On the afternoon of 22 April 2026, the AGM of Phu Nhuan Jewelry JSC (PNJ) approved a 2026 business plan of VND 48,660 billion in revenue (+37% vs 2025) and VND 3,409 billion in after-tax profit (+21%). The headline number isn’t the top line, it’s the margin. Chairwoman Cao Thi Ngoc Dung committed to keeping the gross profit margin within a 17–20% band for the full year, with Q1/2026 already above 20%. Newly-elected CEO Phan Quoc Cong said PNJ stands ready to import its full quota of gold the moment the State Bank of Vietnam (SBV) grants a licence.Investify

The pledge lands at a policy inflection point for Vietnam’s gold market. Decree 232/2025/NĐ-CP, issued on 26 August 2025, amended Decree 24/2012 to end the state monopoly on gold-bar production and raw-gold imports.Investify As of 14 April 2026, the SBV has received 11 applications for gold-bar production licences from enterprises and commercial banks; the identities of the 11 applicants have not been disclosed.Investify Given PNJ’s margin structure and business model, the licensing story is more than a policy event. It is one of the pivotal variables that will determine the realised margin for all of 2026.

The 20% margin sits on two layers

Look at six years of data. PNJ’s gross profit margin over 2020–2024 oscillated in a steady 17.5–19.6% band. In 2025, it jumped to 21.97%, the highest in the six-year series. In Q1/2026, the margin eased back toward 20%. According to Nguoi Quan Sat, the reason is that 24K gold revenue in the quarter rose 324.7% year-on-year, pulling the blended margin down from 21.3% in the year-ago quarter.Người Quan Sát

Unpacked, PNJ’s margin sits on two structurally different layers, and separating them sets up every scenario that follows.

The product-design layer is the stable one. PNJ focuses on thin, light, personalised jewellery. Raw-material cost is a smaller share of retail price, and value-add comes from design, craftsmanship and brand. When gold prices move, this product mix absorbs the swing better because the workmanship fee does not move with gold. That is why gross margin held 17–19% across 2020–2024 despite multiple gold-price cycles. This layer is the floor.

The gold-price volatility layer is the dynamic one. A flexible product mix between designer jewellery and 24K gold, combined with batch-lot input-price locking when conditions are favourable, lets the company lift margin above the floor. This is the source of the jump from 17.64% (2024) to 21.97% (2025) and the reading above 20% in Q1/2026, with SJC gold trading around VND 170 million per tael. This layer is the ceiling, but it is a conditional ceiling.

The 17–20% band PNJ has published mirrors this two-layer structure accurately. 17% is a floor proven across 2020–2024; 20% is a ceiling reached only when both layers work together. The fuel for the dynamic layer comes from two sources: access to raw material, and gold-price volatility. Neither is locked in for 2026.

Three scenarios for PNJ’s margin into end-2026

Three unresolved variables will decide where the margin lands: whether PNJ is among the licensed gold importers, whether gold prices keep moving, and how high the 24K share of revenue rises.

Scenario 1: PNJ is on the approved list. If PNJ is among the 11 applicants the SBV approves, the company sources raw material through official channels rather than buying from a third party. The dynamic layer’s margin is preserved because input cost is lower. Moreover, in the early post-licensing window, total raw-gold supply into the market remains constrained by the quarterly quotas the SBV assigns to each licensee. The committed 17–20% band holds, with scope for modest improvement toward the upper end in the first few quarters. Confirming signal: SBV publishes the approved list together with quarterly quotas, and PNJ is on it.

Scenario 2: PNJ is not licensed. If PNJ is not on the list, it must source raw material through a licensed third party. Input cost rises by the intermediary’s cut, eating into the margin relative to Scenario 1. Here the design layer still holds a 17–18% floor as in 2020–2024, but the dynamic layer loses most of its fuel. Total margin can be compressed toward sub-17% if the 24K share stays elevated at Q1/2026 levels; the 17–20% commitment then grazes the bottom of the band. Confirming signal: PNJ is absent from the SBV list, and 24K revenue keeps accelerating into Q2.

