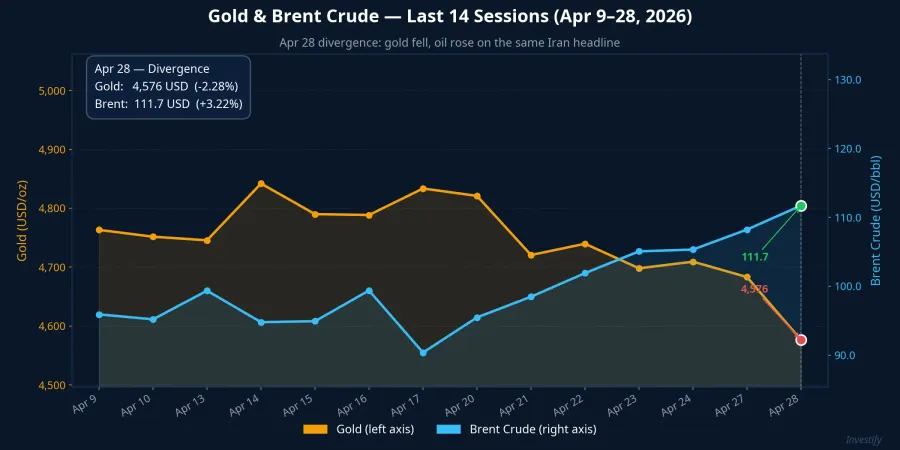

The final trading session before Vietnam's four-day holiday left a notable divergence: gold fell 2.28% to $4,576/oz while Brent crude rose 3.22% to $111.71/barrel — both in response to the same headline. Iran submitted a proposal to reopen the Strait of Hormuz through Pakistani diplomatic channels, deliberately decoupling it from nuclear negotiations.Al Jazeera Same news, opposite reactions. The reason matters more than the numbers.

Why Gold and Oil Read the Same Headline Differently

Gold is a financial asset. It reprices on probabilities — the moment peace odds tick upward, safe-haven capital flows out. Iran's proposal, however incomplete, was enough to shift sentiment. Gold responded instantly.

Oil operates on physical reality. Roughly 20% of global seaborne oil transits the Strait of Hormuz daily. Until tankers actually pass unimpeded, diplomatic language is just paper. The oil market understands this distinction, which is why Brent climbed even as the political news looked superficially encouraging.

Worth noting: Brent has rallied nearly 18% from $94.79 on April 14 to $111.71 today — a sustained move large enough to materially affect Vietnamese oil company earnings in the coming quarters.

Washington's Position: Nuclear Leverage Stays on the Table

Secretary of State Marco Rubio acknowledged Iran's proposal was "better than we thought they would submit" — but quickly made clear that the central issue, preventing Iran from building nuclear weapons, remained completely unaddressed. Rubio described the idea of separating Hormuz from nuclear talks as unacceptable, framing Tehran's offer as an attempt to collect concessions for reopening an international waterway it had no right to close.CNBC

Reuters reporting cited by CNN indicated President Donald Trump was similarly dissatisfied, viewing the proposal as a way to sidestep the nuclear question entirely.CNN

The logic behind Washington's refusal is straightforward: a closed Hormuz is the primary source of leverage over Iran's nuclear calculus. Accepting a decoupled deal means surrendering that leverage in exchange for an incomplete outcome. Neither Trump nor Rubio has shown any inclination to do that.

The result is a structurally designed stalemate. Iran wants to separate the two problems; the U.S. wants to solve them together. The equilibrium holds until one side changes its terms.

How This Splits Vietnamese Oil & Gas Stocks

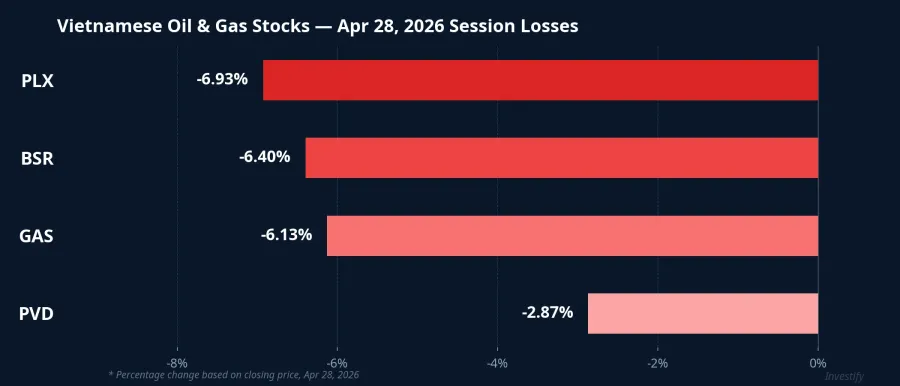

All four major Vietnamese oil stocks fell in the Apr 28 session, but the mechanism differs significantly across names — and those differences matter more than the daily price moves.

PLX fell 6.93% to VND 36,950; BSR dropped 6.40% to VND 23,400; GAS declined 6.13% to VND 73,500; PVD shed 2.87% to VND 30,500. The key insight is not the magnitude of today's losses — it's how each stock would respond under each scenario going forward.

