The 2nd session of the 16th National Assembly (20-24 April 2026) is reviewing draft amendments to the VAT Law and the Personal Income Tax (PIT) Law under fast-track procedure. The headline for Vietnam's 5 million household businesses: the Ministry of Finance proposes raising the tax-exempt revenue threshold from VND 500 million to up to VND 1 billion per year, while delegating the Government authority to adjust the level over time instead of fixing it in the statute.Thanh Nien

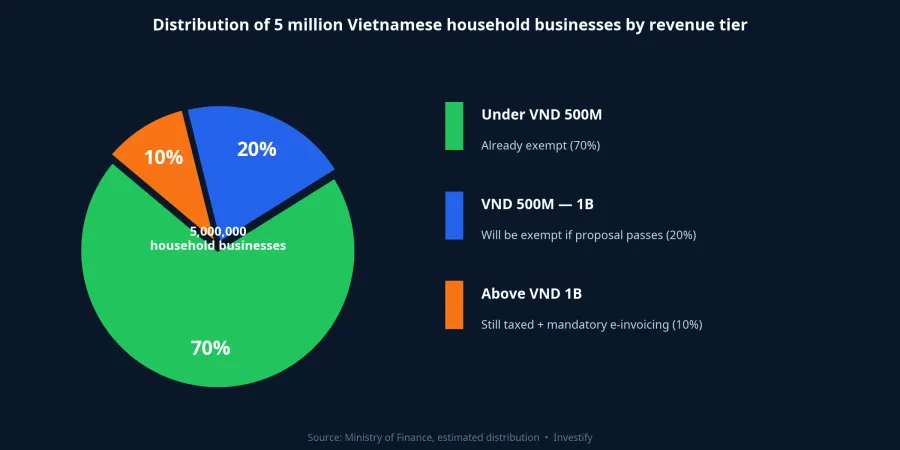

Simply put, for a household business with VND 800 million in annual revenue in the distribution sector, the change means tax liability drops from about VND 9.5 million to zero. Nationally, this proposal could move roughly 90% of household businesses into the exempt bracket based on the estimated revenue distribution: 70% of households are below VND 500 million (already exempt), 20% fall in the VND 500 million to 1 billion band (would be exempt if the proposal passes), and the remaining 10% are above VND 1 billion.PLO

This article walks through three checkpoints that household business owners and individual investors with side businesses should review before the amended law is voted on.

Checkpoint 1: Current VND 500M threshold vs proposed VND 1B — the practical gap

In plain terms, household businesses are today classified into four revenue tiers. Tier 1 (under VND 500 million/year) is exempt from both VAT and PIT. Tier 2 (VND 500 million — 3 billion) pays tax calculated directly on revenue at an industry-specific rate. Tier 3 (VND 3-50 billion) and Tier 4 (over VND 50 billion) gradually move to a profit-based calculation.

Revenue-based tax rates by industry (under the current circular):

| Industry group | VAT | PIT | Total |

|---|---|---|---|

| Distribution, supply of goods | 1% | 0.5% | 1.5% |

| Manufacturing, transport, construction (with materials) | 3% | 1.5% | 4.5% |

| Services, construction (no materials) | 5% | 2% | 7% |

| Asset leasing, insurance agency | 5% | 5% | 10% |

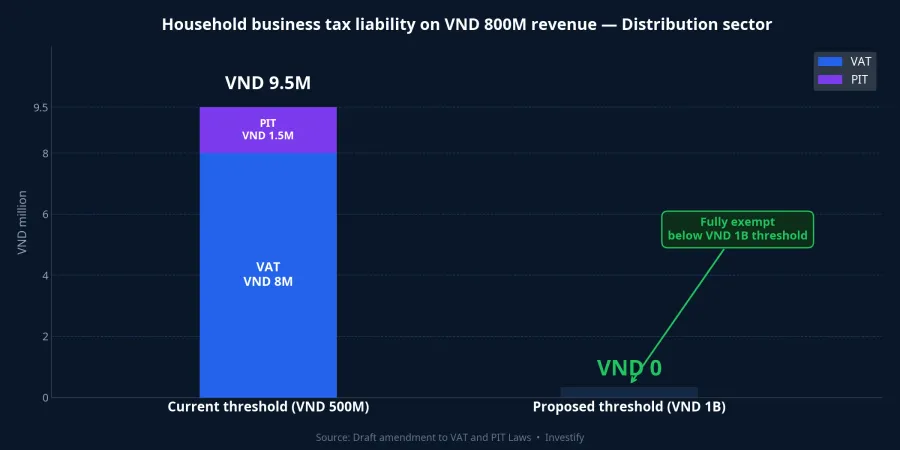

A concrete example with a household at VND 800 million/year in distribution. Under the current threshold, VAT is VND 800M × 1% = VND 8M, PIT is (800 - 500) × 0.5% = VND 1.5M, for a total of VND 9.5 million/year. If the threshold rises to VND 1 billion, the VND 800M revenue sits below it, the household is fully exempt, and the total becomes VND 0.

