Between 9 September 2025 and 27 March 2026, three legal documents and one shortlist round assembled a near-complete framework for Vietnam’s crypto-asset market. Resolution 05/2025/NQ-CP opened a five-year pilot. Circular 32/2026/TT-BTC imposed a 0.1% transfer tax on individuals — exactly the rate currently applied to listed equities on HOSE/HNX. Five exchange applications cleared the shortlist and now await final licensing, with a Q3/2026 pilot launch as the official target.

What stands out is that these three pieces did not arrive in the usual sequence — Resolution first, guidance second, operators last — but in parallel. When the Ministry of Finance issued the tax circular on 27 March 2026, the five exchange applications had already been put out for cross-ministry review just two weeks earlier through Letter 2921/BTC-UBCK dated 12 March 2026.VietnamNet The tax framework and the market-organisation framework arrived almost simultaneously — a sequencing Vietnam typically does not follow for new markets.

Piece one: a five-year pilot and the choice of supervised liberalisation

Resolution 05/2025/NQ-CP, signed by Deputy Prime Minister Hồ Đức Phớc and effective 9 September 2025, established a five-year pilot.Government Portal The intent was not to redefine crypto-assets but to grant a supervised operating window: only licensed entities may issue, organise trading venues, or provide services. Everything outside that window — peer-to-peer trades, unregistered foreign exchanges, self-custody wallets — remains beyond the pilot’s scope.

