On April 30, 2026, billionaire Tran Ba Duong's THACO is scheduled to break ground on the Ben Thanh – Thu Thiem metro line — 5.6 km long, 6 underground stations, a total investment of about 33 trillion VND.Tuoi Tre This is the first time a private Vietnamese automotive group has put its name to a trillion-dong urban rail line under a PPP – BT contract. But this isn't a sudden pivot from cars to rails: it is the closing move of a capability build-up that has been running quietly for years, across three pieces — THACO Industries, Dai Quang Minh, and Truong Hai.

As of April 2026, the pipeline of rail-infrastructure projects THACO has been tasked to study or has proposed joining has already crossed roughly 270 trillion VND.Nguoi Quan Sat For retail investors, the question is no longer "THACO is building metro" but: which listed tickers will receive that order flow, and on what timetable.

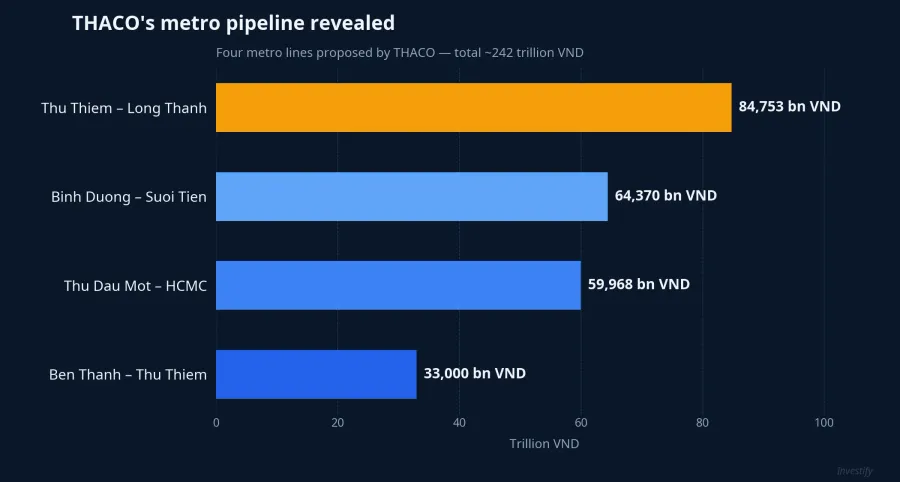

The four-line pipeline

Ben Thanh – Thu Thiem (~33 trillion VND). Fully underground, 5.6 km, 6 stations, crossing the Saigon River into Thu Thiem. HCMC has required investor selection before April 15, 2026, groundbreaking before April 30, 2026, and completion before 2030.CafeF

Thu Thiem – Long Thanh (~84.753 trillion VND). 42 km, 20 stations, double-track 1,435 mm gauge, design speed 120 km/h. The line connects directly to Long Thanh Airport — a 16 billion USD mega-project taking shape.CafeF Dai Quang Minh is running the feasibility study; target groundbreaking before June 30, 2026 and synchronized completion by 2030.

Two HCMC – Binh Duong lines (~124 trillion VND). In early April 2026, the Becamex – THACO consortium proposed studies for two metro lines: Binh Duong New City – Suoi Tien (64.370 trillion VND) and Thu Dau Mot – downtown HCMC (59.968 trillion VND).CafeF The model is PPP combined with TOD-based land development; plan calls for Q1/2027 groundbreaking, operation from 2030.

These four lines alone reach 242 trillion VND. Add the backbone construction packages THACO is participating in on line 2 Ben Thanh – Tham Luong, and the ecosystem's total order exposure approaches the 270 trillion VND figure media outlets have cited.

In-house capability is already in place

Tran Ba Duong isn't entering the rail business empty-handed. In February 2026, he issued Chairman's Message No. 21 committing to mastering "core rail technologies" — tunnel boring machines (TBMs), pre-cast concrete girders, elevated viaducts — and to finishing three HCMC metro lines by 2030.Vietstock

Three internal pieces explain why the pipeline is feasible:

- THACO Industries is building a 320-hectare rail industrial complex at Binh Co, scheduled to start operation in September 2026. Products include locomotives, rolling stock, pre-cast concrete elements, TBM machines, and tunneling services — i.e., the technical core of a metro line.

- Dai Quang Minh has controlled the Thu Thiem land bank for a decade and is now directly running the feasibility study for the Thu Thiem – Long Thanh line. Urban-infrastructure experience is the key to the BT land-swap model, where counter-value land determines project IRR.