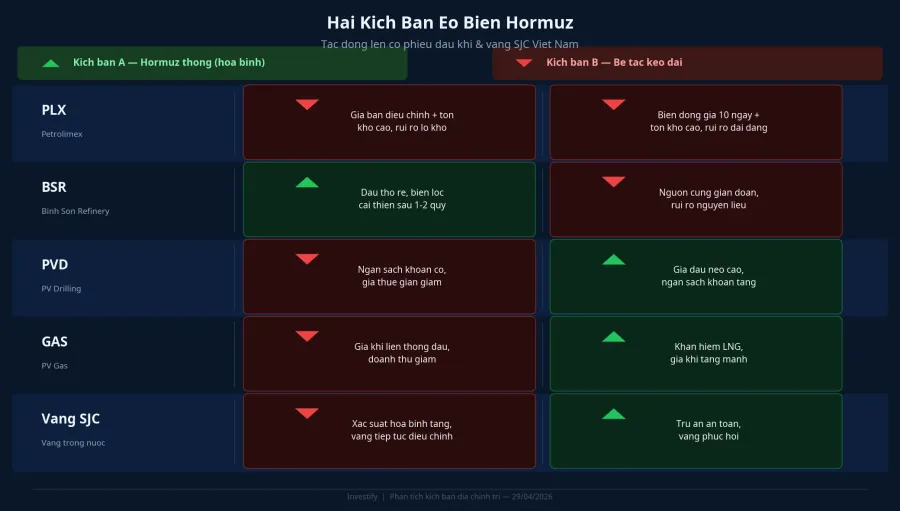

Two Scenarios, Two Different Sets of Winners

Scenario A — Hormuz reopens, oil falls $15–25: PLX and BSR remain under pressure in the near term. Both hold inventory purchased at elevated prices; when the retail price adjusts downward on the 10-day cycle, inventory losses follow. This is the same mechanism that drove Petrolimex to a loss exceeding VND 1 trillion in Q1. BSR has a different long-term trajectory — when crude input costs fall faster than refined product output prices, crack spreads eventually improve, but only after a 1–2 quarter lag. PVD and GAS face the clearest structural headwind here: global drilling budgets contract when oil is cheap, affecting PVD's rig day rates with a 6–12 month delay; GAS's output prices move directly with oil.

Scenario B — Deadlock persists, oil holds $110–120: This is the scenario the market is currently pricing as more likely, given the tone from both Rubio and Trump. In this environment, PVD and GAS benefit structurally — high oil prices sustain exploration budgets and support LNG demand; both names face favorable supply conditions. PLX and BSR face continued inventory cycle risk with every 10-day price adjustment.

The critical takeaway: buying the "oil sector basket" uniformly does not diversify this risk — it concentrates exposure from both directions simultaneously. PLX and BSR move counter to PVD and GAS in Scenario B. The split is not random; it follows directly from upstream vs. downstream positioning.

SJC Gold: Technical Zones to Watch

Vietnam's SJC gold closed at VND 168.8 million/tael on Apr 28, down approximately 3.5% from the month's peak.VietnamNet The move tracks global gold's reaction to the Iran diplomatic signal.

If Scenario A materializes — international gold pulling back toward $4,300–4,400 — SJC may test the VND 162–164 million zone. Under Scenario B's continued deadlock, returning safe-haven demand could push SJC back toward VND 172–175 million. These are the technical reference points for anyone managing gold allocation decisions before the market reopens.

Four Exchange Days Off, Three Signals That Won't Stop

HOSE closes from April 30 through May 3. Three signals will continue moving while the exchange is dark:

The Fed decision drops tonight U.S. time (early morning April 30, Vietnam time). Markets are pricing in over 99% odds of a hold at 3.50–3.75% — the third consecutive pause after March CPI came in at 3.3%.CNBC What matters more is Federal Reserve Chairman Jerome Powell's post-meeting tone: hawkish signaling on future meetings would be an additional headwind for gold; more dovish framing would provide support.

The Rubio and White House messaging track. Language shifts from "unacceptable" to "open to further negotiation" would raise Scenario A probabilities and likely trigger gold recovery alongside oil softness. A hardening of existing language consolidates Scenario B.

Hormuz shipping data. This is the only truly hard signal for oil. If tankers start transiting the strait unimpeded, oil prices will reprice downward materially. If nothing moves on the water, diplomatic statements will keep gold oscillating while oil holds its range.

What to Watch When Markets Reopen May 4

The macro frame is clear: gold has partially priced in a peace scenario; oil has not. This divergence is not a market error — it accurately reflects the different pricing mechanisms of each asset class. Gold moves on probabilities; oil waits for evidence.

When HOSE opens on May 4, the market will need to absorb simultaneously: the Fed decision, the latest Iran negotiation signals, and four days of futures price movement. For investors holding oil sector positions, the PLX/BSR vs. PVD/GAS distinction matters more than correctly predicting which scenario wins. For gold holders near VND 168 million, the 162–164 million and 172–175 million zones are meaningful technical references given the current setup.

The decisive signal is still Hormuz — and that signal only comes from what happens on the water, not from what gets said in press conferences.