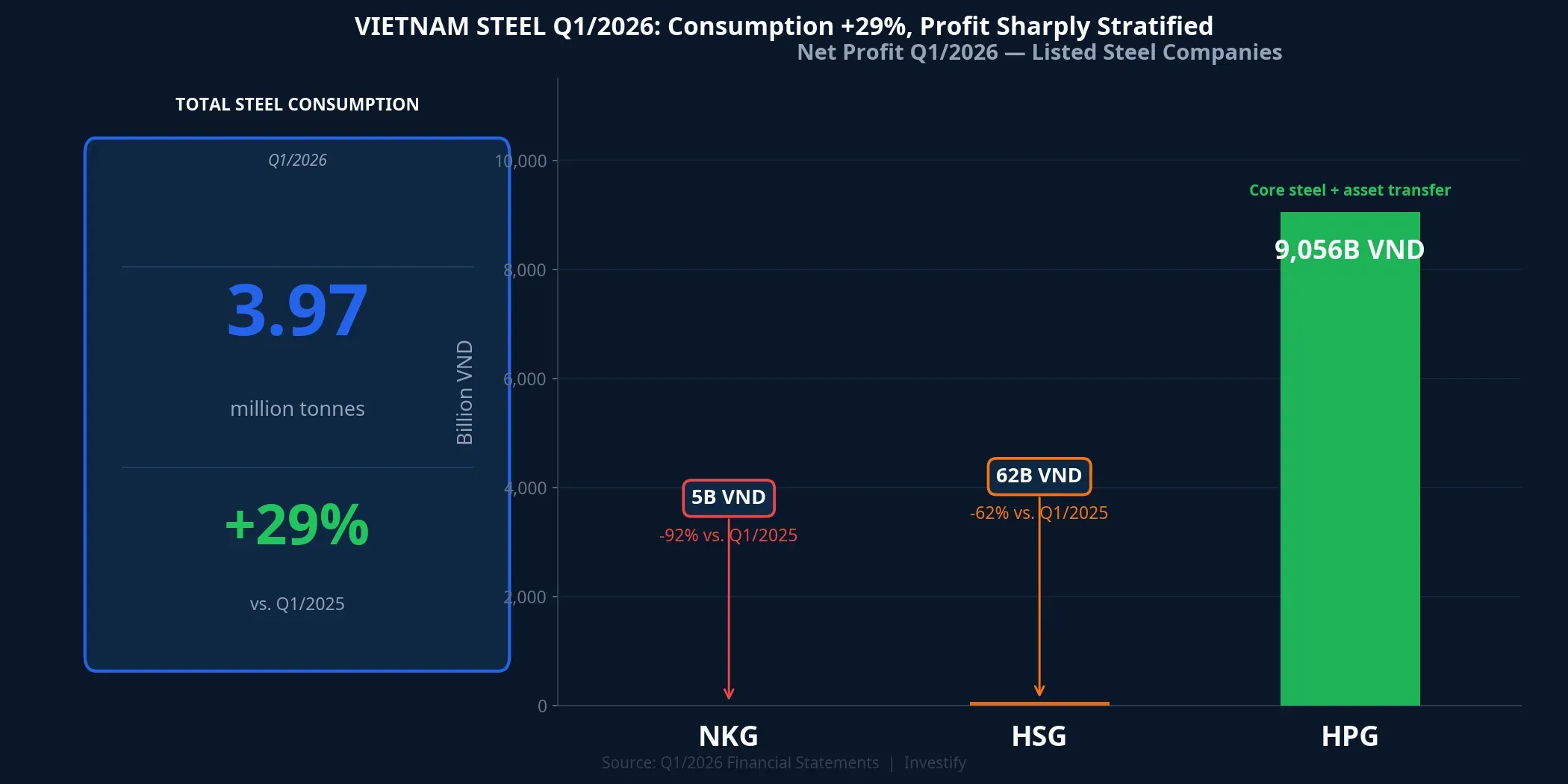

Vietnam’s steel market consumed 3.97 million tonnes in Q1/2026 — the highest figure in a decade, up 29% year-on-year, with domestic production reaching 3.73 million tonnes (+24.1%).DanViet On the surface, it looked like a strong recovery quarter for the entire industry. But when you set the sector-level figure beside the individual company results, the picture becomes far more complicated: Hoa Phat Group (HPG) posted net profit of 9,056 billion VND, while Hoa Sen (HSG) recorded just 62 billion VND and Nam Kim (NKG) barely crossed the 5-billion mark by one estimate. This is not a story of individual company luck — it is the outcome of two structurally different market positions operating in the same quarter.

