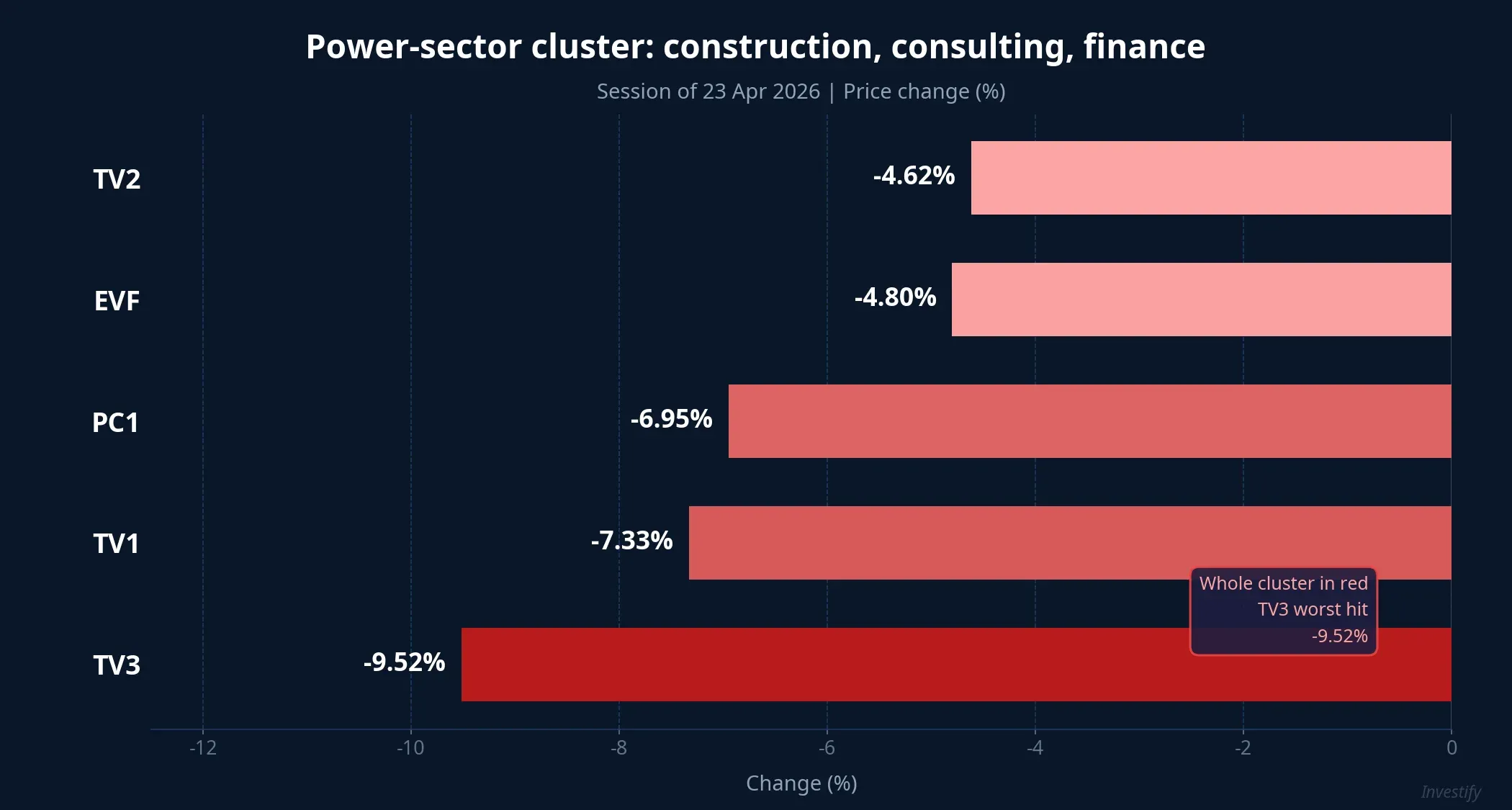

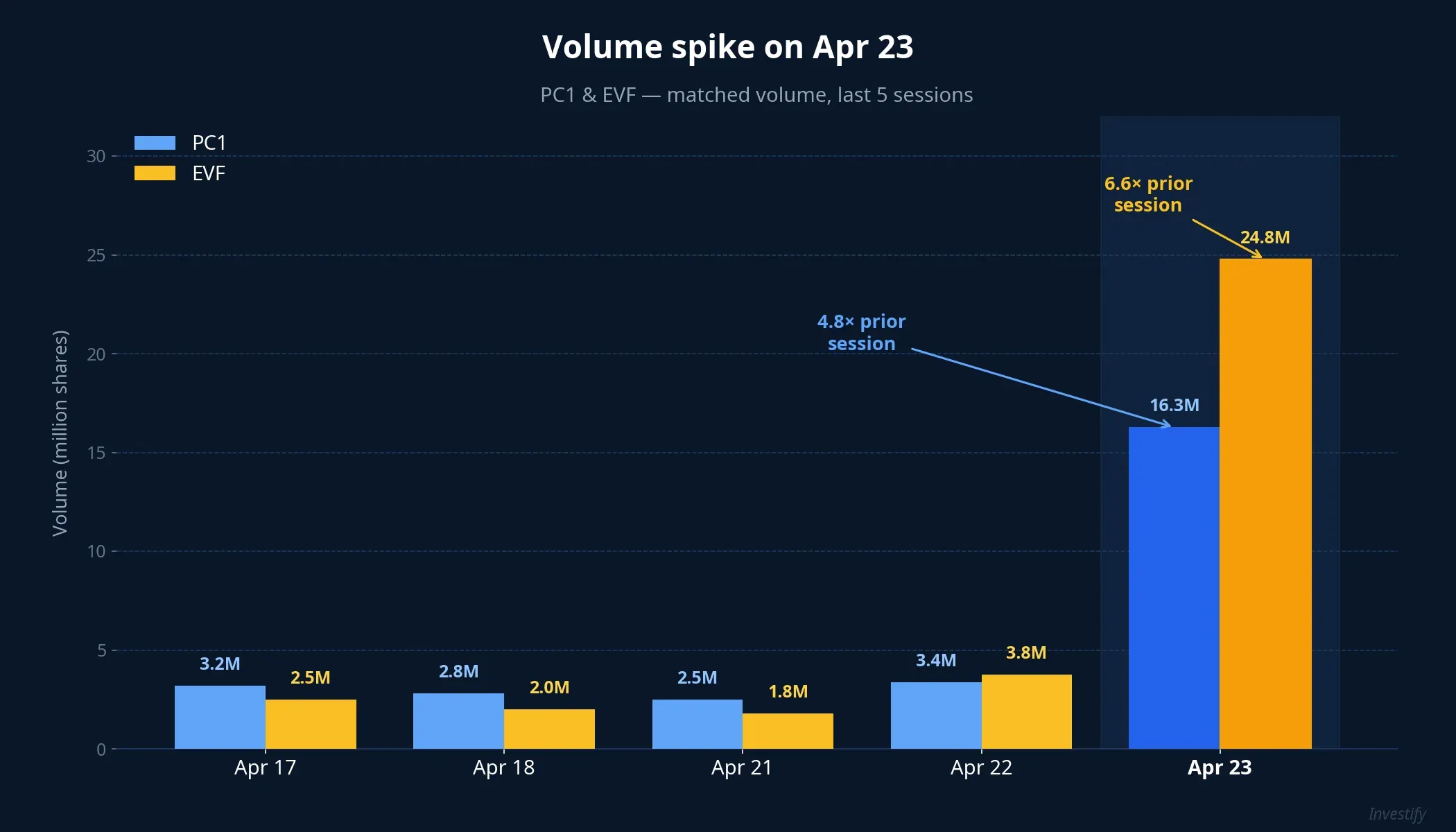

On the Apr 23 session, while the VN-Index still closed up 0.70% at 1,870.36, the power-sector cluster of construction, consulting and finance names turned deep red. PC1 hit the floor at 24,100 VND, down 6.95%, with over 7.7 million shares locked at the sell queueCafeBiz and total matched volume reaching 16.26 million — nearly 5× the prior session. In the same basket, TV3 shed 9.52%, TV1 fell 7.33%, EVF lost 4.80% on volume of 24.76 million shares (6.6× the Apr 22 level), and TV2 gave up 4.62%.

An unremarkable day for the index, a structurally bad day for one basket. The twist: the Government Inspectorate’s conclusion on private-placement corporate bonds, released in February 2026VnEconomy, only named three entities in the energy sector: PC1, VCP Energy, and Bac Phuong Energy. TV1, TV2, TV3 and EVF do not appear anywhere on that list. So why did the board treat the whole cluster as a single risk bucket today?

