Some weeks the trading calendar and the global event calendar create an unusually tight gap. The week of April 28 to May 4 is exactly that. Vietnamese investors have just two trading sessions (April 28 and 29) before the market closes for four consecutive days, from April 30 through May 2. In that window, the most consequential market events of the quarter will arrive from the United States.

On the evening of April 29 in US time, Meta, Microsoft, Alphabet and Amazon will simultaneously report Q1 2026 results after the NYSE close.Motley Fool A few hours earlier, the FOMC will announce its rate decision and Fed Chair Jerome Powell will hold a press conference (the final one of his term).Fed Apple follows on April 30 US time. Vietnam's market stays shut throughout. The earliest session where Vietnamese investors can react to any of this is May 4.

The macro picture points to a rare timing mismatch: the quarter's most market-moving catalysts land precisely when Vietnamese investors have no way to adjust in real time. That makes the two sessions on April 28-29 far more than routine trading days. They are the last opportunity to size positions before global information rewrites the landscape.

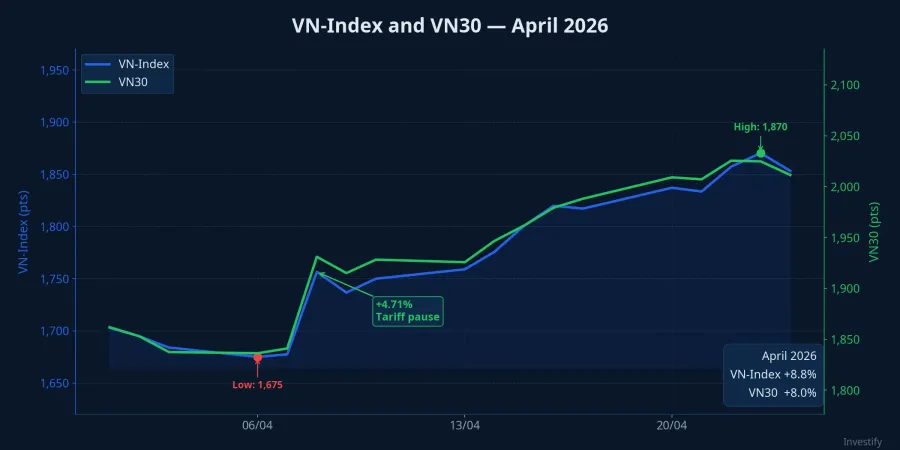

April's Rally: Strong Gains, Approaching Resistance

VN-Index closed April 24 at 1,853.29 points; VN30 at 2,011.42 points, up approximately 8.8% and 8.0% for the month respectively. The rally tracks global sentiment recovery after the tariff-driven volatility earlier in April: on April 8, VN-Index surged 4.71% in a single session when the tariff pause was confirmed. From there, the market climbed steadily through the second half of the month.

Nasdaq closed April 24 at 24,837 points, up roughly 13–15% for the month. That recovery reflects rising expectations for Big Tech earnings.EconCurrents VN-Index's more modest gain versus Nasdaq fits the typical pattern: Vietnam captures the sentiment spillover from the US, but with a smaller amplitude given its different economic structure and capital flows.

Within this picture, FPT stands as the most closely watched domestic proxy. The company reported pre-tax profit for Q1 2026 exceeding 2,804 billion VND, up 16.3%; revenue of 12,480 billion VND; and net profit attributable to parent shareholders of 2,487 billion VND, up 14.4%.BBW Solid fundamentals, but FPT's share price next week will be shaped more by what Big Tech says than by its own numbers.

One key technical point: VN30 has just cleared the 2,000-point level for the first time in this cycle. That level has repeatedly capped previous rallies. With elevated expectations now built in, if global signals are not strong enough to pull fresh capital in, profit-taking pressure will naturally concentrate around this zone.

The Fed: A Foregone Decision, an Open Question on Tone

The CME FedWatch tool assigns 99% probability to the Fed holding rates in the 3.50–3.75% range.Bitcoin News The hold itself is not the variable. The variable is the language of the statement and the tone Powell strikes in the press conference.

