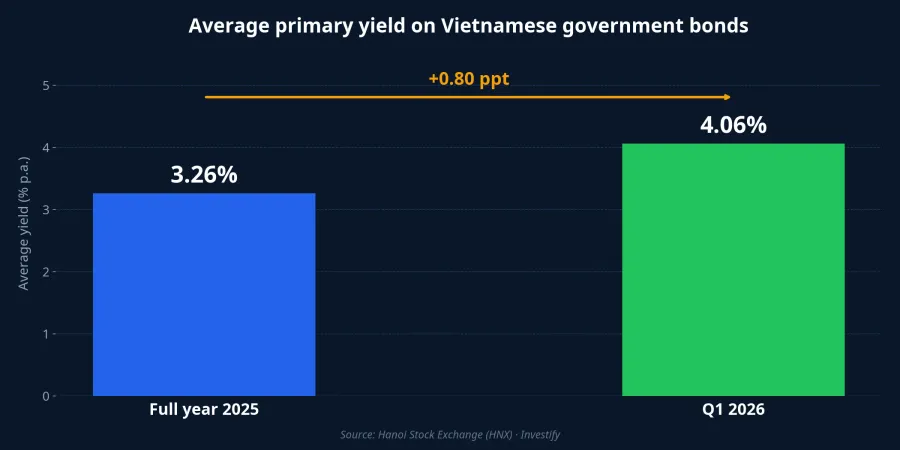

Through 11 auction sessions in Q1 2026, the Vietnam State Treasury raised VND 80.101 trillion in government bonds, hitting 72.8% of the quarterly target and 16% of the full-year 2026 plan of VND 500 trillion. The average primary yield landed at 4.06% p.a., up 0.8 percentage points from the full-year 2025 average.Bao Chinh Phu

For most retail investors, government bonds (TPCP) are a market they don't trade directly. But 4.06% is the hidden pricing frame behind nearly every personal finance decision: bank deposit rates, open-end bond fund yields, and equity discount rates. The listed TPCP market reached over VND 2.6 quadrillion at end-February 2026 — larger than many HOSE sector caps combined.VOV

Understanding why primary TPCP yields moved 0.8 points in a year is understanding why 12-month deposits, bond funds, and equity discount rates are all repricing in sync. The big picture shows Vietnam's rate cycle is in an up-phase, and the three mechanisms below are the data basis for that view.

Mechanism 1: Bank liquidity squeezed, primary yields dragged higher

TPCP coupons aren't set by the Treasury; they're set by the bidders — mainly commercial banks, insurers, and some investment funds. When the funding cost of these bidders rises, the yield they demand when auctioning TPCP rises with it. This is the first transmission channel retail needs to see.

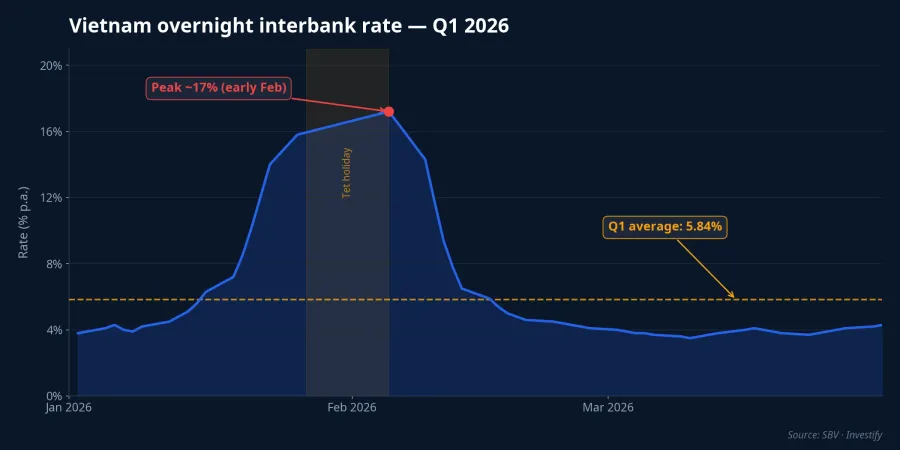

Q1 2026 was the most volatile interbank liquidity quarter in many years. The average overnight rate for the quarter reached 5.84% p.a., up 1.27 percentage points from 2025, and briefly spiked near 17% p.a. in early February — unusually high.Bao Chinh Phu

The squeeze came from three overlapping sources: end-January tax payments, pre-Tet cash demand, and cash flowing from the banking system into the Treasury's account as TPCP issuance accelerated. The State Bank pumped sizeable liquidity through open market operations to cool things off, but volatility lasted nearly the whole quarter.