What the inspection actually says about PC1

Among 14 issuers flagged for using bond proceeds in breach of plan or regulation, PC1 was cited for 90 billion VND deployed off-purposeTheLEADER. PC1 also sits — alongside VCP and Bac Phuong — inside a group of 19 issuers cited for late disclosure of half-year and annual financial reports and late reporting on how bond proceeds were used.

The three entities collectively account for 3 issuances, 5 bond codes and roughly 3,840 billion VND. The underlying risk has two separate layers: post-issuance cash flow not managed according to the stated plan, and delayed or incomplete disclosure to bondholders. This is a specific legal risk attached to three named issuers — not a sector-wide risk.

There is a detail the market quietly dismissed back in February. The inspection has been public for more than two months; PC1’s price barely moved at the time. On Apr 23, however — exactly two days before its scheduled 2026 annual shareholder meeting on Apr 25Tap Chi KTTC — selling pressure piled up sharply. The combination of a re-reading of a two-month-old conclusion plus the prospect of pointed shareholder questioning repriced the stock, even though the conclusion itself contained nothing new.

Why the whole basket sold off when only one name was cited

At the ownership level, PC1 holds no direct stake in TV1, TV2, TV3 or EVF, and none of them hold PC1. EVF has never disclosed any bond exposure to the three inspected issuers. Legally, TV1–TV3 (i.e. PECC1–PECC3, three power-construction consultants in the EVN ecosystem) and EVF (EVN Finance) all sit outside the scope of the conclusion.

What ties them together is not ownership — it is sector recognition. Retail investors read the board by basket. The “power construction and consulting cluster” shares common traits: cash flow depends on EVN’s grid and generation capex schedule, all face the same project-delay risk, all rely on bond issuance to fund working capital. When one name in the basket gets called out by inspectors, the market’s first instinct is sell first, read later — especially for mid-cap tickers with thin liquidity like TV1 (around 0.25 million shares per session) and TV3 (around 0.05 million).

This is a familiar pattern since the 2022–2023 bond-market episodes: a narrow legal finding gets amplified into broad group-level risk. The difference this time is timing — the conclusion has been public for two months, but the trigger for mass selling came from the lead name’s own annual-meeting calendar, not from any fresh move by inspectors.

A framework to separate the two risks

Two distinct kinds of risk are being lumped together and need to be pulled apart. Corporate legal risk attaches to specific named issuers: it comes with regulatory recommendations, a quantified violation amount (90 billion VND for PC1), and an oversight trajectory from the authorities. Group sentiment risk describes how stocks in the same perceived basket — but absent from the conclusion — react. The selling here comes from sector association, not from any violation on record.

The two recover at very different speeds. Legal risk only compresses when the named issuer delivers something concrete: a remediation plan, evidence of corrective action, a final enforcement outcome. Sentiment risk typically fades over a few sessions to a few weeks once no fresh information arrives — volume normalises, the price finds a new base.

A simple mental model for investors holding names in the basket: check the official named list against the ticker you own. If it is not on the list, what is hitting the price is sentiment risk. If it is on the list, read the violation content and assess the remediation outlook before deciding whether to hold or trim. Collapsing both risks into one reflex — sell everything or hold everything — is the most expensive mistake to make.

What to watch from here

For PC1, the Apr 25 annual meeting is the nearest information milestone. Its 2026 plan is public: revenue of 15,618 billion VND, net profit of 1,056 billion — down 22% from 2025 — combined with a plan to issue 46.6 million shares as stock dividendBao Dau Tu and an additional offering to existing shareholders. Three questions shareholders should press in the hall: how far the 90 billion VND off-purpose use has been remediated, how post-issuance bond disclosure will be tightened going forward, and why the profit target falls 22% while the company simultaneously raises significant new capital.

For TV1, TV2, TV3 and EVF, the earliest recovery signal is usually when volume normalises and the first up-session prints on a lower base — evidence that the sentiment shock has been absorbed. Absent fresh inspectorate commentary on the broader basket, the current discount reflects basket reflex rather than any violation record.

Three things to monitor in the coming sessions: the content of PC1’s Apr 25 meeting resolution — specifically the 90 billion explanation and the bond-transparency roadmap; the liquidity trajectory of TV2 and EVF, the two most liquid names in the basket and therefore the earliest indicators for the rest; and any additional disclosure from either the inspectorate or the companies on remediation. The inspection conclusion does not change, but how the market prices the risk will move with each new data point — and that is the real thing to watch if you have exposure.