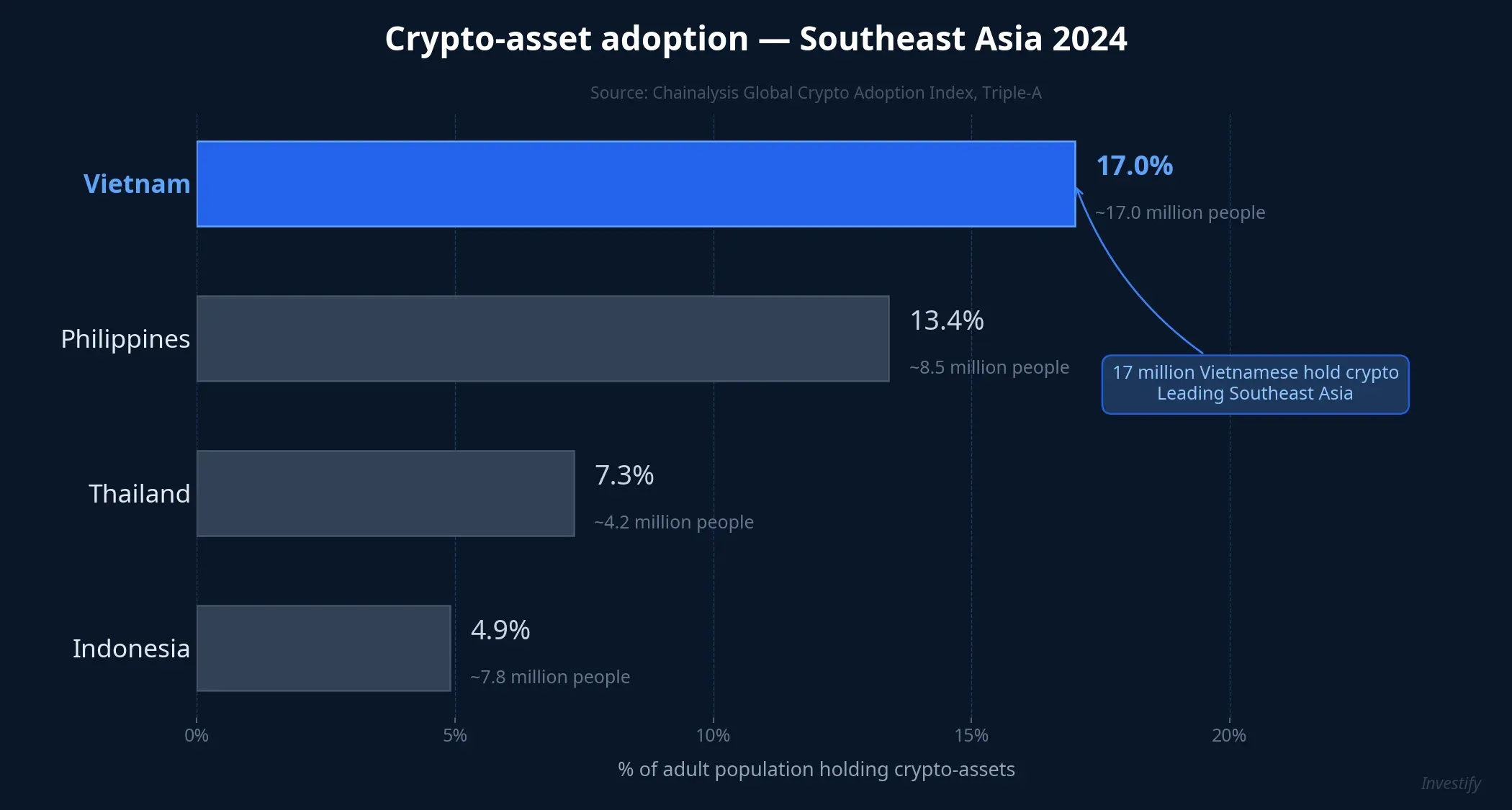

The choice reflects a hard reality. Roughly 17 million Vietnamese hold crypto-assets, the majority via foreign exchanges such as Binance, OKX, and Bybit. An outright ban is not feasible. Yet leaving the market to itself makes it harder for Vietnam to meet FATF recommendations on anti-money-laundering and customer due diligence — a barrier to the country’s ambition to exit the grey list. The pilot threads the middle: legalise a supervised channel and let the unsupervised channel shrink as domestic exchanges deliver liquidity and compliance.

The 17-million figure is not an abstract number. It is larger than the combined population of Ho Chi Minh City and Hanoi, and most of these users are already comfortable with foreign wallets and international exchanges. Pulling them onto domestic venues requires two things: (a) tax treatment that does not penalise migration, and (b) operational infrastructure on par with foreign exchanges. The tax piece addresses the first.

Piece two: the 0.1% rate — anchoring crypto to a familiar yardstick

Circular 32/2026/TT-BTC, effective 27 March 2026, applies three different tax rates by taxpayer type.Tài chính Việt Nam

The 0.1% rate for individuals is worth pausing on. It is precisely the rate currently applied to individual share-transfer tax on HOSE/HNX, and the calculation method is identical: charged on the transaction value, not on profit or loss. A buyer who buys at A and sells at B owes 0.1% × B, even on a losing trade. This linear approach is easy to enforce — exchanges withhold directly, users do not need to file — but punishes high-frequency traders, where tax cost compounds quickly.

The subtle point lies in scope: the 0.1% is triggered only when transactions flow through a service provider licensed in Vietnam.LuatVietnam Trades on foreign exchanges with no Vietnamese legal presence remain outside this withholding mechanism. In other words, Circular 32 collects tax not by the user’s geographic location but by the exchange’s legal jurisdiction. The framework nudges both sides to migrate flow onto domestic venues: investors get a clear and linear tax obligation, and domestic exchanges receive equity-equivalent tax treatment — they are not bucketed into asset classes that bear surcharges or VAT.

