On 20 April 2026, the VN30-Index closed at 2,009.04 points, up 20.93 points (+1.05%). It was the index's first close above 2,000 since 2 March 2026 (2,010.75), roughly seven weeks ago. The VN-Index ended the same session at 1,837.11 (+1.10%), with market-wide volume of 690 million shares.

The headline number sounds expensive, but the six-month record tells a different story. VN30's 52-week peak sits at 2,121.13, and from December 2025 to early March 2026 the index held the 2,000-2,100 range for nearly three months. In other words, 2,000 is familiar ground — not a new high. It is a psychological milestone worth watching, but not a moment for an all-in decision.

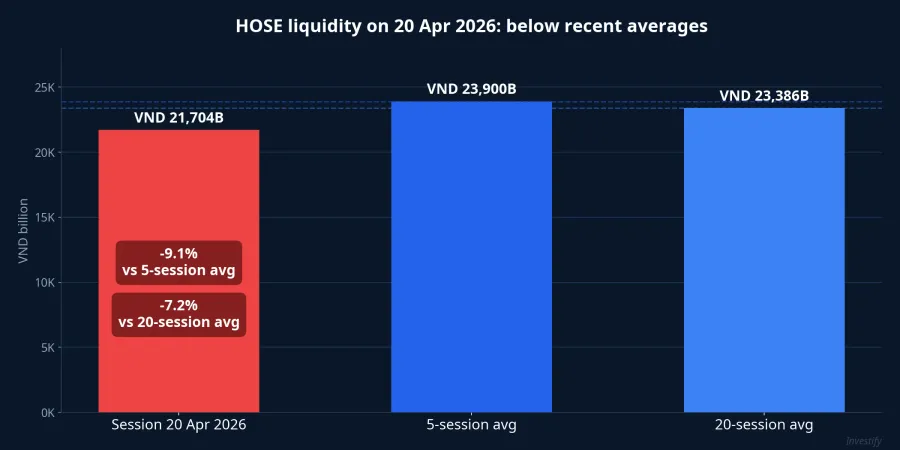

Below the milestone: weak liquidity, rally concentrated in large caps

The real signal is not in the index, but in the liquidity. Matched-order trading value on HOSE for 20 April came in at roughly VND 21,704 billion — 9.1% below the five-session average (~VND 23,900 bn) and 7.2% below the twenty-session average (~VND 23,386 bn). Cash flow was clearly cautious even as the index rallied. This is the classic pattern that brokers describe as "demand at higher prices has weakened."

The gains were concentrated almost entirely in large caps. Within VN30 and related blue chips, GEE led the board at +6.96%, followed by VHM +6.93%, CTD +5.33%, GEX +5.00%, and PNJ +3.60%. On the other side, several heavyweights faced profit-taking: DGC -2.57%, BSR -2.06%, MSB -1.58%, VJC -1.41%. The gainer-to-loser ratio across HOSE was 164/151 — the number of decliners was nearly equal to the number of advancers, meaning the rally did not broaden across the market.

Foreign investors remained net sellers by more than VND 600 billion, concentrated in VIC and VPB. This extends a multi-session net-selling streak, and as long as the intensity does not ease, it remains a structural headwind for the coming week.

The short-term rebound has not yet erased the quarterly drawdown

Looking at the performance numbers, the picture sharpens. VN30 is up 4.33% over one week and 11.74% over one month — a genuinely strong rebound. But on a quarter-to-date basis, the index is still down 3.67%.

Reading these three numbers together tells us that blue chips have recovered most, but not all, of the March drawdown. For investors who added at the March lows, this is good news. For those who had held positions through the correction, portfolios may be approaching break-even, but the quarter has not yet delivered a positive return.

Two views published the same day — not truly in conflict

On 20 April, two lines of commentary were published and read side by side they sound opposed, but stitched together they actually complement each other.

