In April 2026, FTSE Russell confirmed that Vietnam has met the criteria to be reclassified from Frontier to Secondary Emerging Market, effective September 21, 2026. It is the first time a global index provider has written a specific date into the calendar rather than leaving things at "under review." The question has shifted: no longer "will FTSE upgrade Vietnam?" but "what will Vietnam look like when that date arrives?"LSEG

On the morning of April 29, Prime Minister Lê Minh Hưng chaired a working session with the full leadership of the Ministry of Finance, joined by Deputy Prime Minister Phạm Gia Túc and Deputy Prime Minister Nguyễn Văn Thắng. Finance Minister Ngô Văn Tuấn received a raft of assignments, almost all due in Q2/2026. The signal is unmistakable: the government understands that the window between now and September 21 is the window that counts.CafeF

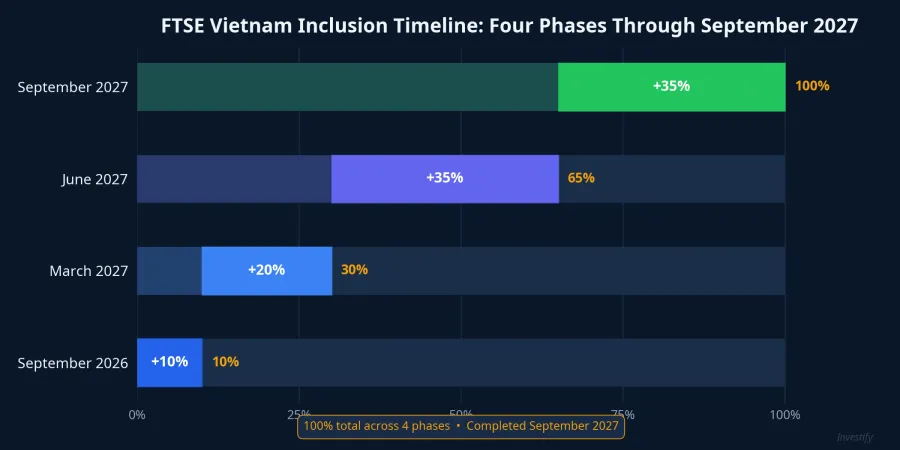

Four Phases and 28 Stocks in the Basket

According to FTSE Russell's published schedule, Vietnam will be added to the FTSE Global Equity Index Series across four phases. The first takes effect on September 21, 2026, allocating 10% of the final index weight. Subsequent phases add 20% (March 2027), 35% (June 2027), and the final 35% (September 2027). The full inclusion process completes exactly one year from the effective date.

Vietnam's final weights across the three index tiers: 0.34% in FTSE Emerging All Cap, 0.22% in FTSE Emerging, and 0.04% in FTSE Global All Cap. The draft basket covers 28 stocks, including large-caps such as HPG, VCB, VIC, VHM, MSN, SAB, VNM, and DXG. The confirmed final list will be published on August 21, 2026.VietnamNews

Capital Flows: Hard Floor Locked, Variable Portion Depends on Reform Signals

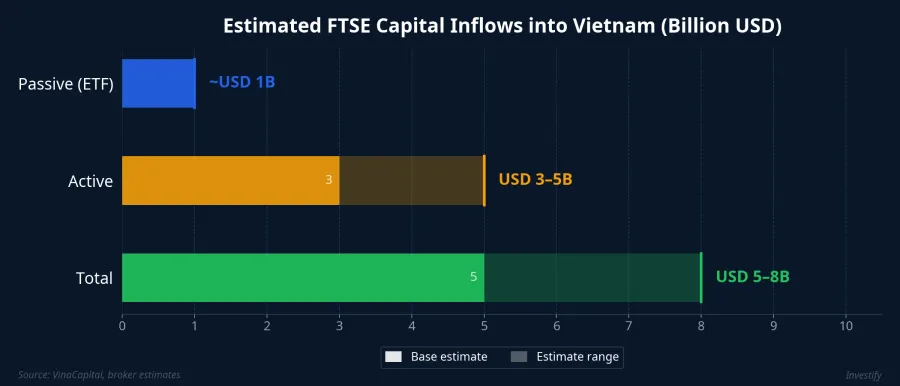

Expected capital flows break into two structurally different buckets. VinaCapital estimates passive ETF inflows at approximately USD 1 billion, with active fund flows running 3–5 times that amount, bringing the total to roughly USD 5–6 billion under a base-case scenario. Several brokerages put the figure higher at USD 6–8 billion, assuming Vietnam's weighting reaches 0.7–1% and active funds deploy capital ahead of the effective date.VinaCapital

The critical distinction is this: the approximately USD 1 billion passive tranche is index-programmed and will arrive automatically on September 21 regardless of domestic reform signals. This is the hard floor. The USD 3–5 billion active tranche is where variance lives. Active managers abroad monitor investment environment signals: reform execution pace, regulatory clarity, and whether Vietnam's corporate bond market reopens to retail investors. The gap between low and high estimates reflects exactly this uncertainty.

Six Tasks for the Finance Ministry, Most Due in Q2

According to reporting from VnEconomy and CafeF, Prime Minister Lê Minh Hưng assigned the Finance Ministry six priority workstreams at the April 29 session.VnEconomy A comprehensive financial market reform plan tied to long-term growth targets through 2045 must be submitted within Q2/2026. Amendments to the corporate bond (TPDN) decree must be finalised in Q2/2026. The legal framework for restructuring SCIC and forming a sovereign wealth fund also carries a Q2 deadline. Classification of state-owned enterprises must be submitted by May 15, and the priority privatisation and divestment plan is expected before the end of May.