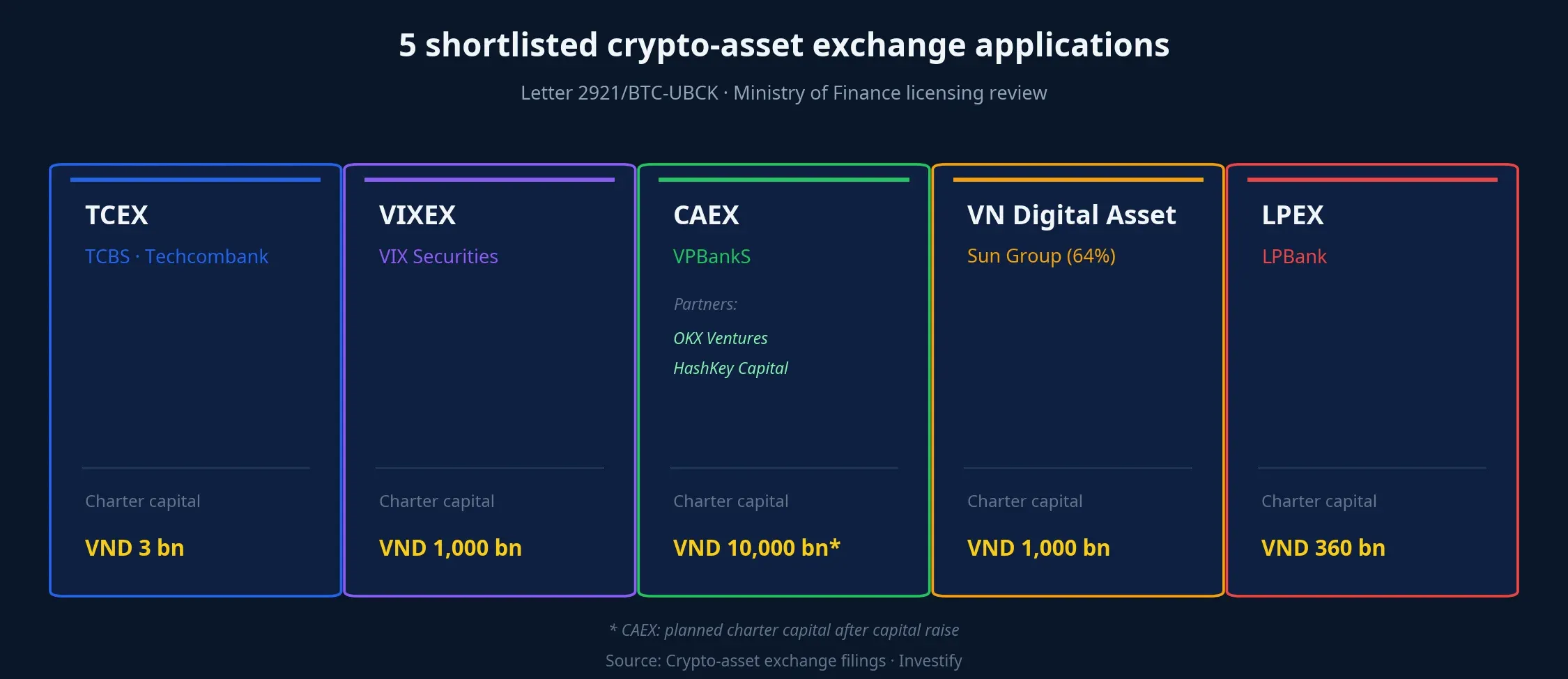

Piece three: five applications and a three-ministry review

Through Letter 2921/BTC-UBCK on 12 March 2026, the Ministry of Finance selected 5 of the 7 submitted applications as meeting initial criteria. According to early-April announcements, these five are now under review by the Ministry of Public Security and the State Bank of Vietnam ahead of the final licensing round.Người Quan Sát

The final review involves three agencies: the Ministry of Finance leads licensing; the Ministry of Public Security audits system security and AML capability; the State Bank reviews payment and custody integration. This is the milestone worth watching closely — the rigour of the final round can either thin the field or push the actual launch beyond the Prime Minister’s Q3/2026 target.

