Q1 2026 has a quiet detail that most market dashboards miss: in the same product — open-ended bond funds — US and Vietnamese retail investors moved in opposite directions during the same window.

In the US, retail kept pouring money into bond funds at near-record intensity. According to Morningstar, taxable-bond funds posted their strongest start to a year in many years through Q1, with January's intermediate core bond inflow the second-largest on record and muni-bond AUM crossing USD 1 trillion for the first time in four years.Morningstar MarketWatch read this as a contrarian signal: history says that when an asset class hoovers up retail flows at peak intensity, that often marks a relative top in forward returns.

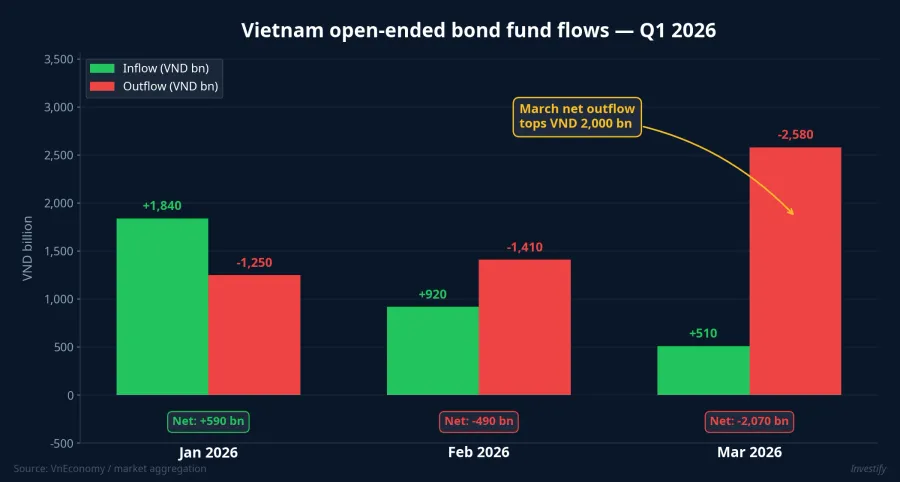

In Vietnam, retail did the opposite. Domestic open-ended bond funds saw net redemptions of more than VND 4,500 billion in Q1 2026 — the second consecutive negative quarter, although the redemption pace had eased 23% from Q4 2025. The pressure concentrated in March, when net outflows topped VND 2,000 billion, up 78% from February.VnEconomy

TCBF lost nearly half its AUM in four months — yet per-unit NAV rose

The center of the redemption wave is TCBF — Techcom Bond Fund, Vietnam's largest open-ended bond fund. In March 2026 alone, TCBF saw net outflows of around VND 1,500 billion, dragging end-Q1 AUM down to VND 6,800 billion, a 44% drop from end-November 2025.VnEconomy

Here is the detail that matters: TCBF's per-unit NAV still rose 2.5% over the same period. Performance, in other words, was not the problem. Investors didn't pull out because they lost money; they pulled out for another reason. DCBF and DCIP — both managed by Dragon Capital and both with AUM above VND 1,000 billion — saw similar pressure.

When a fund still earns positive returns and yet bleeds nearly half its AUM in four months, the story isn't internal performance. It sits outside the fund: a competing channel has become more attractive.

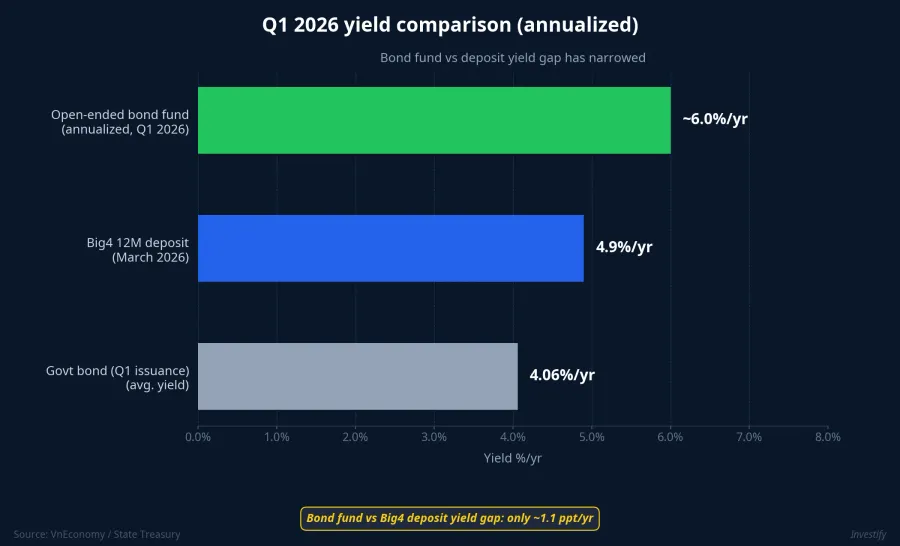

The yield premium over deposits has disappeared

The reason is on the yield comparison sheet. Average open-ended bond fund yield in Q1 2026 ran around 1.5%/quarter, equivalent to roughly 6%/year. Over the same period, deposit rates caught up materially: the average deposit rate ran around 1.4%/quarter, and 12-month deposit rates at the Big 4 state-owned banks reached 4.9%/year in March, up from 4.2% in February.VnEconomy