A Clear Earnings Divergence

First, a necessary clarification: the 3.97 million tonne figure and the 29% growth rate measure consumption volume, not profit. The largest driver of that volume was construction steel — a product that benefits directly from infrastructure project disbursements and a post-Tet recovery in residential construction. In March 2026 alone, construction steel sales ran approximately 1.5 times the prior month’s volume, fueled by pre-price-movement stockpiling and an early-year push in public infrastructure spending.StockBiz

The aggregate number obscures a deep split at the company level. HPG delivered 9,056 billion VND in net profit, of which approximately 5,200 billion came from its core steel operations (construction steel and HRC) and approximately 3,800 billion from the transfer of the Pho Noi real estate project. Sales volume reached roughly 3 million tonnes, with the domestic market accounting for around 80% of the mix. At the other end of the spectrum, HSG posted 62 billion VND in net profit for its fiscal Q1 2025–2026 (October–December 2025), down 62.3% year-on-year.Thuong hieu Cong luan According to VCBS estimates, NKG earned approximately 5 billion VND in Q1/2026, a roughly 92.4% decline on revenue of around 3,081 billion VND — the deepest single-quarter drop since 2023.Nguoi Quan Sat

HPG: Right Product, Right Market

What stands out in HPG’s results is not just the size of the profit number — it is the structural logic behind it. Hoa Phat did not get lucky with product mix. Over many years the group built a fully vertically integrated model spanning iron ore to finished long steel and HRC, through to downstream products (steel pipes, coated sheet) sold domestically. With roughly 80% of output going to domestic customers — infrastructure contractors, pipe manufacturers, and domestic coated steel producers — every acceleration in public capital disbursement translates directly into HPG order books.

Nguyen Viet Thang, CEO of Hoa Phat Group (HPG), stated at the annual shareholders’ meeting on April 22 that construction steel demand is likely to remain positive through at least the end of Q2/2026, supported by continued infrastructure project disbursements.VietnamBiz HPG closed at 27,900 VND per share on April 26, reflecting the market’s relatively clearer view on the domestic demand narrative compared to the two export-facing names.

Coated Steel: Caught in a Two-Way Squeeze

NKG and HSG both carry high export exposure — and that is the structural root of their Q1/2026 problem. When export demand weakened, neither company had sufficient domestic demand to offset the shortfall, because coated sheet and galvanised products are not the primary materials for basic infrastructure construction. HSG’s Q1 results illustrate the mechanics clearly: net revenue fell 17–18%, gross margin compressed from approximately 11.8% to around 11.2% as lower volume spread fixed costs across fewer tonnes, and interest expense rose roughly 6% in line with higher lending rates.

Two structural forces are pressing simultaneously on this group.

