On the morning of 21 April 2026, Hoa Phat Group's annual AGM reported Q1 revenue above VND 53,500 billion and net profit of VND 9,056 billion, up 170% year-on-year.CafeF The +170% figure will run across news headlines all day. But for a stock with 300,000 individual shareholders like HPG, reading the composition of that number matters as much as reading the total itself.

Looking at the numbers, the core message is: actual steel business growth this quarter was only about +52% YoY; the rest came from a one-off real estate transaction.

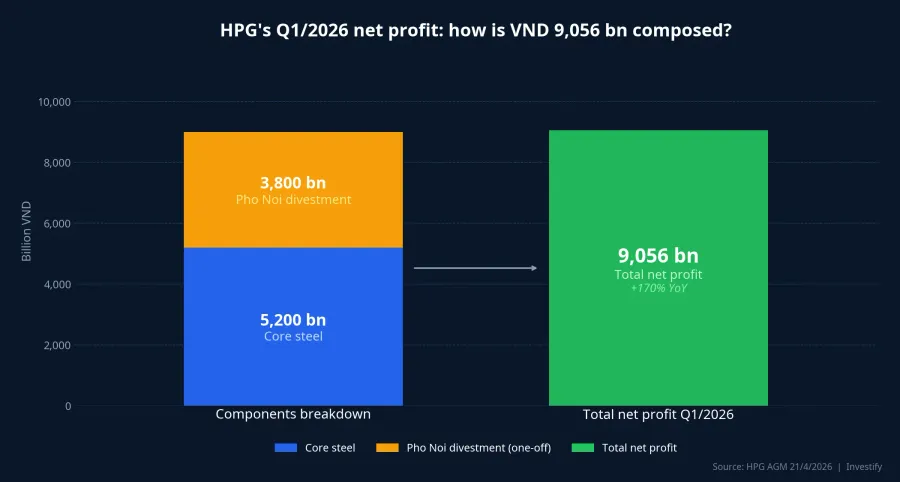

VND 9,056 bn is not a steel number

The official breakdown was disclosed by HPG at the AGM itself, not inferred from financial statements:

- Core operating profit (mostly steel): above VND 5,200 billion, up about 52% YoY.CafeF

- Profit from divesting the Pho Noi urban project (Hung Yen): VND 3,800 billion.CafeF

In other words, of the VND 9,056 billion Q1 net profit, nearly 42% came from a single real estate transaction — not from an operational jump in the steel business. Looking at steel and recurring activities alone, actual YoY growth was +52%. This is still a good number, still showing a clear operational recovery compared to 2024–2025, but far different from the +170% headline.

This is not an accounting error or a misleading presentation: HPG stated it clearly at the AGM. The investor's job is to self-separate layers when assessing "earnings quality" — which portion can repeat in Q2, Q3, Q4, and which portion cannot.

300,000 shareholders: a slice that shocked the Chairman himself

At the AGM, Chairman Tran Dinh Long said that when he learned HPG had about 300,000 shareholders — the largest shareholder count on Vietnam's stock market — he was "stunned".CafeF HPG is nicknamed the "national stock" for exactly this reason: dispersed ownership, a high retail share, and a price that strongly reflects retail sentiment.

On the board, HPG closed the 21/4 morning session at VND 28,950/share, up 1.76% on volume of 72.79 million shares, market cap around VND 222.2 trillion. Morning session liquidity was nearly 3x the previous session (26.6 million) — money flow is reacting directly to the AGM news. With such dispersed ownership, HPG can easily fall into a pattern where retail anchors expectations on the +170% headline rather than the +52% core number.

2026 plan: VND 210 trillion revenue, VND 22 trillion net profit

The Board presented an ambitious 2026 plan to shareholders: revenue of VND 210,000 billion (+35% YoY), net profit of VND 22,000 billion (+42% YoY), and a 2025 dividend of 10% in shares plus 5% in cash, raising charter capital above VND 84,430 billion.CafeF The 2026 dividend is projected at 15%.