The yield gap between the two channels has narrowed to about 1.1 percentage points per year. For a Vietnamese retail investor, that incremental 0.1–0.2 percentage points per quarter is not enough to compensate for three things:

- Credit risk of corporate bonds inside the fund's portfolio.

- NAV volatility driven by secondary-market conditions.

- Liquidity friction: T+3 to T+5 redemption versus deposits that can be unwound instantly, particularly when the 12-month Big 4 deposit rate is approaching 5%.

The personal calculus is straightforward: when the premium isn't enough, money naturally drifts to the simpler channel.

Portfolio structure: credit risk weighs more than rate risk

To understand why credit risk is so heavy here, look at the April 2026 portfolio composition of two Dragon Capital funds. DCBF holds 73.8% bonds and 26.2% cash; within bonds, 92.68% is corporate paper, with almost no government bonds. DCIP holds 55.98% bonds and 44.02% cash, with corporate bonds at roughly 78.47% of the bond sleeve.VnEconomy

Both funds concentrate in corporate paper from three sectors: real estate, brokerage, and banking. When retail pulls out, the funds either have to sell into a thin secondary market or hold heavy cash buffers. DCIP holding 44% cash is a clear signal: the fund is prioritizing liquidity over yield. That's not an offensive move — it's a defensive one.

Institutional buyers still absorb government bonds at higher yields than 2025

Within Vietnam itself, a second contrast has appeared. While retail pulls out of open-ended bond funds, institutions continue to absorb government paper: in Q1 2026 the State Treasury raised VND 80,101 billion in government bonds at an average yield of 4.06%/year, 0.8 points higher than 2025.

Two groups, two completely different positions. Institutions (banks, insurers) are locking in long duration at yields above 2025 levels: this is liability-matching, largely insensitive to short-term yield spreads. Retail is exiting corporate bond exposure as the yield premium disappears: a flexible allocation decision driven by short-term conditions. Same market, two time horizons, two allocation logics.

Why the US contrarian signal isn't symmetric in Vietnam

A natural question: if record inflows in the US are a top signal, are record outflows in Vietnam a bottom signal?

The symmetry doesn't hold. Three structural differences are worth putting on the table:

- Product structure: US bond funds mostly hold Treasuries, Investment Grade Corporates, and MBS, with deep liquidity and low credit risk. Vietnamese open-ended bond funds hold mostly corporate paper from a concentrated sector mix, with thinner liquidity and heavier credit risk.

- Retail's alternative: in the US, the substitute for a bond fund is money market funds and equities. In Vietnam, the direct substitute is bank deposits — a channel with no credit risk inside the VND 125 million deposit insurance limit and higher liquidity. When the yield premium disappears, the money doesn't have to travel far.

- Cycle position: US bond fund inflows have run for many consecutive months — late-cycle euphoria. Vietnam's outflows are only in their second consecutive quarter, and the pace is easing by 23% versus the prior quarter. This may be mid-correction, not necessarily a bottom.

In short: the US signal is about an asset class repricing after euphoria; the Vietnam signal is about a product losing its relative-yield story while a safer substitute sits next door. These are two completely different mechanisms.

What role open-ended bond funds still play in a retail portfolio

When the relative-yield story ends, open-ended bond funds don't lose their place. Three roles remain, separate from "yield higher than deposits":

- Mid-tier liquidity layer: between non-term deposits and 12-month time deposits, with T+3 to T+5 settlement and no early-withdrawal penalty.

- Portfolio rebalancing tool: when reweighting fast, a bond fund is a faster vehicle in and out than buying government bonds directly through HNX.

- Periodic accumulation channel for investors with steady cash flow: with small monthly amounts, a fund's transaction costs and minimums are far lower than buying individual bonds.

The watch points for the next two quarters: whether the 12-month Big 4 deposit rate stays around 4.9%/year or keeps drifting up, and whether open-ended bond fund yields widen the spread back. If the gap returns to 1.5–2 percentage points per year, retail flows are likely to come back. If it stays around 1 point, the redemption scenario still has runway.

The reference rate is the deposit — no longer equities or government bonds. Vietnamese retail investors are using the Big 4 12-month deposit as their yield benchmark, and every other fixed-income product will be measured against it.