Three events unfolded in the first four months of 2026, each reported by the press as a standalone story. Placed in sequence, the picture reads differently: the Vietnam Debt and Asset Trading Corporation (DATC), under the Ministry of Finance, waived approximately VND 1,534 billion in interest owed by Hoang Anh Gia Lai (HAG) on the HAGLBOND16.26 note. In the same Q1/2026 reporting period, HAG disclosed net profit after tax of approximately VND 1,172 billion, up 250% year-on-year.Nguoi Quan Sat Then on April 29, 2026, HAG closed a successful VND 2,000 billion bond issuance, the HAG12601 note, with a 36-month tenor.Mekong ASEAN

What the headline earnings figure does not spell out: the accounting interest waiver alone is larger than a full quarter of net profit. That is the starting point for reading the +250% figure accurately, and for any investor deciding whether HAG12601 belongs in their portfolio.

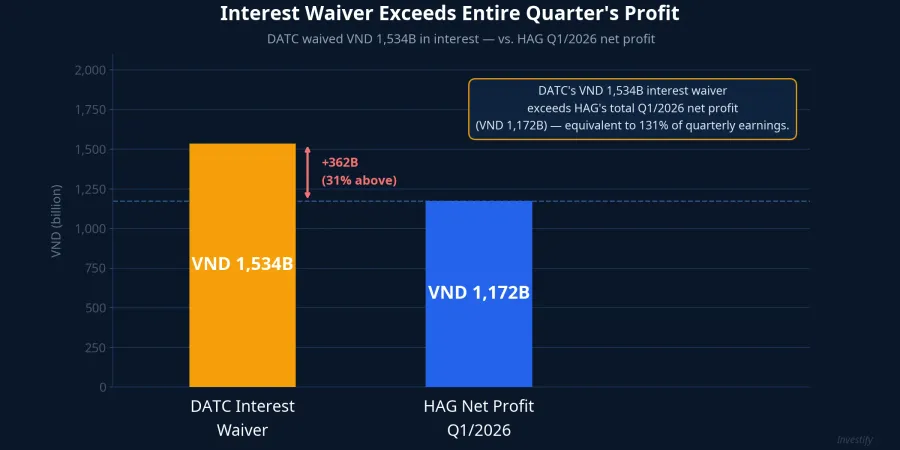

Separating the Accounting Gain from Operating Earnings

The driver behind Q1/2026's profit surge is a sharp reduction in financial costs. The approximately VND 1,534 billion interest waiver from DATC was recognized as a benefit in the period: a charge that would otherwise have been incurred was instead reversed into income. When reported net profit of approximately VND 1,172 billion is itself smaller than the VND 1,534 billion accounting entry, most of the 250% growth comes from this single non-recurring item, not from the fruit or livestock businesses.

HAG's core operations are still running. Fruit revenue in Q1/2026 exceeded VND 1,314 billion, accounting for nearly 74% of total net revenue of approximately VND 1,784 billion.Nguoi Quan Sat Banana and durian remain the core. Livestock revenue declined year-on-year. Coffee has not yet reached large-scale commercial harvest because most of the planted area was established in 2025–2026 and requires approximately three more years before the first commercial crop.

The question investors should ask themselves: strip out the accounting waiver, and what does operating profit look like? The detailed breakdown must wait for the audited consolidated financial statements. But the fact that the interest waiver exceeds total reported net profit is already enough to show that the strong quarterly growth is a one-time event, not a repeatable signal.

Reading the HAG12601 Bond Structure Carefully

Most individual investors stop at "VND 2,000 billion bank-guaranteed bond" and fill in the rest themselves. The real risks are in the details few people read all the way through.

Who can buy directly. HAG12601 was issued through a private placement with a face value of VND 100 million per bond. Under Decree 65/2022, only professional securities investors may purchase directly, a designation that requires a portfolio averaging at least VND 2 billion over 180 consecutive days. Retail investors access it indirectly through bond funds. If you are considering exposure via a fund, the first question to ask the fund manager is whether it holds HAG12601 and at what allocation.

