On the morning of April 24, 2026 in Ho Chi Minh City, Chairman Nguyen Dang Quang opened Masan Group's annual general meeting with a "great connectivity" narrative and a high-case 2026 net profit target of VND 7,900 billion.Nguoi Quan Sat Alongside that headline came a less-emphasized proposal: Masan will pay no dividend for 2025 — the third consecutive year since 2022 — even as its subsidiary Masan Consumer (MCH) has just ratified a VND 5,270 billion cash dividend.

Retail shareholders holding MSN around VND 78,000 at the April 24 morning session have every right to ask: when MCH opens its cash box to the tune of 50% of charter capital, why does that cash not flow on down to parent-level shareholders? The answer sits in the last three lines of MSN's balance sheet — and it shapes the entire investment case for this ticker over the next twelve months.

2026 plan: revenue near VND 100 trillion, high-case NPAT VND 7,900bn

Management presented a consolidated revenue plan of VND 93,500–98,000 billion, equivalent to growth of 15–20% on the VND 81,930 billion base from 2025.CafeF The net profit after tax scenario (before minority interest) sits in the VND 7,250–7,900 billion range, up 76–92% on the VND 4,110 billion base of 2025. That is a large quantitative leap, and the high-case figure is only meaningful if every link in the chain below runs to plan.

The "great connectivity" strategy centers on four links management named at the AGM: the retail system, WinCommerce, WinX and the consumer data layer.Bao Moi WinCommerce carries most of the growth expectation. In 2025 the retail chain posted VND 38,979 billion in revenue and VND 501 billion in NPAT. For 2026, the plan opens 1,000–1,500 new stores concentrated in rural areas, targeting an NPAT margin of 1.8–3% and a VND 1,000 billion profit line. That margin needs to roughly double the current base (~1.3%) — the single variable that decides whether consolidated NPAT reaches the VND 7,900 billion zone.

Masan Consumer remains the highest-margin profit pillar, while Masan MEATLife contributed VND 9,230 billion in revenue and VND 619 billion in NPAT for 2025.TNCK Masan High-Tech Materials has returned to positive profit as tungsten and copper prices recovered. Management also set a 2026 cash flow target of USD 500 million, aiming toward USD 1 billion by 2030.VOV Those are large numbers, but the more practical question for retail shareholders is: once that cash is generated, where does it go?

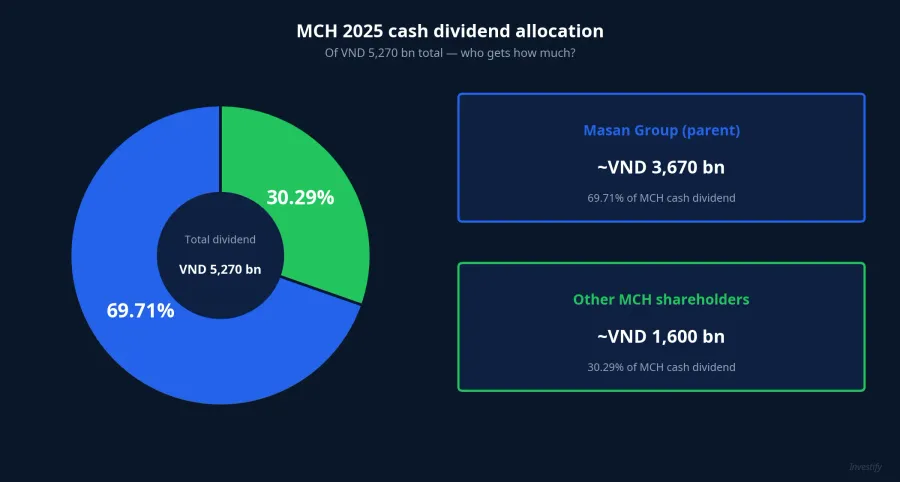

Where MCH's cash flows: VND 3,670bn stops at the parent

This is the real tension of today's AGM. MCH approved a 50% cash dividend totaling VND 5,270 billion for 2025 — of which VND 2,628 billion was paid as interim in 2025, with the remaining ~VND 2,642 billion due in 2026.VnExpress MSN owns roughly 69.71% of MCH through Masan Consumer Holdings, meaning approximately VND 3,670 billion of that VND 5,270 billion flows upstream to the parent. The remaining ~VND 1,600 billion goes to outside MCH shareholders.