The capital structures across applicants are strikingly different. TCEX starts at just VND 3 billion in charter capital — a symbolic figure compared with VND 1,000 billion at VIXEX or CAEX’s planned VND 10,000 billion. The gap reflects different strategies: TCEX leans on the existing Techcombank-TCBS ecosystem, while CAEX is designed from the ground up as a large-scale exchange with international partners. CAEX is the only applicant to publish strategic agreements with OKX Ventures and HashKey Capital — both with international exchange operations and KYC standards.

A corporate view: TCBS bets big

At TCBS’s annual general meeting on 25 April 2026, Chairman Nguyễn Xuân Minh stated the strategy plainly: “leveraging the Techcombank advantage to shape the crypto-asset game”, with digital custody and tokenisation identified as the core verticals.Vietstock TCBS’s 2026 plan targets revenue of VND 13,227 billion and pre-tax profit of VND 7,535 billion, up 26% and 18% versus 2025. Crypto-asset products and gold are flagged as the two new growth drivers to be rolled out this year — conditional on receiving the licence in time.

The framing matters. TCBS does not treat TCEX as a side experiment; it is positioned as an ecosystem extension. When a leading securities house identifies crypto-assets as a revenue driver, competition in the final review will be sharper than expected. Each month of licensing delay is another month of flow staying on foreign exchanges, and whichever applicant receives the licence first will shape liquidity, listing standards, and international partnerships.

Why all three pieces converged

The simultaneity is not accidental. Each piece has its own driver, but they share a common purpose: pulling Vietnam’s crypto flows onto a supervised system.

- The Resolution arrived because two pressures converged: FATF commitments on AML required a formal supervisory channel for digital-asset transactions, and the underground market was already too large (~17 million users) to ignore.

- The tax circular was needed because a licensed exchange operating without a tax framework leaves the tax authority reactive. Issuing tax rules ahead of (or alongside) licensing lets exchanges integrate withholding from day one rather than retrofitting it later.

- Securities firms racing for licences because the gap between domestic equity flows and crypto flows on foreign exchanges is the single largest growth opportunity over the next several years. The first licensee will set liquidity, listing standards, and partner relationships.

The dominant driver is the first — international compliance and FATF pressure — but the other two determine the speed and quality of execution.

Implications for individual investors

For Vietnamese holding crypto on foreign exchanges, the new framework opens a choice — not a mandate, at least for now. Within the five-year pilot window, investors can keep assets abroad or migrate gradually as domestic venues come online.

A simple framework by user type:

- Low-frequency, long-term holders: a 0.1% per-transfer tax is not a meaningful burden when portfolio turnover is low. The main benefit of a domestic venue is reduced custody risk — no longer dependent on a foreign exchange that may restrict service or freeze Vietnamese accounts at its discretion.

- High-frequency traders: the 0.1% × number-of-trades cost compounds quickly, similar to high-frequency equity trading. Tax cost needs to be modelled when comparing against foreign exchanges, which charge fees but no Vietnamese-withheld tax.

- Domestic corporate holders: the 20% rate on net income is materially higher than the individual rate, suggesting that holding through individuals is typically tax-cheaper than through a corporate vehicle — unless the corporate side has offsetting advantages such as carried losses or specific cost-basis accounting.

Conclusion: the framework is set; execution begins

The legal framework is in place. The remaining variables — which exchange goes live first, which tokens are eligible for listing, what KYC and custody quality look like — will be settled over the next eight months.

Three signals to watch from now to Q3/2026: (1) official licensing announcements from the Ministry of Finance, particularly the order in which exchanges are licensed; (2) General Department of Taxation guidance on the actual withholding mechanism at exchange level; (3) the list of crypto-assets permitted for listing in the early phase — which is likely to be limited to large-cap tokens with strong international compliance records.

The Q3/2026 launch target remains feasible if the three-ministry review surfaces no major issues on system security or payment integration. A one-quarter slip is the most plausible downside scenario; a two-quarter slip would mean another half-year of flow remaining on foreign venues, and the project of “bringing 17 million users onto a supervised channel” loses another step.