OCB's payment guarantee. This is the most significant structural difference from HAG's previous bond issues. Orient Commercial Bank (OCB) provides an irrevocable, full payment guarantee totaling approximately VND 2,135 billion, covering VND 2,000 billion in principal and approximately VND 135 billion in interest and fees within the tenor.Mekong ASEAN If HAG fails to pay on time, OCB is contractually obligated to step in. The practical implication: investors are taking on OCB's credit risk more than HAG's.

The "A" credit rating: read the footnote. FiinRatings assigned an A rating to this note, published April 25, 2026.DNSE The key detail: the A rating reflects the OCB guarantee mechanism, not HAG's standalone credit quality. FiinRatings is rating OCB's ability to fulfill its guarantee obligation, not whether HAG can repay independently.

No direct physical collateral. OCB's guarantee commitment is the form of security; there is no specific agricultural land or infrastructure pledged. The use-of-proceeds covenant restricts the raised capital to agricultural investment partnerships, specifically the 20,000-hectare coffee project, and prohibits using the funds to restructure existing debt. This covenant is a positive feature that limits the risk of new money repaying old obligations.

The Biological Calendar vs. the Financial Calendar

HAG12601 matures on April 29, 2029. HAG's plan is to use the proceeds to plant approximately 7,000 new hectares of coffee in 2026, targeting a total of 20,000 hectares by 2028.Nguoi Quan Sat Arabica and robusta coffee require approximately three years from planting to first commercial harvest. Trees planted in 2026 would yield their first commercial crop around 2029, roughly coinciding with the bond's maturity date.

The tension is this: the VND 2,000 billion principal repayment in 2029 cannot come from the coffee trees planted with these very proceeds. The first harvest cycle will not yet have stabilized at commercial scale. The repayment must come from one of several other sources: cumulative cash flow from banana and durian over three years, a new bond issuance to refinance, asset disposals, or OCB stepping in under its guarantee obligation. Each scenario carries different implications for investors.

This is not a risk unique to HAG. Any corporate bond that finances a project with a longer payback period than the bond's own tenor carries refinancing risk. But for an issuer with a history of multiple debt restructurings, the question of where the 2029 principal comes from deserves an explicit answer, not one buried inside a coffee farm expansion plan.

Historical Debt Restructuring: Context, Not Verdict

The HAGLBOND16.26 note was issued in late 2016 at a value of nearly VND 6,600 billion. The resolution stretched across nearly a decade: Group A noteholders received gradual repayments from 2024 to 2026; Group B holders exchanged their notes for equity in September 2025; the remaining balance was transferred to DATC in December 2025; and in early 2026, DATC agreed to waive approximately VND 1,534 billion in accrued interest, equivalent to approximately 96% of the accumulated interest on the note.

This history is not a reason to reject HAG12601 outright. But it provides essential context before using "DATC debt cleared" as the sole basis for judging repayment capacity on a new note. HAG12601 operates under a different structure with a different guarantor. The OCB guarantee is a substantive improvement, not just window dressing.

Five Items to Verify Before Drawing Conclusions

The audited consolidated financial statements for Q1/2026 will be published within the coming weeks. That release is the right moment to properly decompose accounting profit from the DATC waiver versus genuine operating earnings from fruit and livestock. Before those numbers arrive, five questions need answered.

First: are you buying directly or accessing indirectly through a bond fund? If through a fund, does the fund publicly disclose holding HAG12601?

Second: what is the final coupon rate per the exchange filing, relative to three-year government bond yields and bank-issued retail bonds?

Third: if OCB is required to execute its guarantee obligation in an adverse scenario, what is the specific timeline and process for investor repayment?

Fourth: if coffee planting runs one year behind schedule, or coffee prices fall 30%, does HAG's cash flow from other segments cover the VND 2,000 billion principal in 2029?

Fifth: what percentage of your total portfolio would this position represent? A standard sizing framework for single-issuer private placement bonds is below 10–15%, even with a bank guarantee. The guarantee reduces principal loss risk but does not eliminate concentration risk or settlement timing risk.

OCB's irrevocable full-payment guarantee is a material structural feature that genuinely distinguishes HAG12601 from HAG's previous bond issues. The right question for investors to ask is not "Is HAG trustworthy?" but rather: "How much OCB credit risk am I taking on, and how does that fit the overall composition of my portfolio?" The most credible answer to that question should wait for the audited financial statements and the full exchange disclosure before reaching a conclusion.