VND 9.5 million may not sound large, but this is distribution — the lowest-rate bracket. At the same VND 800M revenue, a household in services (5% + 2%) could owe roughly VND 25-28 million, and a household in asset leasing (5% + 5%) could reach about VND 40 million per year. Savings therefore differ substantially by industry.

Worth noting: this is still a proposal before the National Assembly, not law yet. The "delegate to the Government" mechanism means the specific VND 1 billion figure could be adjusted down to VND 700 or 800 million during review.Tuoi Tre Effective date is expected to align with the 2026 tax year if passed.Vietstock

Checkpoint 2: The VND 1 billion line is a double boundary

Something many owners have not noticed: the VND 1 billion mark is not only the proposed exemption threshold — it is simultaneously the mandatory e-invoice boundary. Since 1 June 2025, under Decree 70/2025/ND-CP, household and individual businesses with annual revenue of VND 1 billion or more are required to use coded e-invoices generated from a cash register, with data transmitted directly to the tax authority. According to the tax sector, about 270,000 household businesses fall under the first-wave application.Government

In addition, certain sectors must use cash-register e-invoices regardless of revenue, including restaurants, hotels, food & beverage, supermarkets, shopping centers, passenger transport, arts/entertainment/recreation, cinemas, and personal services.MISA

Real-world compliance cost is much lower than common fears suggest. Invoice fees run about VND 30-50 per slip (Viettel, VNPT, Minvoice, Fast), so a household issuing 5,000 invoices a year spends only about VND 150,000-250,000 on invoices. Sales and filing software (MISA, Sapo, KiotViet) costs around VND 100,000/month after promotions, with many plans offering 12-24 months free for newly registered households. Learning time is only 4-8 hours, and local tax offices run free "hand-holding" support programs.

The practical result is that VND 1 billion becomes a clear financial milestone. Households below VND 1 billion (if the threshold is raised) simultaneously pay no VAT/PIT and are not required to use e-invoices. Households above VND 1 billion must both pay tax and switch to e-invoicing. This directly affects your wallet: if side-business revenue (online sales, property leasing, small services) is approaching VND 1 billion, now is the time to plan ahead — whether to register as a formal household business or convert to a micro-enterprise, where the Ministry of Finance is also proposing a VND 3 billion exemption threshold.

Checkpoint 3: Where freed capital from tax savings should go

Assume the proposal passes and an average household saves VND 5-30 million per year in tax (depending on industry and revenue). Over 5-10 years, the accumulated pool could reach VND 50-300 million — enough to warrant a plan. With the policy rate held at 4.5%/year and the deposit rate environment easing into early 2026, three channels are common options for capital of VND 20-200 million.

Bank deposits — suitable for an emergency fund. 12-month deposit rates in early 2026 range from 5.8% to 7.6% depending on the bank. Advantages: low risk, with deposit insurance up to VND 125 million per person per bank. Drawbacks: early withdrawal earns only the demand-deposit rate (~0.1%), and real yields may lag inflation when CPI sits at elevated levels.

Open-ended bond funds — flexible liquidity. Vietnamese open-ended bond funds currently yield around 6-8%/year on average, with T+2 to T+5 liquidity and no early-redemption penalty. Suitable for capital without a clear use-date, where the goal is a yield slightly above deposits while keeping stability. The main risk is the credit quality of the bonds held, so reading the fund's portfolio composition before buying matters.

Equity fund SIP — the long-term channel. A Systematic Investment Plan (monthly periodic contribution) averages the entry price and dampens the impact of volatility. A reasonable long-term expectation for Vietnamese equity funds is 10-12%/year, even though a few funds posted 2024-2025 performance above 30%. This channel suits goals of 3-5 years or more, and is not suitable for capital needed within 12 months because short-term drawdowns are possible.

Suggested allocation by capital size (for reference, not individual investment advice): VND 20-50 million should prioritize online savings and/or a bond fund for liquidity and safety. VND 100-200 million can balance 50% savings, 30% bond fund, 20% equity-fund SIP — stable with a long-term growth slice. For busy household business owners, an automatic monthly SIP removes the burden of tracking markets.

Three things to do while the proposal is under review

First, identify your tier based on the most recent year's revenue: under VND 500 million (already exempt), VND 500 million — 1 billion (would be exempt if the proposal passes), or above VND 1 billion (still taxed and required to use e-invoicing).

Second, if revenue is near VND 1 billion, start exploring e-invoicing software and cash-register systems now. Take advantage of the 12-24 month free plans from MISA, VNPT, and Viettel to bring startup cost close to zero, avoiding a scramble if revenue crosses the threshold mid-year.

Third, plan for the freed capital before it gets absorbed into everyday spending. You do not need to move everything into investment channels — keep 3-6 months of living expenses as an emergency fund in savings or a bond fund, and only direct capital with a 3+ year horizon into an equity-fund SIP.

The proposal is under review at the 20-24 April session and is not yet a final document. The task now is to follow the session, review 2025 revenue records, and prepare for both scenarios — passed or not passed within the year. The final outcome will answer whether the exemption will be VND 700 million, 800 million, or 1 billion, and from which tax year it takes effect.