- Truong Hai supplies logistics, transport chains, and two decades of cash flow from car sales — the financial base for equity commitments in highly leveraged projects.

These three pieces have existed separately for years; April 30, 2026 is simply the moment they are fused into a single investment commitment.

How private PPP differs from ODA

Metro line 1 Ben Thanh – Suoi Tien and metro line 2 Tham Luong – Ben Thanh followed ODA funding: low interest rates, long maturities, but tied to donor disbursement procedures and multiple design-revision rounds — the main reason both lines have slipped by years.

Private PPP is more flexible technically and on schedule. In return, capital cost is higher, there is no revenue guarantee or demand-share mechanism, and leverage can be very high. The Ben Thanh – Can Gio line (proposed by a different investor) shows a reference structure: about 15% equity, the rest from bank borrowings. Applied to a 33 trillion VND line, the debt financing required could reach 20–28 trillion VND. Rising capital cost erodes project IRR before it erodes contractor margins — this is the financial variable retail investors must read before placing long-term bets on the satellite stocks.

The stock map: three timing layers

THACO is not listed, so retail cash flows can only reach the ecosystem via satellite firms. Based on the typical cost structure of a metro line — materials ~20–25% of total investment, civil construction 35–40%, equipment 25%, TOD-area real estate benefiting indirectly — the beneficiary groups split into three timing layers.

Layer 1 — Construction materials (earliest orders, year 1–3). HPG (long steel, HRC), HT1 (cement in the South), KSB (construction stone from Binh Duong mines). This group captures the earliest order flow because every kilometer of tunnel requires massive concrete, steel, and aggregate volumes from the excavation stage onward. A slice of the infrastructure-cycle expectation may already be in the price: HT1 is up 41.3% and HPG up 31.7% over the past year.

Layer 2 — Construction contractors (tracking disbursement progress). CTD (P/E 9.6) has underground-station construction capability; VCG (P/E 3.78) is strong in large-scale general contracting; LCG sits near Long Thanh; C4G carries high leverage at D/E 1.29. This group has room to win sub-contract packages if THACO partitions work, but also carries cost-overrun risk if EPC contracts are not tightly drafted. Reading this group requires attention to the debt structure: high leverage combined with rising capital cost erodes contractor margins.

Layer 3 — Beneficiary real estate (once infrastructure runs). KDH and PDR around the Thu Thiem – Dong Nai axis; NVL (up 63.8% over a year, the strongest reaction in the group) and DXG benefit cyclically. ACV (Long Thanh Airport) is a long-duration beneficiary when the Thu Thiem – Long Thanh line begins operation, even though the short-term price is weak (-20.4% over a year).

A simple framework for retail investors: with a metro line's 4–5 year construction cycle, materials order flow arrives earliest, contractors follow disbursement volumes, and real estate around the line only repices once the infrastructure actually runs. These three timing layers have different cash-flow properties and should not be lumped together as "the infrastructure group".

Risks to monitor

The 270 trillion VND picture is context, not guarantee. Four variables could drag the entire pipeline:

- Legal progress and site clearance. All three project clusters depend on investment approval and compensation. A one-quarter delay sets back the entire order chain — this is the leading cause of the multi-year slippage on metro lines 1 and 2 under ODA.

- Capital cost. High leverage under the BT model is sensitive to interest rates. If corporate borrowing rates cross 10%, project IRR gets eroded fast.

- Underground design. Geological surveys beneath Thu Thiem and the Saigon River crossing may generate cost surprises. The Tham Luong – Ben Thanh ODA line overran budget for similar reasons.

- Orders not formally signed. As of April 2026, most lines remain at feasibility-study or investor-selection stage. Expectations are running 12–24 months ahead of real cash flow.

What to watch in the coming quarters

The 270 trillion VND chain will be confirmed — or slowed — by three concrete events: the April 30, 2026 groundbreaking on Ben Thanh – Thu Thiem (first legal signal), the investment-approval decision for Thu Thiem – Long Thanh expected to be submitted to the National Assembly in 2026, and the commissioning of the THACO Industries rail complex from September 2026 — if on schedule, it confirms domestic manufacturing capability and means THACO can self-supply the technical core.

The THACO story has been flowing through the market for months. What is happening now is not a surprise opening chapter but the closing arc of a long preparation cycle. For retail investors, this is a long-term allocation problem across three timing layers, not a fast-money trade — the confirming signals lie in legal progress on each line, not in a single limit-up session for any one ticker.