Recent Fed communications lean cautious. John Williams, President of the Federal Reserve Bank of New York, warned that energy prices could push inflation above 3%. Christopher Waller, a member of the Fed Board of Governors, said inflation risks now outweigh labor market risks. Continued tariff pressure and elevated oil prices have narrowed the window for early rate cuts; market expectations have shifted the first likely cut to June or later in the year.

Two divergent outcomes emerge from this meeting. If Powell keeps his tone neutral and keeps the June cut option alive, growth and technology stocks continue drawing support from easing expectations. If he instead emphasizes that inflation is not yet under control and drops language suggesting a near-term cut, the market will reprice the timeline. Compressed multiples in the growth segment will follow. The distance between these two scenarios could determine the direction of Nasdaq on April 30 in US time, and by extension VN-Index on May 4.

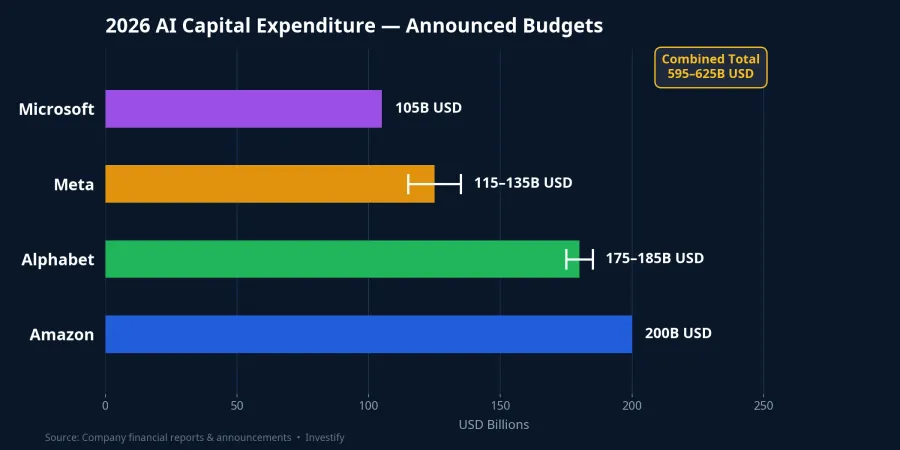

Big Tech: $600 Billion in AI Capex and the Revenue Test

The four companies reporting on April 29 have announced unprecedented AI capital expenditure budgets for 2026: Amazon approximately $200 billion, Alphabet approximately $175–185 billion, Meta approximately $115–135 billion, Microsoft approximately $105 billion.Motley Fool Combined, the four names represent over $595–625 billion in AI infrastructure spending in a single year, a level of investment without precedent.

Analysts have placed expected Mag 7 EPS growth for Q1 2026 at approximately +20.3%, with revenue growth of +22%.Yahoo Finance High expectations mean a narrow margin of safety: a single name missing consensus could trigger a reaction larger than in a typical quarter.

The core question the market is asking is straightforward: is AI revenue growing fast enough this quarter to justify that level of capital spending? The specific metrics are Azure growth (Microsoft), Google Cloud (Alphabet), AWS (Amazon), and Meta's AI-linked advertising revenue. Last quarter, Azure grew 39% but decelerated from the prior quarter, a sign of slowing momentum worth watching.Kraken If that slowdown continues, the narrative that "AI investment is translating into revenue" faces a direct challenge from the earnings data itself.