Looking at the numbers, the VND 22,000 billion profit plan rests on three operational assumptions. First, Dung Quat 2 has been running stably since late 2025, with actual utilization of 70–90% depending on the broker model. Second, HRC volume grows about 18% per FPTS estimates, with some more bullish reports suggesting total output could rise by as much as ~50% thanks to added capacity and trade defense policies. Third, global HRC prices — which rose from ~USD 940 to ~USD 1,106/ton over the last 12 months — are assumed to edge up another 3–4% in 2026.

The VND 21,000–22,000 billion range is what brokers (MBS, FPTS reports) have estimated for HPG in 2026 under conservative price and volume scenarios. The 22,000 billion plan is therefore not inflated, but it also carries little cushion. Existing risks include rising interest costs as HPG begins long-term debt repayment on Dung Quat 2, and competition from cheap Chinese steel.

Chairman's message: core steel, rail, and caution on real estate

Mr. Tran Dinh Long delivered three noteworthy messages. On the steel cycle, he said growth is supported by Vietnam's public investment push, especially the multi-year infrastructure boom ahead; he stressed that he does not advise shareholders to buy HPG, and asked investors to assess the cycle and demand themselves.

On rail steel and railways, the specialty rail and section steel plant broke ground in late 2025 and is expected to deliver its first products in 2027 with 200,000 tons of rail and 500,000 tons of structural steel capacity, targeting the Hanoi – Quang Ninh rail project. This segment contributes no revenue in the 2026 plan, but each contract announcement during the year will serve as a qualitative signal for a new revenue stream.

On real estate, HPG only invests selectively in highly liquid projects; the Pho Noi transaction falls under opportunistic deal-making, not a signal of aggressive expansion into real estate. The connective message is clear: HPG remains focused on core steel and specialty steel for national infrastructure; the Pho Noi profit this quarter was an opportunity captured, not a new direction. Anyone building an EPS model should not expect a similar VND 3,800 billion item to recur in future quarters.

A reading framework for individual investors

When a blue chip records a large unusual profit in a single quarter, three questions are worth asking before re-anchoring expectations:

- Will core profit sustain the +52% pace in the next quarter? Q2 will no longer carry the VND 3,800 billion from Pho Noi. If core steel continues at about VND 5,000 billion per quarter, steel contributes around VND 20,000 billion for the year — just enough for the VND 22,000 billion plan when other items are added, with very little cushion.

- What are the risks to the 70–90% Dung Quat 2 utilization assumption? If HRC output runs below expectations, full-year net profit could drop below plan.

- Is there still room for global HRC prices to rise 3–4%? Competition from Chinese steel and swings in global industrial demand are variables outside the company's control.

At HPG's current price of around VND 28,950, expectations are largely anchored on core steel sustaining the +52% pace and Dung Quat 2 reaching high utilization. The VND 3,800 billion Pho Noi profit in Q1 should be treated as "one-off" when constructing an expected EPS model — not as a basis for raising the target price in proportion to the +170% print.

Signals to watch

Three signals worth tracking over the next 2–3 months:

- Q2/2026 financial report (released at end of July): the first quarter without the unusual Pho Noi contribution, a clean test for the steel business. If core profit stays around VND 5,000 billion, the +52% YoY thesis is confirmed; if it drops to the 3,500–4,000 billion range, the full-year VND 22,000 billion plan will need adjustment.

- Actual Dung Quat 2 utilization: HPG typically updates this at institutional investor meetings and in financial reports. The gap between 70% and 90% utilization is worth several thousand billion in full-year net profit.

- Global HRC prices: if they hold around USD 1,100/ton or higher, HRC margins have a cushion for the Chinese steel competition scenario.

For a stock with 300,000 individual shareholders, reading the composition of profit matters as much as reading the total. The +170% is the headline; the +52% core is the foundation for anchoring expectations for the remaining three quarters.