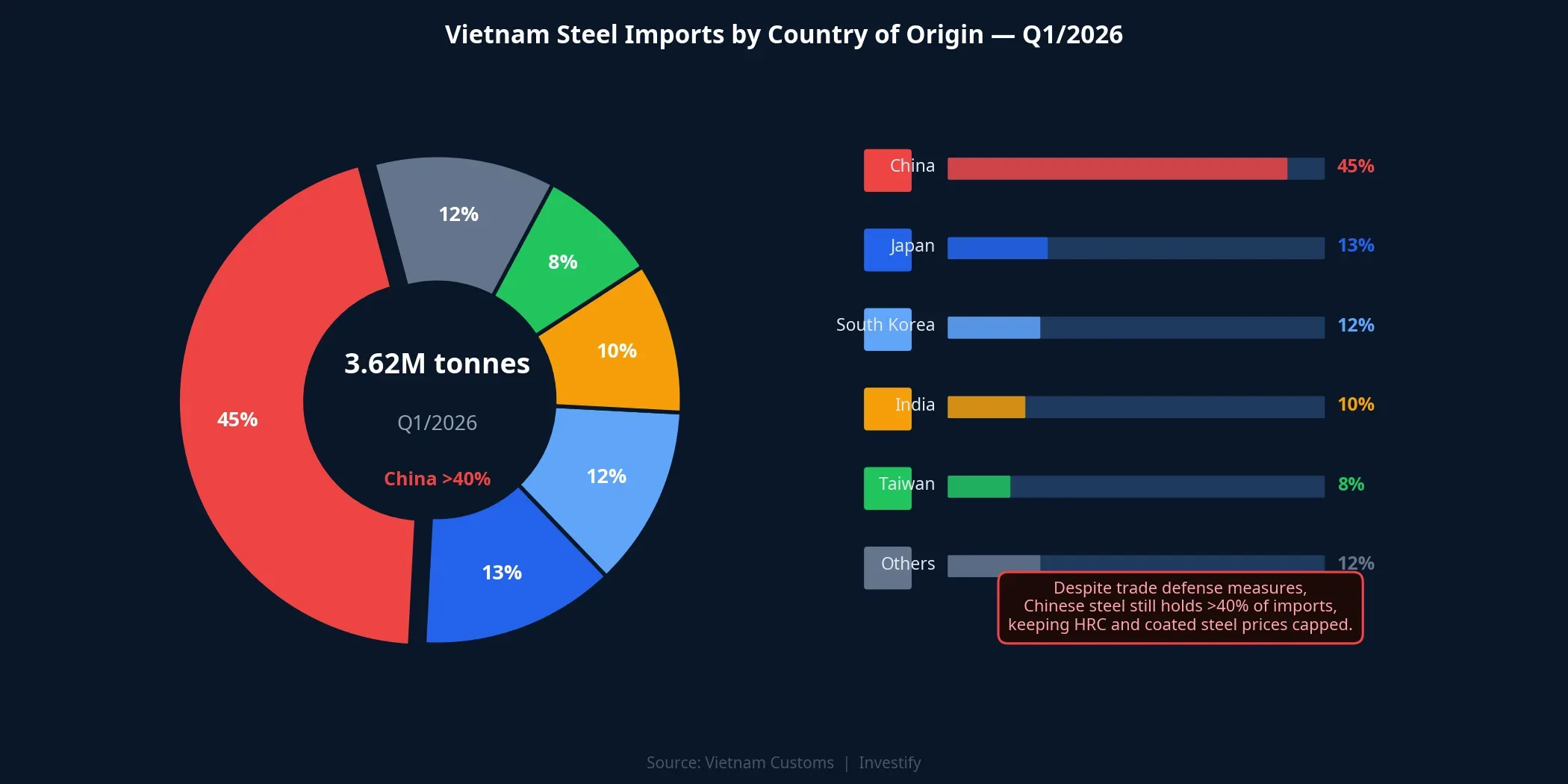

The first is cheap Chinese steel on the domestic market. In Q1/2026, Vietnam imported approximately 3.62 million tonnes of steel products, with China accounting for more than 40% of the total at an average import price of around 490 USD per tonne.Bao Van Hoa While trade defense measures have moderated peak import volumes, the Chinese supply overhang remains large enough to cap domestic HRC and coated steel prices — preventing gross margins from recovering even as sector volumes improve.

The second is the EU Carbon Border Adjustment Mechanism (CBAM) at the export end. The EU began applying CBAM fully to the steel sector in 2026.Tai chinh Doanh nghiep Vietnam’s average steel emission intensity stands at approximately 2.51 tonnes of CO₂ per tonne of crude steel, above the global average. At a EU carbon price of 50–100 EUR per tonne of CO₂, every tonne of steel exported to Europe could face roughly 20–30% additional cost. This is not a short-lived disruption: CBAM will intensify progressively as free-allocation allowances for EU producers are phased out through 2034, making it a structurally rising barrier rather than a one-time adjustment.

Are There Other Explanations?

The evidence points to export structure as the primary driver — but two additional factors compounded the pressure and should be acknowledged.

The first is rising HRC input costs in Q1/2026. Rising HRC prices are positive for HPG as a producer of HRC, but negative for coated steel makers who consume HRC as raw material. When HRC costs rise while finished product prices are capped by Chinese import competition, NKG and HSG get compressed on both the input and output side simultaneously. The second is fixed-cost dilution: HSG rebalanced its sales mix toward the domestic market (to approximately 75% of volume), but domestic coated steel prices are also capped by Chinese competition, so the channel shift did not meaningfully improve margins.

That said, the data points most strongly to export structure as the primary cause. The 50%-plus drop in HSG’s export volume in the same period coincides precisely with the steepest profit decline since 2023. Rising HRC prices and higher interest costs are amplifying factors, but neither alone would explain a 92% profit collapse at NKG or a 62% collapse at HSG.

Q2/2026: Which Group Has Clearer Visibility?

Domestic construction steel — led by HPG — has relatively clear positive momentum for at least Q2/2026, as outlined by Nguyen Viet Thang at the annual meeting. Continued public capital disbursements and major infrastructure projects remain the strongest near-term demand drivers.

Coated steel recovery depends on three conditions that remain uncertain: whether alternative export markets outside the EU (Southeast Asia, the Middle East, the US) can absorb Vietnamese product at prices sufficient to cover CBAM costs; whether HRC input costs moderate as global iron ore demand softens; and whether domestic trade defense measures effectively limit continued Chinese low-price penetration. NKG has set a pre-tax profit target of 400 billion VND for full-year 2026, approximately 66% higher than 2025 — but if Q1 came in at roughly 5 billion VND by current estimates, the entire recovery burden falls on the second half of the year, contingent on the Phu My plant ramping up output. NKG traded at 14,450 VND per share and HSG at 15,800 VND per share at the close on April 26, reflecting subdued recovery expectations from the market.

Reading Earnings Season by Layer

The most important signal in Q1/2026 earnings is not the 29% sector consumption growth — it is the depth of the stratification underneath that number. In the same quarter, in the same industry, HPG and NKG sit at opposite poles of the profit cycle. The cause is structural, not coincidental: the domestic steel group has near-term visibility driven by public investment; the export-oriented coated steel group faces two structural headwinds that are both intensifying.

This divergence is likely to persist until at least one of two conditions changes: coated steel exports find an alternative market at prices that cover CBAM costs, or Chinese import prices rise enough to allow domestic coated steel margins to recover. The key indicators to watch over the next two quarters are NKG and HSG Q2 results, export order data, and EU carbon price movements. These figures will determine whether the coated steel group has already reached the bottom of this cycle or still has further ground to give.