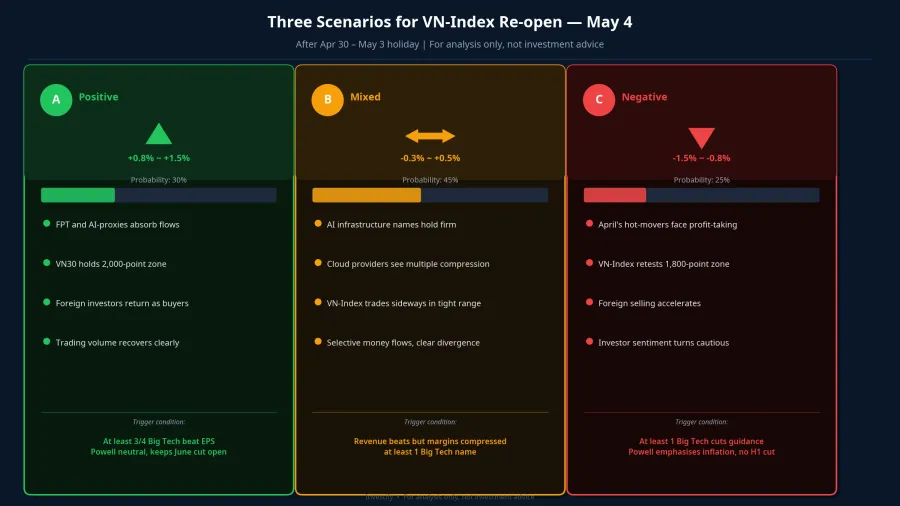

Three Scenarios for the May 4 Market Open

All of the Vietnamese market's reaction to the FOMC decision and Big Tech earnings compresses into the single session on May 4. Three scenarios have clearly differentiated triggers.

Scenario A: Both signals positive. At least 3 of 4 Big Tech names beat EPS consensus, cloud revenue maintains growth above 30%, and Powell keeps a neutral tone without adding new hawkish signals. Result: Nasdaq rises in the April 30 US session, sentiment carries into Asia and Vietnam. Technology stocks, FPT first among them, absorb near-term inflows; VN30 has a basis to hold the 2,000-point zone.

Scenario B: Revenue beats, margins compressed. Cloud divisions accelerate but data center depreciation and energy costs weigh on gross margins; Powell stays neutral. The market diverges sharply: AI infrastructure beneficiaries (chips, servers) hold firm; large cloud providers face multiple compression. VN-Index trades sideways in a narrow range when it reopens May 4; FPT faces a valuation challenge tied to the leading cloud names.

Scenario C: Dual disappointment. At least one major name misses revenue or cuts guidance due to tariff pressures, while Powell stresses that inflation does not yet permit easing in the first half of the year. Result: Nasdaq falls more than 2%, cautious sentiment flows into Asia and Vietnam. April's biggest gainers face concentrated profit-taking; VN-Index risks retesting the 1,800-point zone.

Two Signals to Watch in the April 28-29 Window

During the two pre-holiday sessions, no hard data from the US is available. The two indirect signals worth tracking most closely:

First, foreign investor flows on HOSE. Ahead of major US events, foreign funds typically reduce long positions to cut overnight risk. If net selling accelerates in the April 28-29 sessions, that is a broad defensive signal: the market is already pricing Scenario B or C as more likely than Scenario A, before the holiday even begins.

Second, FPT's price behavior. With Q1 results already reported and solid, if FPT weakens in the pre-holiday sessions despite no negative company-specific news, it signals that the market is pricing risk around Big Tech's forward guidance rather than responding to FPT's own fundamentals.

Portfolio Positioning Before the Four-Day Closure

The distinctive feature of this week is not volatility — it is the timing mismatch. The quarter's most significant catalyst lands precisely when Vietnamese investors cannot react in stages. That justifies deliberately defensive positioning, not panic selling.

For portfolios that have gained 8–12% following April's rally, holding 15–20% cash is a reasonable defensive buffer when indices approach resistance and a long closure blocks the ability to respond in real time. Reducing exposure in April's hottest movers, particularly AI-proxy names, back to portfolio-average weights is appropriate. Specific decisions depend on entry price and profit margin for each position.

The practical test: if May 4 opens into Scenario C, can the current portfolio absorb that without being forced into panic selling? Working through that question before April 29's close is the most important task of the week.

Signals to monitor after the holiday: Azure and AWS growth rates versus last quarter; the precise language of the FOMC statement on the rate path; and how FPT trades in the opening session on May 4. Those three data points together will clarify the picture far better than any pre-holiday forecast.