When bidders are borrowing overnight at 6-8% — and sometimes 17% — they cannot accept a 10-year TPCP at below 4%. Primary yields in the auction records adjusted up 0.11-0.4 percentage points across 5, 10, and 15-year tenors inside Q1. This is not a random move; it is the direct consequence of short-term funding costs.

Mechanism 2: Heavy public-investment funding need, Treasury pays up

The 2026 issuance plan is VND 500 trillion, but Q1 only cleared 16%. The remaining three quarters must raise roughly another VND 420 trillion — a large figure in a liquidity-tight system. For Q2 2026 alone, the Treasury has announced auction calls of around VND 110 trillion, concentrated on the 10-year tenor.CafeF

This continuous supply pressure forces the Treasury into two concessions. First, effective maturity shortening: all Q1 awards clustered in the 5-15 year band, while 20-30 year tenors didn't attract enough demand. The average issued maturity reached 10.02 years and the portfolio's residual maturity held at 8.44 years — shorter than the government's preferred long-duration debt profile. Second, paying more: the 4.06% average is the highest in several years for equivalent tenors.

The 20-30 year gap is not because the market dislikes Vietnamese government bonds. It is because the bidders — mainly banks — are unwilling to lock in a 30-year funding cost when they themselves don't know where their own yield curve will sit in 5-10 years. This is a clear signal that rate expectations remain unsettled, and that even the institutional side is keeping distance from long-term commitments.

Mechanism 3: TPCP is the hidden benchmark for deposits, funds, and equities

This is the most important layer for retail investors. TPCP yields are not the rate of some niche market; they are the risk-free rate — the reference every other channel prices risk premium against. When this reference moves, the entire financial ecosystem moves with it.

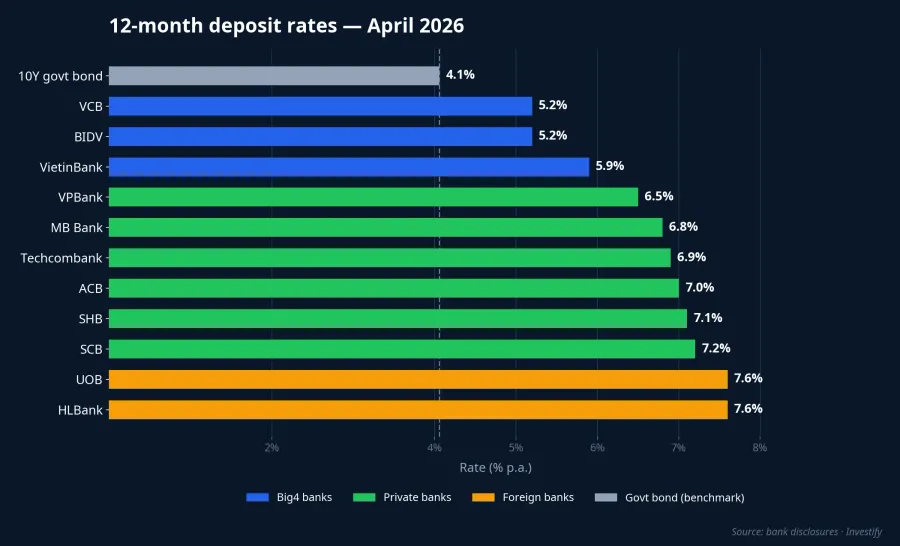

Bank deposits. April 2026 12-month deposit rates at the Big4 range 5.2-5.9%, with VietinBank at 5.9% after a 0.7-point hike.CafeF Listed private-bank rates sit at 6.5-7.2%,Techcombank and some foreign banks like UOB and HLBank push the ceiling to 7.6%.Cake

Against a 10-year TPCP at 4.06%, the 1.2-3.5 point spread reflects the credit and liquidity risk premium on bank deposits. When TPCP is still rising, deposit rates typically follow with a lag — something to factor in before locking in a long-tenor deposit. The Big4 versus private-bank spread (around 1.5-2.4 points) is a genuine liquidity risk premium, not a "free higher rate."

