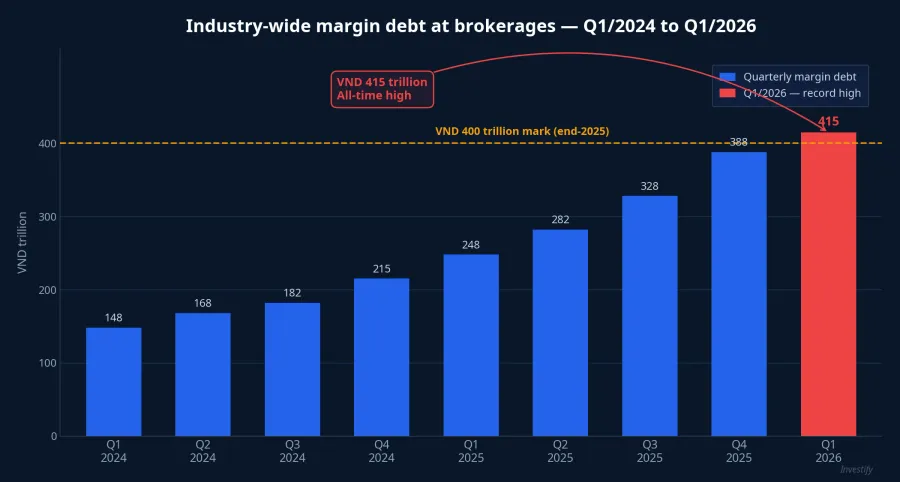

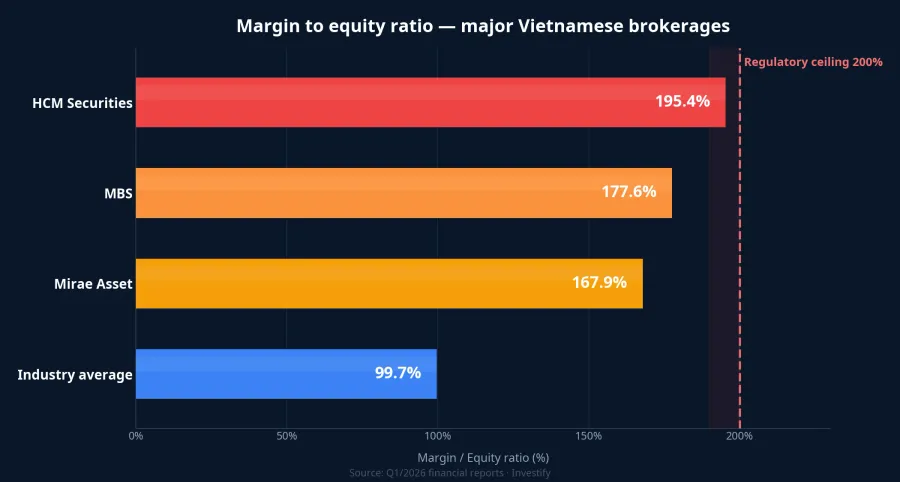

Industry-wide margin debt at Vietnamese securities firms reached approximately VND 415 trillion at the end of Q1/2026, up roughly VND 15 trillion from the end of 2025 and the highest level on record.VnEconomy More striking than the headline number, a cluster of large brokerages has pushed their margin-to-equity ratios close to the 200% ceiling set by Circular 121/2020/TT-BTC: HCM at 195.4%, MBS at 177.6%, Mirae Asset at 167.9%.LuatVN

The question worth asking is not how much margin grew, but where the funding to lend VND 415 trillion came from — and who ultimately bears the risk in this structure. The context deserves a closer look given that the VN-Index closed on April 23 at 1,870.36 points, a level that several research notes have flagged as overbought.

Margin lending: the most visible layer

When retail investors think about "brokerage credit", margin is the first thing they see. The industry-average margin-to-equity ratio sits around 99.7% — roughly one VND of lending for every VND of equity. That sounds comfortable, but the average hides significant dispersion.

HCM's 195.4% leaves only 4.6 percentage points of headroom before the legal ceiling. MBS at 177.6% and Mirae Asset at 167.9% are in similar near-cap territory. The outlier case of SBS, which briefly touched 216% at end-2025, demonstrates that the 200% boundary can be breached when oversight is loose.VnEconomy

Firms with ratios well below 100% — SSI, VCI — have far more room to expand lending when conditions are favourable. In the opposite direction, the near-cap group is the first that must shrink lending, and force-sell collateral, when the market turns. The same VN-Index move produces meaningfully different responses across these two groups, and which broker an investor chose matters more than the headline number.

The second channel: business cooperation contracts

Not every VND a brokerage extends flows through the margin book. Business cooperation contracts (BBC) are a second channel: a brokerage contributes capital to a joint operation with a corporate or institutional partner and shares the resulting profits, without forming a new legal entity. Individual contracts typically run from a few hundred to a few thousand billion VND.

