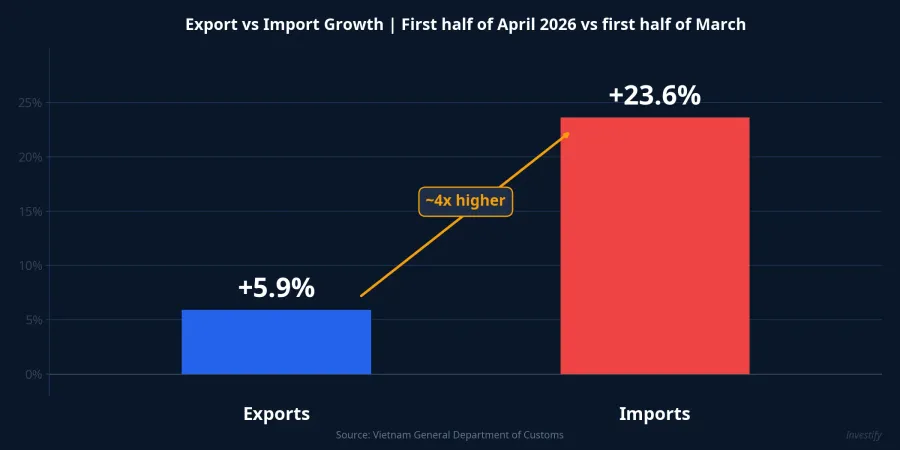

Preliminary data for the first half of April 2026 from Vietnam's General Department of Customs reveals a pattern not seen in a while: imports grew 23.6% while exports rose only 5.9% compared to the first half of March. The nearly fourfold speed gap pushed the trade balance into a USD 4.25 billion deficit for the 15-day period, the deepest of any bi-monthly period since the start of 2026.

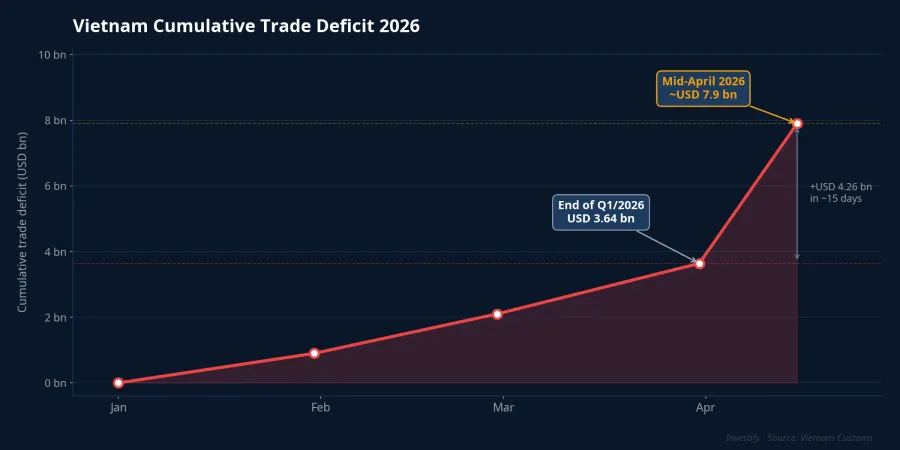

Cumulatively, the year-to-date deficit has reached nearly USD 7.9 billion, already larger than the entire Q1/2026 deficit (USD 3.64 billion). Total trade turnover for the period was approximately USD 47.37 billion, with exports at USD 21.56 billion and imports at USD 25.81 billion.VnEconomy

The big picture shows two stories running in parallel. On one side, VN-Index closed the 20 April session around 1,837.11 points, near its historical peak, reflecting Q1 earnings expectations. On the other side, the underlying macro balance is tightening. This is not a conflict — but both must be read together to understand where capital will flow over the next 4–6 weeks.