Nguyễn Thế Minh, Director of Investment Banking Services at An Binh Securities (ABS), argues the market is showing signs of a long-term bottom. His case: equities are currently the strongest global asset class and are the priority destination for capital flows in April 2026; the retail share of total US market volume has fallen to 7-8% — the lowest since before COVID, a level historically associated with attractive entry zones for long-term positioning; and the VN-Index has rebounded more than 14% from its 1,591 low on 24 March to 1,817 last Friday. ABS itself notes, however, that the indices are short-term overbought and a correction could occur in the week ahead.Thoi Bao Tai Chinh

On the other side, multiple brokers on the same day recommended caution as the VN-Index approaches resistance. VCBS advises keeping portfolio weights at a safe level and avoiding chasing stocks that have already run hard; SHS sees correction pressure emerging after the sustained rally from the 1,600 zone; SSI and ACBS also flag short-term risks amid weakening liquidity.Tuoi Tre

The two views do not really conflict. ABS is talking about a long-term bottom signal in a multi-quarter frame, but still acknowledges short-term correction risk. The VCBS/SHS/SSI cluster focuses on short-term caution at resistance. The common message is the same: this is not the moment to chase the rally.

Three allocation questions before the week of 21-25 April

Rather than asking "will next week go up or down" — a question almost nobody answers correctly on a consistent basis — retail investors should ask three concrete allocation questions.

Question 1: The equity slice that is up 20-30% from the March lows — hold, reduce, or partial take-profit?

VN30 is up 11.74% over one month, and many blue chips have returned to pre-correction prices. The decision frame has three branches: hold if the fundamental thesis (Q1 earnings, sector outlook) still stands; take partial profits (around 20-30% of a position) on names that have hit technical resistance or have outrun the index rally; and park the proceeds in a waiting channel rather than redeploying immediately into a new name. The "take partial profits, avoid chasing" message from brokers aligns with this logic.

Question 2: How much cash should sit on the sidelines waiting for a correction?

If the base case is a short-term correction before the uptrend resumes — the consensus position of both ABS and the cautious cluster — the cash sleeve needs to be large enough to redeploy when the market discounts 3-7%. For medium-term investors, 20-30% of the portfolio is a reasonable reference. Lower leaves too little to exploit a pullback; higher carries meaningful opportunity cost if the correction does not arrive.

Question 3: Where should waiting cash sit so its opportunity cost is not excessive?

Three common channels, suited to different time horizons:

- 6-12 month term deposits at large banks: reference rates of roughly 3.6-4.7% at Vietcombank/BIDV and 4.5-5.0% at Techcombank/MB/ACB — good liquidity, low risk, appropriate for 3-6 month waiting cash.

- Open-ended bond funds: 12-month NAV change at major funds (DCBF, VFF, VCBF-FIF, VNDBF, MBBOND) ranges around 6.2-7.3% — suitable for 6-12 month waiting cash with acceptance of small NAV volatility.

- Fixed-income products on fintech platforms: reference yields of 8-11% p.a. — higher than deposits, suitable for stable capital willing to accept a lock-up period.

One important caveat: deposit rates are currently at low levels and could rise 0.5-1 points during 2026 per the published FiinRatings forecast. Locking in excessively long terms at this point is therefore not an optimal choice.

What to watch in the week of 21-25 April

Four factors will determine whether 2,000 becomes a durable base or just a failed retest:

- Does VN30 hold above 2,000 or get pulled back below it — the psychological reversal level. Losing this mark in the first sessions of the week would confirm short-term correction risk.

- Does HOSE liquidity bounce back above VND 23,000 billion per session or keep contracting — the confirming or disconfirming signal for the rally. An index rising on weak volume is not a reliable uptrend.

- Q1 2026 earnings season is about to peak, with reports from state-owned banks, Vingroup, and Hoa Phat. A "sell-the-news" risk is real if results are already priced in.

- Does foreign net-selling ease or continue — 20 April saw more than VND 600 billion in net outflows, concentrated in VIC and VPB. A prolonged net-selling streak is a structural drag.

The 2,000-point mark on VN30 does not by itself answer the buy-or-sell question. It simply reminds investors that the right moment has come to revisit the allocation questions: how much to take off the table, how much cash to hold, where to park the waiting portion. The two views published on the same day agree on one thing — this is not the moment to chase. Q1 earnings reports over the coming week will provide concrete data to adjust positioning.