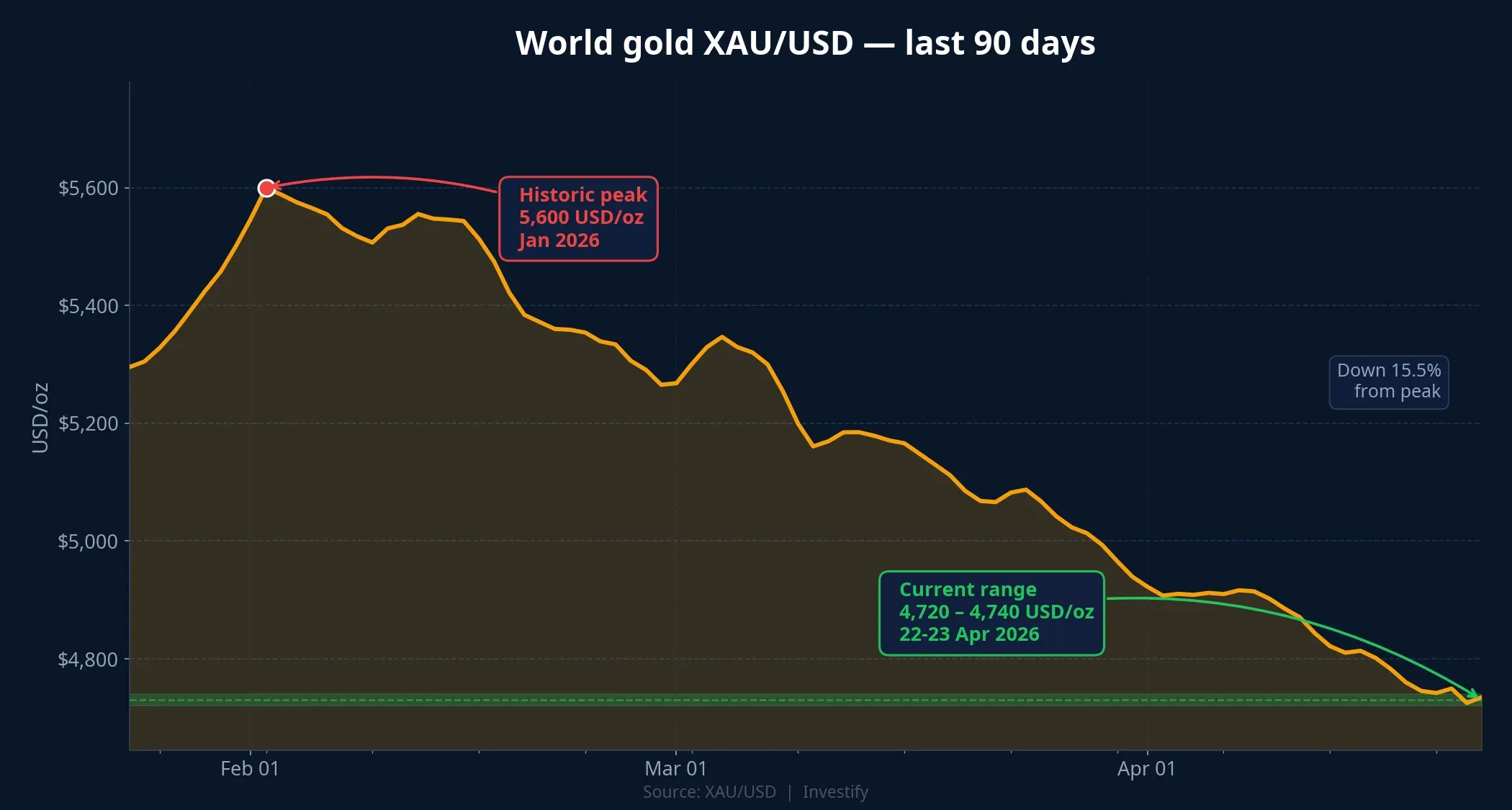

Scenario 3: gold cools off and trades sideways. World gold is down 16% from a January peak of 5,600 USD/oz toward a 4,720–4,740 USD/oz range on 22–23 April.Investify If gold transitions into a sideways phase in H2 2026 (with daily ranges tightening), the dynamic layer loses its main weapon. A flexible product mix no longer generates the margin lift from input-price spreads. Margin falls back to the design-layer floor, the 17–18% zone of 2020–2024. This scenario is independent of the licensing story: even if PNJ is licensed, a sideways gold market means the self-import advantage does not translate into strong dynamic margin. Confirming signal: world gold daily ranges compress below 1%, and SJC follows a similar pattern for several weeks.

The three scenarios are not mutually exclusive. The most likely blend into end-2026 is a hybrid: Scenario 1 or 2 on the licensing side, and a middle-ground volatility regime on gold, neither as strong as Q1 nor as flat as Scenario 3. In other words, the year-end margin most plausibly lands somewhere inside the 17–20% band, with the exact position depending on how the three variables combine.

Signals to watch and a reading frame for retail investors

The chairwoman’s 20% margin pledge should be read as a conditional ceiling, not a guaranteed floor. That framing matters because it changes how retail investors treat the number. 20% is not a starting point for further upside; it is a ceiling that requires specific conditions to reach.