Mechanism 1: Production inputs drove nearly all the import surge

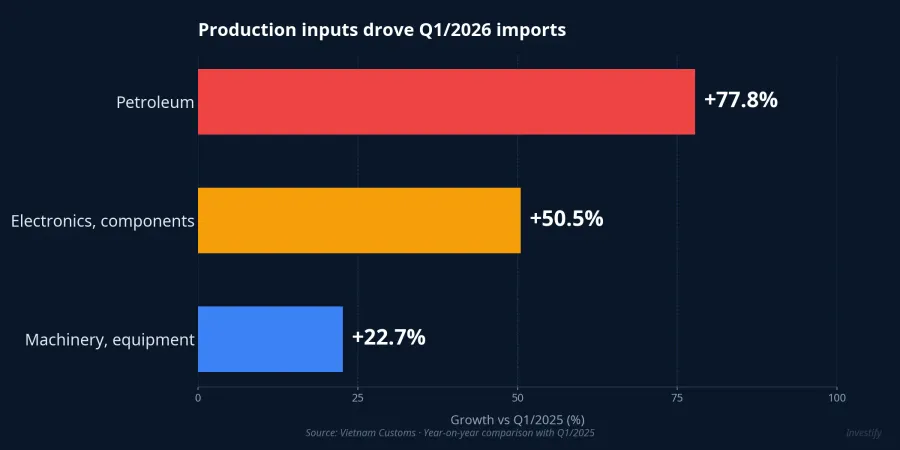

To understand where the +23.6% came from, look at Q1/2026 category composition as the baseline. In Q1, Vietnam's imports reached approximately USD 126.6 billion, up 27% year-on-year. Within this, production inputs accounted for 93.9% of total turnover, around USD 118.84 billion.Vietstock

The three fastest-growing categories were all production inputs: petroleum +77.8% YoY by value, electronics and components +50.5% YoY (about USD 47.57 billion), and machinery, equipment, and parts +22.7% YoY. When the first half of April posted a +23.6% import gain versus the first half of March, it is likely these same categories continued to expand.

A key point about the nature of this flow: production inputs are not end-consumer goods. Once imported, they feed production lines — not retail shelves. The surge in the first 15 days of April therefore reflects manufacturers preparing inputs for the Q2–Q3 order cycle, not a spike in domestic consumer demand. This is a familiar signal when a production cycle bounces off the bottom: imports lead, exports follow with a 1–2 quarter lag.

Mechanism 2: Key exports grow slowly because external demand is still recovering

On the export side, the first half of April grew only 5.9%, more than 17 percentage points below the import pace. The source of this gap lies in the structure of Vietnam's key export goods.

Electronics and components remain the pillar contributing most to export growth, benefiting from the global semiconductor recovery cycle. This group sets the pace. But the other three pillars all run below expectations: textiles and garments see low growth as orders from the US and EU recover slowly, with companies still taking short-term orders and margins yet to improve; seafood holds a mild uptrend driven mainly by shrimp, with average export prices still subdued; agricultural products (rice, coffee, fruit) stay positive thanks to global commodity prices and demand from Asia and the Middle East.

In other words, the export side is in a "electronics pillar ahead, labor-intensive lagging" state. This is the direct source of the near-fourfold speed gap: companies have accelerated raw-material imports, but the export side still depends on end demand in the US and EU — something that cannot be directed from Hanoi or Ho Chi Minh City.

Three other forces also contributed to the outsized import gain, though they are not dominant: global petroleum prices holding at elevated levels pushed energy import values higher; some companies front-loaded purchases out of concern over Middle East logistics tensions; and a base-effect comparison against a softer first half of March.VCCI News

Mechanism 3: USD/VND pressure has not surfaced, but is accumulating

The underlying logic is familiar: a wider trade deficit means higher USD demand for imports than USD supply from exports. With a USD 4.25 billion deficit in just 15 days and a cumulative USD 7.9 billion since year-start, USD/VND should theoretically face upward pressure.

But reality over the past 30 days tells a different picture. USD/VND has held around VND 26,333, essentially flat from the start of the period (range: VND 26,235–26,360). DXY has fallen about 1% per month, passively supporting VND. The State Bank of Vietnam (SBV) has operated in a soft-intervention mode: injecting and withdrawing VND liquidity through open-market operations to keep the VND–USD rate differential attractive, without direct intervention on the central rate within the current narrow band.

