits protect nominal capital well. Protecting real purchasing power over the long term typically requires additional asset layers.

Two Signals Worth Watching

Law 111/2025 sets the legal framework and creates the tools. Two specific developments are worth tracking in the coming months: first, when the SBV Governor issues a formal decision on a new coverage limit: the question is no longer whether a change will happen but when the DIV fund is financially ready to absorb the expanded liability; second, whether the insurance premium rate of 0.15% per year is adjusted at the same time, because keeping the premium flat while raising the cap 2.8-fold raises legitimate questions about the fund's long-run balance.

The belief that "bank deposits are absolutely safe" has held up factually for 25 years. But that track record reflects how the SBV has handled weak banks, not the VND 125 million insurance limit. Understanding the distinction helps you place money more intelligently in the banking system, not less.