On the morning of 22 April 2026, around 4,000 SHB shareholders voted to approve the creation of a wholly-owned single-member bank, 100% domestic capital, inside the Vietnam International Financial Centre (VIFC).Nguoi Quan Sat It is the first time a listed Vietnamese bank has lifted its VIFC commitment from a strategy memo to a signed shareholder resolution.

In the same AGM season, MB went public as a founding member of VIFC-HCMC, with CEO Pham Nhu Anh declaring the bank is "ready to ride the wave" at the hub.Vietstock Chairman Luu Trung Thai earlier laid out a four-pillar strategy: modern financial products, payment infrastructure, new market platforms, and core technology.Vietstock But as of 22 April, no shareholder or board resolution has been disclosed on creating a new VIFC entity. MB's commitment still sits at the executive-direction layer, not a legal decision signed by shareholders.

This distinction is not merely procedural. For investors, it is the first quantifiable signal of execution pace in a brand-new arena.

VIFC is more than an administrative zone

The VIFC operates under National Assembly Resolution 222/2025/QH15 effective 1 September 2025, backed by three guiding decrees 323, 324 and 328/2025/ND-CP.Government The key feature is a relatively self-contained legal zone: IFRS reporting, foreign-currency transactions permitted for most eligible cases, a dedicated court and international arbitration for disputes.

Priority projects inside VIFC enjoy a 10% corporate income tax rate for 30 years, with up to 4 years fully exempt and a 50% reduction for the following 9 years. Experts, managers and investors are exempt from personal income tax through end-2030.Legal Library For a financial institution, the real draw is not the tax rate. It is access to foreign-currency capital flows, the right to raise international funding without additional approvals, and the ability to place products on a legal framework compatible with Singapore or Hong Kong. VIFC-HCMC has attracted more than USD 9 billion in capital commitments in the first two months after its pilot opening.Thuong Gia

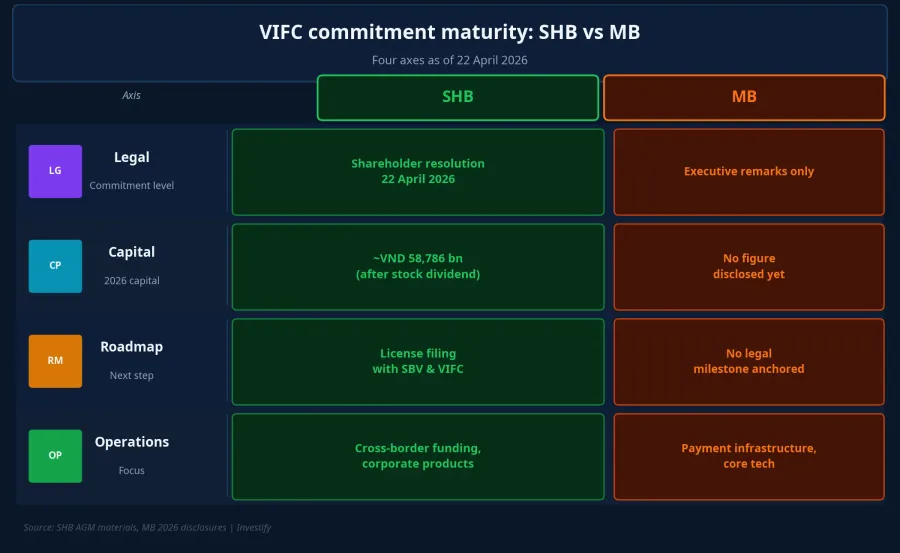

Four axes: SHB is one step ahead of MB

Legal. SHB has a shareholder resolution approving the plan to set up a subsidiary, delegating decisions on name, charter capital, organizational model and personnel to the board. MB has stopped at statements by its chairman and CEO at February and April events, with no published resolution.

Capital. SHB aims to raise charter capital to around VND 58,786 billion in 2026 through a 10% stock dividend combined with prior issuance rounds.Vietnambiz The capital carved out for the VIFC subsidiary will be separated from this equity base after the board decides. Pre-tax profit target for 2026 is VND 17,655 billion (base case, up 18% versus 2025) or VND 19,165 billion (expanded credit case). MB has not disclosed a capital figure for its VIFC entity.

Roadmap. SHB takes 22 April 2026 as its starting point; next steps are licensing filings with the VIFC authority and the State Bank of Vietnam, framed by Decree 323/2025/ND-CP. MB's four-pillar direction is clear but not yet anchored to a specific legal milestone; the next step to watch is MB's AGM and internal disclosures.

Expected operations. Both banks target business lines that the domestic market cannot fully serve: offshore banking for import-export firms, cross-border treasury management, international-standard debt issuance and listing, and participation in carbon markets and regional commodity exchanges. MB leans toward payment infrastructure and core technology, while SHB leans toward cross-border fundraising and corporate-client products.

Beyond SHB and MB, HDBank and Nam A Bank have approved their VIFC participation plans, Vietcombank is bringing the topic to its next meeting, and VietinBank is studying the entity model.Vietstock BIDV, TCB and VPB had not issued separate VIFC disclosures as of mid-April 2026.