That does not mean the pressure has disappeared — it is accumulating. Three factors to monitor for May: the second half of April (if the deficit stays at USD 3–4 billion per period, YTD could exceed USD 11 billion); April CPI after March's 4.65% YoY print; and Q2 remittances after HCMC Q1 remittances fell 15.6% quarter-on-quarter. The SBV is not forced to react immediately, but if this pattern persists for 2–3 more periods, the line between "active stability" and "stability leaning on a weak DXY" will narrow.

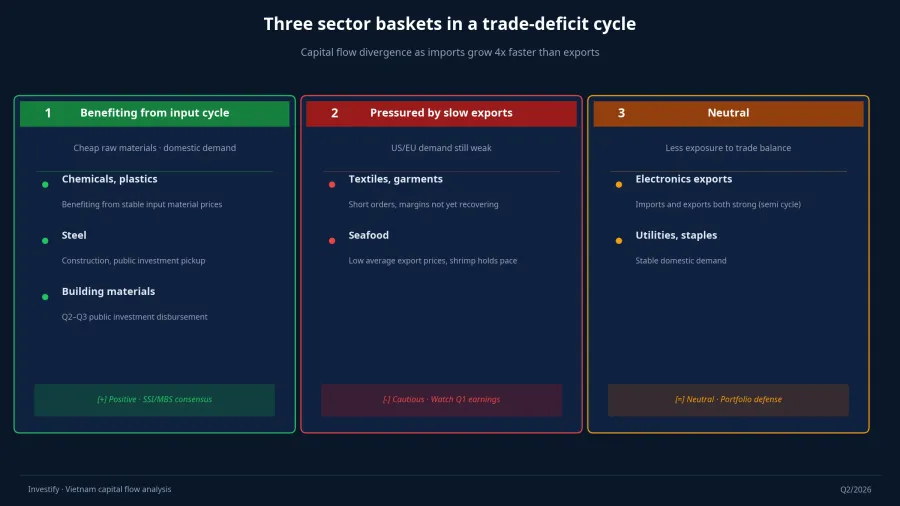

Sector divergence: three baskets to read differently

The pattern of imports outpacing exports is not a broadly negative signal. As consensus among major brokerages holds, it is a signal of manufacturers preparing a new production cycle. But capital allocation will not be even across groups.

Basket 1 — Benefiting from input imports for domestic consumption: chemicals, plastics, cold-rolled steel. SSI and MBS both lean toward rotating capital into this group as input costs stabilize and domestic consumption improves alongside public investment. Illustrative names: AAA, TPC (plastics), VCA, TNS (steel).

Basket 2 — Pressured by slow export recovery: labor-intensive textiles and seafood. Short orders, weak average selling prices, Q1/2026 gross margins expected below multi-year averages. TCM, NTT, GIL, HTG (textiles) and APT (seafood) are examples to watch closely through Q1 earnings for stress readings.

Basket 3 — Neutral: electronics and components exports (strong on both the import and export side through the semi cycle), utilities, and essential consumption. FiinRatings adds that accelerating imports align with firms drawing working capital for H2 orders; VNDirect notes a 1–2 quarter lag before exports improve to match current import momentum.

What to watch over the next 4–6 weeks

With retail investors entering the second week of Q1/2026 earnings season and the index near its historical peak, the USD 4.25 billion deficit does not flip the market's direction immediately. But it does change the reading frame for roughly the next six weeks: VN-Index near 1,837 points reflects Q1 earnings expectations; the USD 7.9 billion cumulative deficit reflects a tightening balance of payments. This divergence suggests sector rotation will play a bigger role than a "rising tide lifts all boats" scenario.

Three specific confirmation markers:

- Second half of April (released early May): if the deficit stays at USD 3–4 billion per period, the USD/VND pressure thesis becomes more concrete, and capital rotation toward Basket 1 (input importers — domestic consumption) will strengthen.

- April CPI: below 4.5% keeps policy room intact; above 4.65% narrows the corridor, and the bond yield curve will react first.

- Q1 earnings for textiles and seafood: the gap between revenue and gross margin will reveal how much stress Basket 2 is actually absorbing before external demand improves.

The big picture: the production cycle imports raw materials first, exports finished goods later. That 1–2 quarter lag is the space where sector divergence plays out. The question worth watching in May is not predicting USD/VND or GDP, but simpler: does the second half of April confirm this pattern, and does CPI close the policy-room window?