The important point: cash from MCH does not evaporate on the way up — it stops at MSN parent. MSN's 2025 cash flow statement records VND 3,031 billion received from dividends and interest, most of which came from MCH itself. CEO Danny Le framed the retention policy as strengthening the balance sheet, cutting financial costs and reinvesting into digital infrastructure and WinCommerce.

Why keep it? At end-2025, MSN carried total debt of VND 64,880 billion against cash of VND 12,100 billion — net debt of VND 52,780 billion. With EBITDA of VND 16,730 billion in 2025, the net-debt-to-EBITDA ratio sits at 3.15x — elevated by consumer-sector standards (typically below 2.5x). Every VND 1,000 billion retained and applied to debt reduces interest expense and widens future NPAT. That is a coherent financial calculation. But for retail MSN shareholders, it translates to a third straight year on the outside of the cash the ecosystem is generating.

MSN or MCH: two very different cash profiles

Retail investors can reach Masan's consumer story through two doors, and those doors deliver opposite cash experiences. Same value chain, same governance — opposite cash-in-hand outcomes.

- Holding MCH directly: steady cash dividends. MCH has just locked VND 5,000 per share for 2025 and plans an interim of up to 50% for 2026, i.e. up to VND 5,000 per share.DNSE At VND 139,900 on the April 24 session, this is a clear cash-yield channel, but liquidity is thin (April 23 volume was only 330,100 shares).

- Holding MSN parent: betting on deleveraging and the "great connectivity" narrative. MSN liquidity is materially deeper (6.07 million shares on April 23), it sits in the VN30 and in many open-end funds — but the dividend channel is closed for now, so shareholder returns depend on price appreciation and on net-debt-to-EBITDA dropping to a lower band.

Neither door is "more correct" than the other — the decision frame depends on each portfolio's profile. Investors prioritizing steady passive cash flow will find MCH the better fit; thin liquidity is a reasonable trade-off. Investors willing to sit through a deleveraging cycle in exchange for capital appreciation and a possible future dividend will find MSN the right slot. Both tickers reflect different phases of the same ecosystem — the mistake is misjudging when to hold which.

Four checkpoints for the next 12 months

The "great connectivity" strategy is not rhetoric; it is a chain of measurable milestones across the next few quarters. For retail MSN shareholders, four indicators will decide which scenario is winning:

- WinCommerce store-opening pace — quarterly reports will show whether net store additions track the 1,000–1,500 annual plan. If Q2 slips, the VND 7,900 billion high-case is already hard to hold intact.

- WinCommerce NPAT margin — moving from ~1.3% in 2025 (VND 501bn / VND 38,979bn) to 1.8–3%. This is the margin lever that decides whether consolidated NPAT reaches VND 7,900 billion.

- Net debt / EBITDA — dropping from 3.15x to below 2.5x is the threshold usually cited as the trigger for reopening the MSN dividend. This is the "key" to the dividend-returns-to-parent story.

- MCH 2026 dividend cash flow — when the remaining ~VND 2,642 billion is booked will affect MSN parent's quarterly liquidity, and indirectly the pace of deleveraging.

Chairman Quang spoke of "creating superior value." For retail MSN shareholders, that value will show up in exactly those four numbers — not earlier, not through quotes. The Q2 report (expected late July) will be the first check: if store-opening speed and WinCommerce margin track, the high case stays intact; if they slip, the expectation range has to compress. Which scenario has the higher probability — that is for the next set of numbers to answer.