Why VIFC is more than a PR story

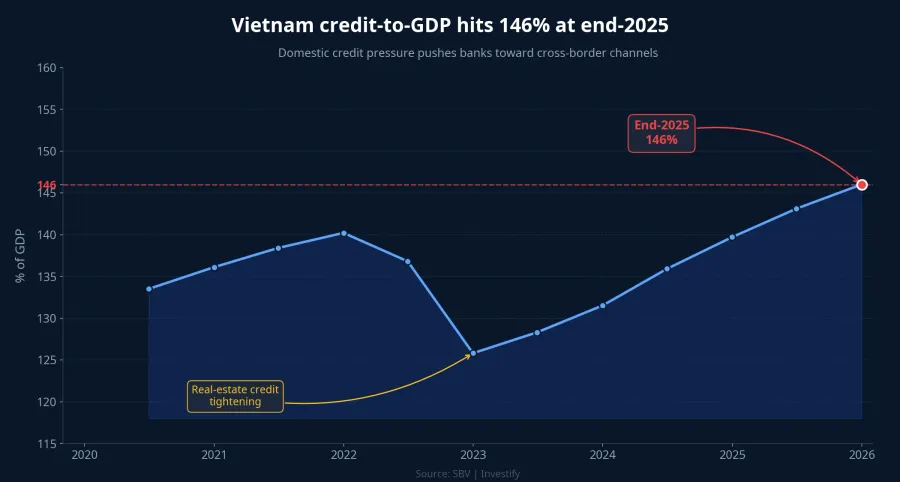

The VIFC equation does not stand alone. In late 2025 and early 2026, Vietnamese banking entered a phase of compressed domestic net interest margin. Credit-to-GDP across the system hit 146% at end-2025, while 2026 credit room is around 15%, down from 19% in 2025.

With domestic margins squeezed and credit-growth headroom shrinking, opening a VIFC entity becomes a structural growth channel rather than a communications story. It lets banks diversify funding in foreign currency, add cross-border fee income, and reach corporate clients that domestic branches cannot serve at scale.

Reading VIFC commitments into stock valuations

Experience from internationally present banks such as DBS, Standard Chartered and HSBC shows P/B tends to improve when a bank grows cross-border fee income, diversifies cheap foreign-currency funding, and raises risk governance to international standards. The valuation premium comes from stable income sources — payment fees, bancassurance, wealth management — not raw credit growth.

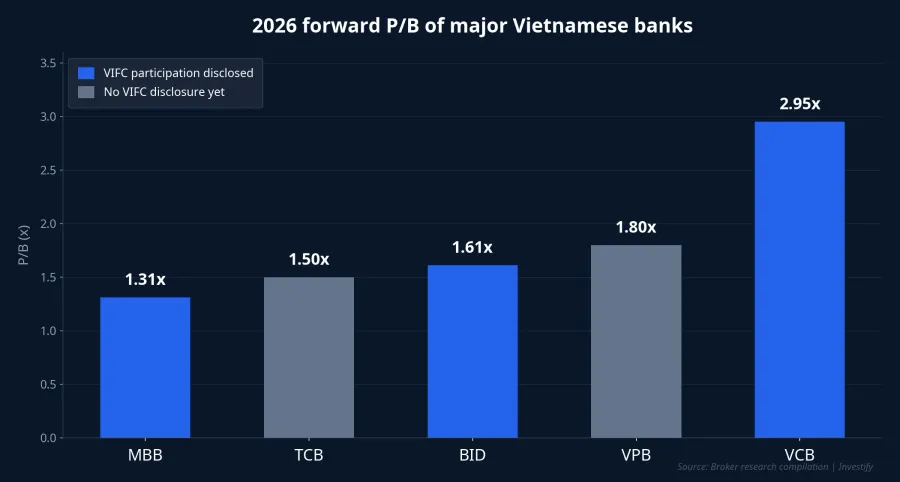

2026 forward P/B: MBB around 1.31x with 2026 ROE near 21.5%; TCB around 1.5x; BID 2025F at 1.61x; VPB target 1.8x; VCB target 2.95x. The spread among this group reflects multiple factors: asset quality, ROE, fee-income mix, foreign ownership ratio. VIFC is not yet the main driver of valuation dispersion, because no entity has launched and no actual income stream exists.

SHB closed 22 April at VND 15,150, unchanged, and MBB at VND 26,300, unchanged. The market has not re-rated either name after the morning announcement, which is reasonable since the VIFC commitment is still 2-3 years from generating real revenue. If the banks actually open VIFC entities and produce fee income from 2027-2028, this could be an additional valuation layer not fully priced in. The 2028-2030 window is when the real impact can be measured.

Execution risk and three milestones to watch

The VIFC legal framework is still being rounded out through guiding decrees. The physical build-out in Ho Chi Minh City's District 1 and Thu Thiem depends on infrastructure progress. A VIFC subsidiary needs time to fill its balance sheet and build an international corporate client base. These variables could extend the 2028-2030 timeline by 1-2 years if progress runs behind plan.

The reasonable analytical frame at this stage is to distinguish three commitment levels: shareholder resolutions (SHB, HDBank, Nam A Bank), AGM discussion items (Vietcombank), and executive statements (MB, others). Commitment maturity differences form the basis for P/B divergence in 2027-2028, but are not the deciding factor for 2026 prices.

Three milestones to watch over the next 6-12 months: SHB's licensing-filing date with the State Bank of Vietnam; MB's AGM and whether a VIFC resolution is tabled for vote; and capital-size disclosures for VIFC entities from both banks. The race has only just started, and the maturity of today's commitments may not line up with the maturity of 2030's profits.