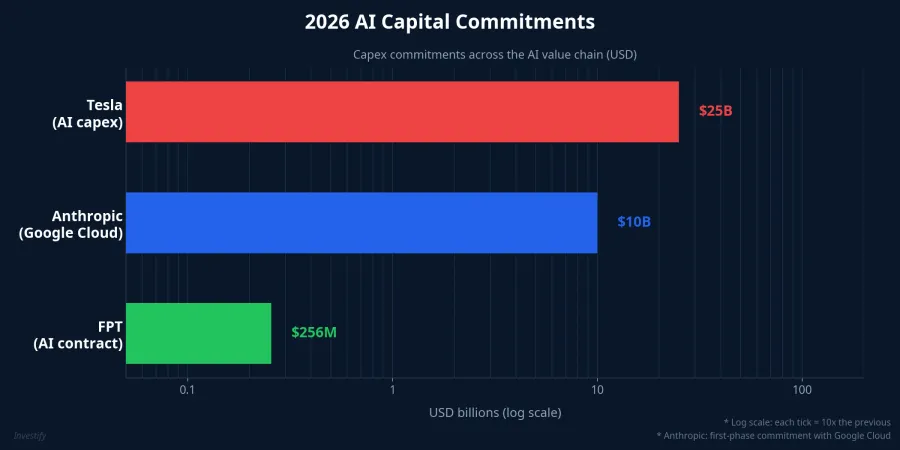

On the night of April 22 (US time), three signals converged on the same AI cycle within hours of each other. Tesla reported Q1/2026 results with EPS of 41¢ beating the 37¢ consensus, but the more important number was the CFO lifting full-year 2026 capex guidance from $20B to more than $25B, versus just $8.6B for all of 2025.CNBC At the same time, at Google Cloud Next 2026, Google split its Gen-8 AI chip into two distinct lines, one for training and one for inference, claiming 3x faster training and 80% better performance per dollar versus the prior Ironwood generation.TechCrunch

On the same day in Hanoi, FPT reported Q1/2026 results with pre-tax profit of over VND 2.8tn and a string of multi-million-dollar contracts, including a $256M AI deal and a $100M contract in Japan.CafeF

The easy mistake looking at these three announcements is to bucket them all as "AI stocks" and trade the headlines. But once you separate the numbers, the three companies sit in three very different positions within the same cycle, each with its own cash-flow profile, risk exposure, and monitoring signals.

Position 1: Tesla, the self-financed self-user

Tesla is not selling compute to anyone. All $25B of 2026 capex flows back into its own infrastructure, supporting three pillars: the FSD self-driving system, the Robotaxi network (running unsupervised in Austin since June 2025 and expanding to Dallas and Houston in April 2026), plus the Optimus humanoid robot and the Dojo supercomputer. That $25B figure does not yet include Terafab, the domestic AI chip plant Tesla is co-developing with SpaceX.

This position has large long-term optionality but comes with a long stretch of negative cash flow. Every dollar of capex has to earn itself back through vehicle sales, Megapack battery units, or eventual Robotaxi service revenue. In Q1, no Robotaxi or Optimus revenue was booked. That is why Tesla shares initially rose about 4% after hours, then gave back the entire move once the $25B number hit: the market had already priced in $20B, so the extra $5B just means more near-term cash burn in exchange for a long-dated payoff that has yet to show up in revenue.CNBC

Position 2: Google, the infrastructure vendor

Google sits one layer up, selling tools to the companies that actually want to run AI. The Gen-8 chip now splits into two lines: a training chip for firms building foundation models, and an inference chip for enterprises serving trained models at scale. Splitting the two streams is a direct shot at Nvidia's data-center dominance.

The evidence that large customers are ready to diversify away from traditional GPUs came in the form of the Anthropic deal: a commitment to deploy over 1 gigawatt of capacity and up to 1 million TPU chips in 2026.Anthropic The initial phase is estimated at around 400,000 Ironwood chips, worth roughly $10B flowing through Broadcom as the assembly partner.VentureBeat

The upside here is tied directly to US Big Tech's capex curve. The more Anthropic, OpenAI, and Meta spend, the more chips Google ships. Conversely, if that cohort slows capex in the second half of 2026 under margin pressure, Google feels the brake first.

Position 3: FPT, the enterprise AI integrator

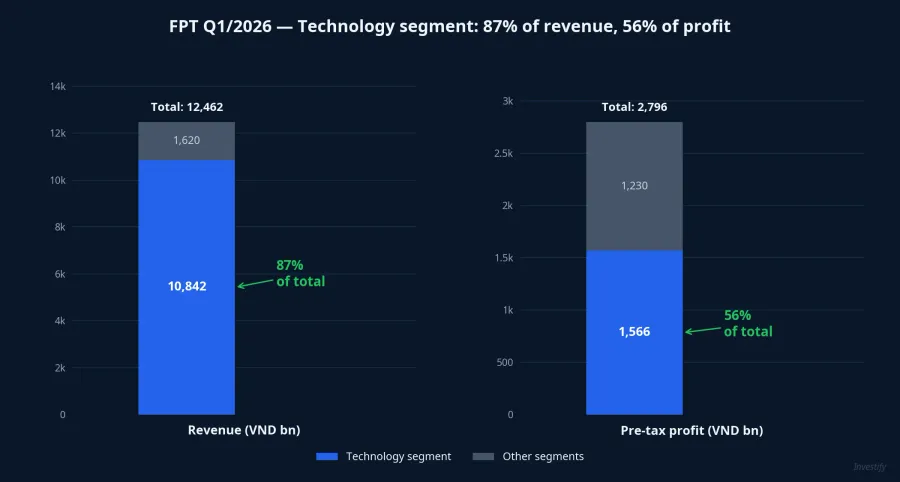

FPT is not making chips and not consuming compute at hyperscale. Its way of monetizing the AI cycle is to deliver digital-transformation services to enterprises — the layer that sits closest to the end customer. The Technology segment (mostly FPT Software) contributed VND 10,842bn in revenue and VND 1,566bn in pre-tax profit in Q1, up 11% and 10.6% year-on-year respectively. That is 87% of group revenue and 56% of group profit.CafeF

The structure of the two large deals signed in the quarter is the part worth reading closely. A $256M digital-transformation contract with an Asian energy group, and a $100M contract in Japan. FPT Software's customer base is mostly non-US, with Japan still the largest market by revenue. Signing deals above the $100M mark is a signal that demand for AI deployment outside the US Big Tech ecosystem keeps flowing.