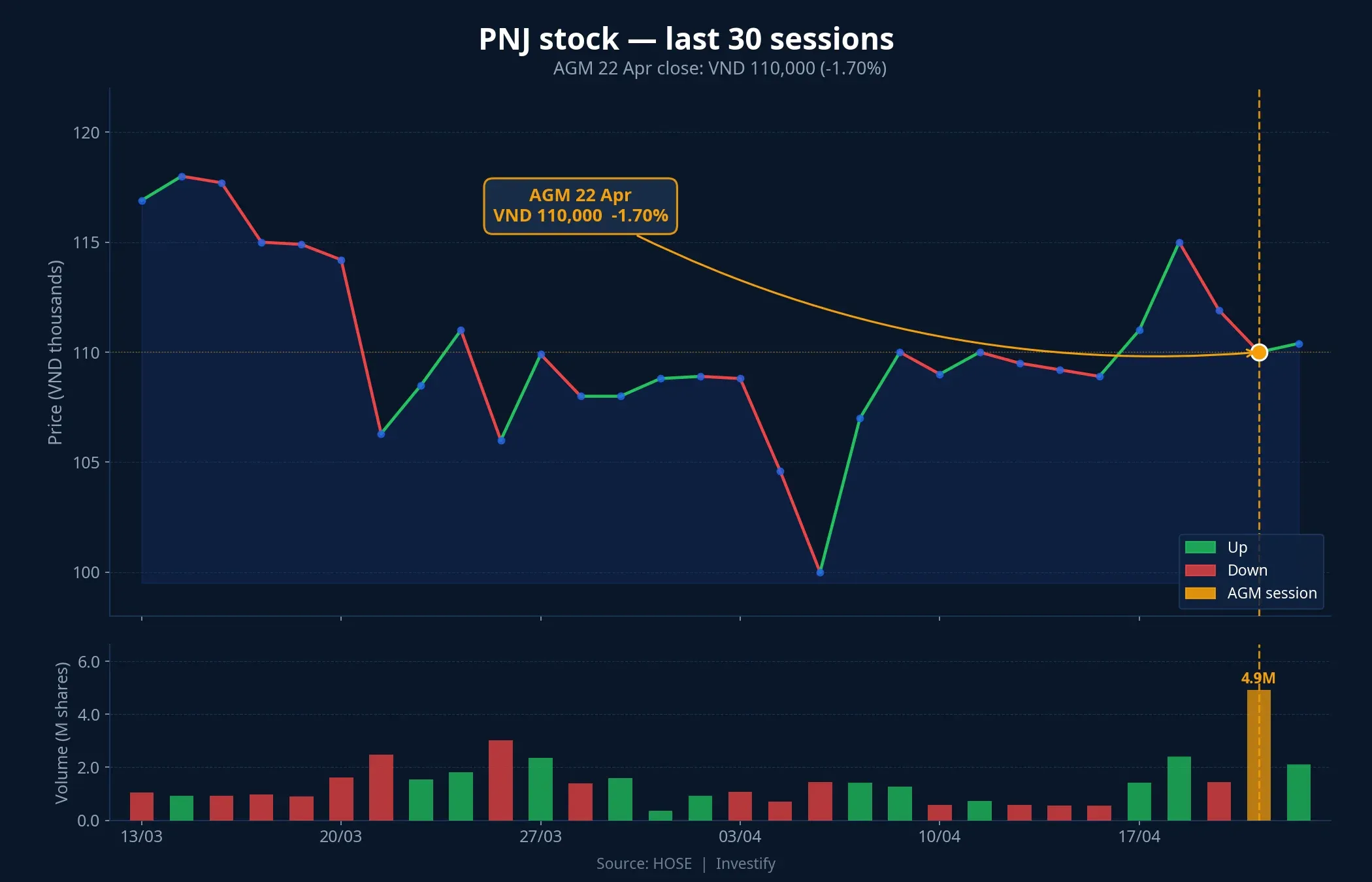

PNJ stock closed at VND 110,000 on 22 April, down 1.70%; this was the second consecutive decline after a 3.60% bounce on 20 April. Market cap stands at VND 37.5 trillion. The current price zone suggests the market has not yet priced in any one of the three scenarios. The Q2/2026 report and the SBV’s licensed list will be the two main resolution points.

For retail investors considering PNJ in a portfolio, the standard analytical frame under current conditions has two branches.

- Treat PNJ as a position within the gold asset class, not a substitute for physical gold bars. PNJ’s margin depends on licensing, product mix and gold-price volatility; it does not track gold prices linearly. A gold-price rally won’t necessarily lift PNJ shares by the same magnitude; a sideways gold market can compress PNJ’s margin while bullion itself holds its price.

- Track the three signals that resolve the scenarios. The SBV’s licensed list (resolves Scenarios 1 vs 2), gold-price volatility (resolves Scenario 3), and the 24K share of revenue in the Q2/2026 report (confirms whether the product mix can keep feeding the dynamic layer).

One closing note on the gold asset class overall. The SJC premium over world gold on 22–23 April still sits around VND 20–20.5 million per tael, even though Decree 232 has opened the legal door. This premium will be among the first variables to move once the SBV approves the 11 applications and bullion supply diversifies. For retail investors who want to maintain a gold allocation in their portfolio, the time to re-evaluate across channels (SJC bars, 9999 rings, gold equities such as PNJ) is after the SBV publishes its licensed list, not before.

Looking at the numbers, 20% is a structurally precise commitment: two stacked layers, three scenarios, three signals. Current evidence is insufficient to decide whether year-end margin will lean closer to 17% or 20%. Wait for the SBV’s list and the Q2/2026 report before reaching a conclusion.