Unlike margin, which is standardised under Circular 121, BBCs sit in a thinner accounting zone. The contributed capital may be recorded as a financial asset if the brokerage does not control the operation, and profit shares are recognised under the contract terms. From 2026 onward, accounting standards have tightened the treatment of non-controlling parties, but transparency for outside readers of financial statements remains far lower than the monthly margin disclosures.

The third channel: corporate bonds via the proprietary book

Following the 2022–2023 issuance crackdown, commercial banks reduced their corporate bond holdings. Securities firms stepped in to fill that gap through their proprietary trading books, recorded under FVTPL, HTM or AFS. The size has become material: SSI's proprietary book stood at approximately VND 46.2 trillion at end-Q1/2026, mostly certificates of deposit and bonds.VnEconomy

Measured against equity, SSI is above 116%, VND around 92%, VCI around 90% — meaning the proprietary book alone is the same size as, or larger than, equity, before counting margin lending. Combine the two and the total assets exposed to market risk at the largest brokerages exceed equity by a wide multiple. This is the point that strong quarterly earnings can obscure: today's profit comes from precisely the desks carrying tomorrow's mark-to-market risk.

Funding: retail investors are both creditor and debtor

These three lending channels need corresponding funding. The capital structure of large Vietnamese brokerages today rests on three buckets.

Savings-style products are deposit-like instruments issued by brokerages or their partners, paying 6–8% annually with flexible terms. Retail investors place money with the brokerage expecting a yield slightly above bank deposits; the brokerage uses the same money to fund margin, BBCs and corporate bond holdings. The loop closes on itself: the same retail investor is creditor through the savings product and debtor through the margin account.

Bonds issued by the brokerages themselves are the second source. SSI, VND and TCBS have issued at large scale over the past two years, typically pricing above bank deposits of the same tenor to attract flow. This funding lifts lending capacity quickly but raises cost-of-funds whenever market rates drift higher.

Bank borrowings — the third source — are concentrated at brokerages with a parent bank, such as VPBankS and MBS. Pricing is below bond issuance, but credit limits depend on the parent bank's policy.

A common feature: tenors are short and the structure rolls quickly. When deposit rates rise and money flows out simultaneously, pressure arrives from all three sides at once. TCBS chairman Nguyen Xuan Minh said on April 23 that the bond market needs three to six months to absorb the recent shock from rising deposit rates.NguoiQuanSat The fact that this view came from a major brokerage is not incidental — it signals that the funding pressure on the industry itself is real.

How a single break propagates

The three lending channels and three funding sources connect into a chain that can be traced. Suppose a large margin borrower defaults, or a sharp correction triggers wide-scale forced selling. The propagation usually unfolds in four steps.

The brokerage must liquidate the affected accounts first. If the size is large enough, prices fall under the selling pressure — other accounts cross into a margin shortfall and trigger the next wave. The corporate bond and equity holdings inside the proprietary book are simultaneously revalued downward, compressing available capital. Finally, depositors in the savings products may demand redemption if negative news surfaces, precisely when the brokerage is having difficulty liquidating assets.

Smaller versions of this loop have been observed in the sharper drawdowns of early 2026 and several sessions in 2025, when record margin debt overlapped with overbought levels. To be fair: the trigger does not have to come from the brokerage layer. It can come from foreign net selling, from negative corporate news, or from macro shocks. Brokerages are an amplification layer, not the ignition layer — but the VND 415 trillion leverage structure ensures that whatever shock arrives travels further than it would in a less levered market.

A framework for reading brokerage financials

Retail investors can gauge how stretched their own brokerage is by reading four lines on the quarterly financial statements:

- Margin lending — divide by equity for the margin/equity ratio. Above 150% is a sensitive zone; above 180% is near-cap.

- FVTPL financial assets — read the notes that break out equities, corporate bonds and certificates of deposit separately. The corporate bond share over equity indicates how much corporate credit risk the brokerage has absorbed.

- Business cooperation contracts (BBC) — usually buried in "other receivables" or "other investments". Large balances without detailed counterparty disclosure are a signal that warrants additional caution.

- Issued bonds and long-term borrowings — these tell you how dependent the brokerage is on market-based funding. Short tenors and a high share are a clearer liquidity-risk profile.

Two ratios to compute before looking at anything else: margin-to-equity (200% cap) and total liabilities to equity (firm-wide leverage).

What to watch in the next two weeks

Q1/2026 financial statements from the major brokerages will be fully published over the next two weeks. This is the moment to recheck the four lines above before deciding how to structure accounts for the remainder of Q2.

Three signals worth tracking: (1) whether HCM's margin-to-equity ratio crosses 200% in the official Q1 filing; (2) whether FVTPL portfolios continue to expand and what share corporate bonds occupy within them; (3) whether the coupon on Q2 brokerage bond issuance prints above Q1 — a direct read on the industry's cost of funds.

The risk that retail investors carry is not only in the individual tickers in their accounts. It is in the credit structure of the brokerage serving them — and that structure, at this moment, is at the most stretched level it has ever been.