These are not isolated items. Two of them, the corporate bond decree and the comprehensive reform plan, directly affect what active foreign funds will see when they evaluate Vietnam ahead of September 21. The corporate bond decree determines whether capital markets open a new fundraising channel for both corporates and retail investors. The reform plan's short-term signal is simpler: does the government follow through on schedule, or does it remain a document of intent?

Three Scenarios Diverging on Reform Pace

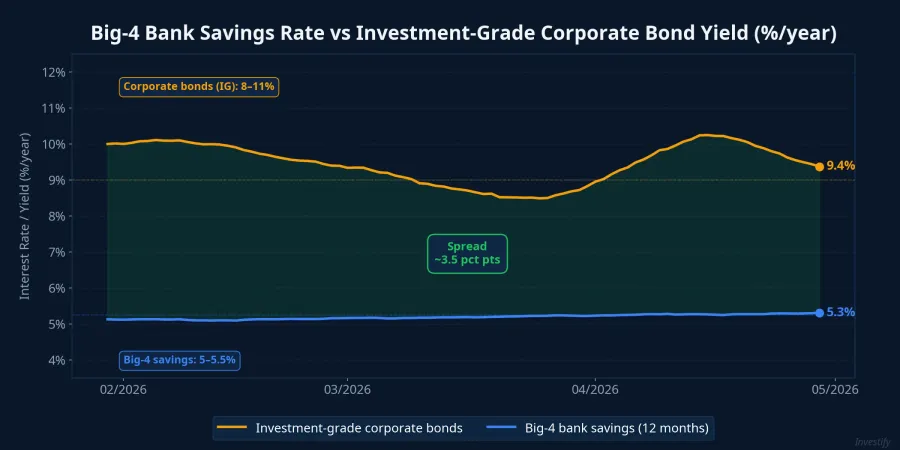

Constructive scenario: The corporate bond decree is revised before July, reopening the private placement market to retail investors under more flexible accreditation standards. SCIC receives its sovereign wealth fund legal framework. The comprehensive reform plan is approved on schedule. The result: active foreign funds enter early in Q3, pushing valuations of the 28-stock basket ahead of September 21. The retail corporate bond channel begins reopening in Q3, filling the yield gap left by Big-4 bank savings rates sitting at 5–5.5% per year for 12-month deposits.

Middle-of-the-road scenario: This is the highest-probability outcome. The comprehensive reform plan and SOE classification meet their deadlines. The corporate bond decree slips into Q3 due to additional consultation rounds. SCIC restructures but capital transfers play out over several quarters in 2027. The equity market absorbs most of the Phase 1 FTSE inflows; the retail corporate bond market remains in a holding pattern through year-end.

Slow-across-the-board scenario: Reforms miss broadly. The passive USD 1 billion still arrives on schedule because that tranche is index-driven and independent of domestic signals. But active managers read the slow-reform signal as an operational risk, trim overweights, and allocate less. Active flows land closer to USD 2–3 billion rather than USD 4–5 billion. Phase 2 (March 2027) and Phase 3 (June 2027) become the next catch-up windows.

One structural note worth highlighting: the corporate bond decree and the comprehensive reform plan are both assigned to the same ministry with the same Q2 deadline. A split outcome (one hits, one misses) is less likely than both hitting or both slipping together.

Four Specific Checkpoints in Q2

Four observable milestones will reveal which scenario is playing out:

Before May 15: The SOE classification decision. This is the technical prerequisite for transferring capital to SCIC under the new fund model. If it extends past this date, the Q2 deadline for the sovereign wealth fund framework becomes hard to hold.

End of May: The Finance Ministry's priority privatisation plan. The publication pace of this report is a real-time indicator of the ministry's execution prioritisation.

June: A public consultation draft of the revised corporate bond decree. If no draft appears before the end of Q2, the deadline almost certainly slips to Q3.

August 21: FTSE publishes the confirmed final basket of 28 stocks. This date is independent of domestic reforms but serves as the pricing reference point for the window between August 21 and September 21.

Asset-Class Implications

For large-cap stocks in the 28-stock basket: passive demand from September 21 is locked in, independent of Q2 reform outcomes. The variable component comes from active flows and shows most clearly in price moves during the August 21–September 21 window after the final basket is announced. VN30 and VN100 ETFs, which hold most of these 28 names, capture this passive demand directly across all four phases.

For corporate bonds: the most reform-dependent asset class. The current "professional investor" threshold requiring VND 2 billion in investment assets held continuously for 180 days is blocking most retail investors from the private placement market. If the revised decree broadens that definition, the 8–11% per annum yield channel could reopen for retail participation, addressing the gap that Big-4 savings rates of 5–5.5% are leaving behind.

For fund certificates and ETFs: indirect but more stable beneficiaries of the FTSE upgrade. Each passive allocation phase lifts valuations across the 28-stock basket, supporting performance in VN30- and VN100-tracking funds. Bond funds hinge on whether the corporate bond decree generates new supply of investment-grade paper.

What to Watch in the Next Two Months

The real variable is not FTSE. It is the Finance Ministry's Q2 execution record. The timeline to September 21 is short enough that delays cannot easily be absorbed, and transparent enough that outcomes are publicly verifiable without needing insider access. The four checkpoints above (May 15, end of May, June, August 21) are all observable through public announcements. Q2/2026 will speak for itself on which scenario is materialising. Active foreign managers are watching exactly the same set of signals.