This position does not grow as fast as the chipmakers at a cycle peak, but it also does not carry the negative cash-flow profile of the self-financed self-user. Growth depends on the number of new projects, contract value signed per quarter, and the pace of revenue recognition on booked deals — not directly on US Big Tech's infrastructure capex curve.

How each position responds to a capex squeeze

Assume US Big Tech cuts capex by 25% in the second half of 2026 under margin pressure. The three companies respond very differently:

- Tesla gets pushed to prove a faster payback path for Robotaxi and Optimus. The stock faces re-rating risk, even though spending is internal and not immediately cut.

- Google loses momentum selling chips into the pure AI-native cohort (Anthropic, OpenAI). Revenue from the already-signed Anthropic deal still flows, but new bookings get harder.

- FPT takes an indirect hit: Japanese, European, and Southeast Asian clients may slow new bookings if global tech-capex sentiment turns. But the backlog already signed (including the $256M and $100M deals) still feeds cash into several quarters ahead, so the brake reaches FPT later and milder than the other two.

Read FPT on its own terms

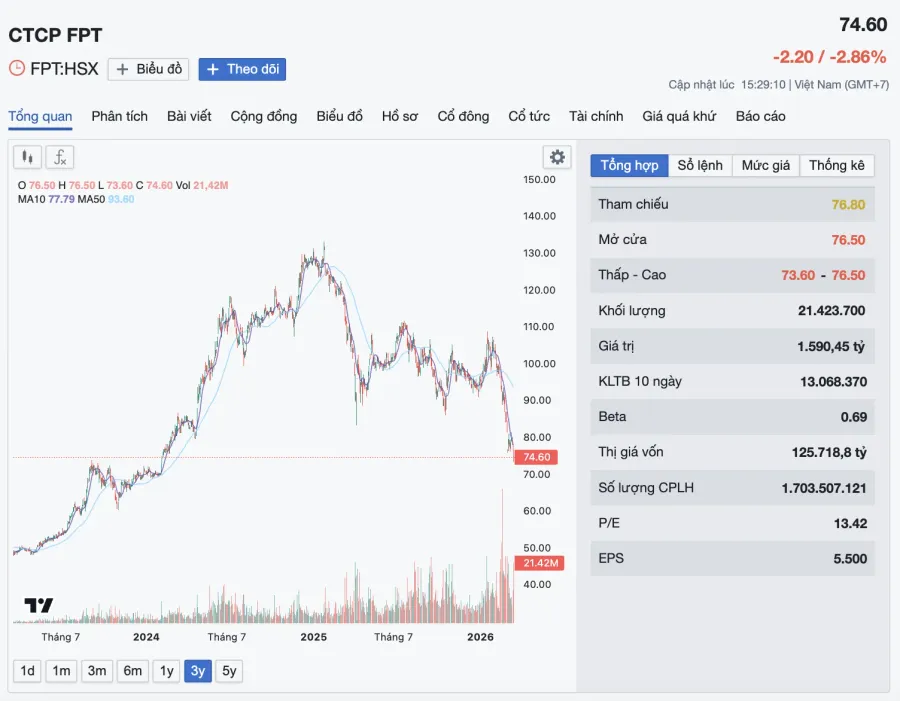

At the current mark, FPT closed April 22 at VND 74,600, for a market cap of VND 127.1tn. The full-year 2026 plan is VND 58,580bn in revenue and VND 11,629bn in pre-tax profit, representing growth of 11% and 20.6% versus 2025.CafeF After Q1, FPT has completed 21% of the revenue plan and 24% of the profit plan. That is slightly ahead of a flat 25%-per-quarter pace on profit and near it on revenue. It is the anchor to track over coming quarters, not the headlines Tesla or Google delivered last night.

The reading principle is clear. Tesla and Google news matters for assessing the AI cycle overall, because it tells you whether US Big Tech is accelerating or decelerating its spend. But those are not direct signals for FPT. The direct FPT signals are the number of multi-million-dollar deals signed each quarter, the share of Japan and Asia-Pacific revenue in the customer mix, the pace of recognition on the large contracts already signed, and the US exposure disclosed at the AGM.

What to watch over the next two quarters

The thesis from Q1 is clean: FPT sits in the services layer deploying AI for enterprises outside the US Big Tech ecosystem, and Q1 reinforces that thesis with 21% revenue and 24% profit progress against the annual plan. The main risk is global tech-capex sentiment: if it turns in the second half of 2026, new bookings from Japan, Europe, and Southeast Asia will slow, though the existing backlog still secures cash flow for several quarters ahead.

Three checkpoints to watch: (1) new multi-million-dollar contracts in Q2 and their geographic mix; (2) revenue split by market disclosed at the AGM; (3) H2 2026 tech capex guidance from Google, Microsoft, and Meta. These three indicators, not Tesla's after-hours move last night, are the anchor for assessing FPT.