Open-end bond funds. 12-month NAV returns to mid-April 2026 diverge by asset structure. Pure bond funds like VCBF-FIF and VFF logged around 7% p.a., consistent with fixed-income behavior in a rising-rate environment. Liquid fund VLBF, which holds a large cash weight, sits near 4-5%. In a rate-up cycle, bond funds face a double pressure: rising coupon yield is good for new holdings, but prices of existing bonds in the portfolio fall — the reason many funds show yields below 12-month deposits at private banks.

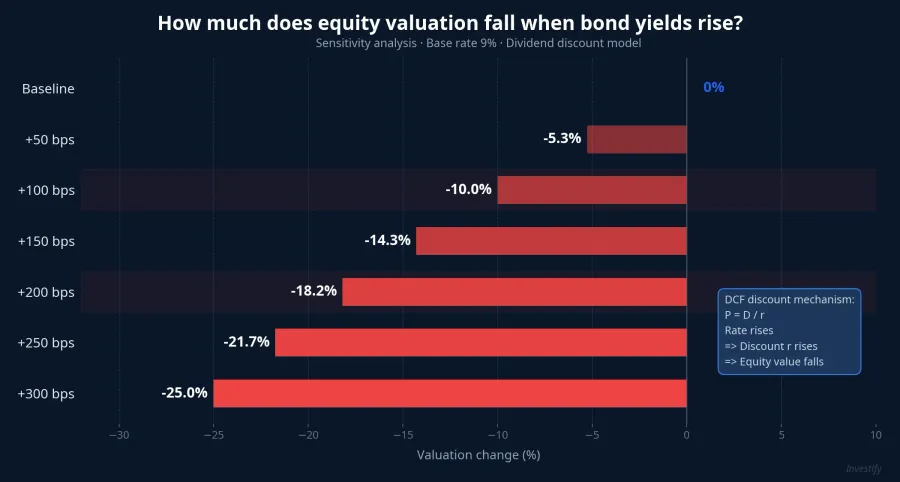

Equity valuation. 10-year TPCP yields at the start of 2026 already edged above 4.3% p.a. on a monthly average. When this risk-free baseline is higher, the required return on equities has to rise too, compressing market P/E.

Sensitivity math shows that if TPCP yields rise a sustained 100 basis points, equity valuations may drop around 10%; 200 basis points maps to roughly 18%. These are reference parameters, not forecasts, but they explain why VN-Index is trading around 1,817 points — below early-year highs — even though Q1 bank earnings are not bad. Part of the pressure comes from the discount rate, not just corporate profits.

What does retail read from 4.06%?

The 4.06% number doesn't tell the market what to buy or sell. But it sets the pricing frame that every personal finance decision is running inside. Evidence from the three mechanisms above points in one direction: Vietnam's rate regime is in an up-phase, not a down-phase.

First, with primary TPCP yields up 0.8 points in a year and Q2 supply still heavy at VND 110 trillion, the "rates will fall soon" expectation has no data basis to support it. This does not mean rates will keep rising indefinitely, but betting on a rapid cut scenario over the next 3-6 months runs against what the primary market is pricing.

Second, the deposit-rate spread between Big4 and private banks reflects a real liquidity risk premium. Private banks are paying more because they urgently need medium-to-long term funding, as MB CEO Pham Nhu Anh put it bluntly: "the market is fundamentally short on cash." For investors prioritizing absolute safety, this spread is compensation for accepting a different liquidity profile — not a freebie.

Third, open-end bond funds and fixed-income products provide indirect exposure to the TPCP rate wave without requiring large trade sizes. Each product group has distinct behavior in a rising-rate environment, and allocation choices depend on each investor's liquidity needs and tolerance for price volatility.

Which scenario has higher probability — rates continuing up, or starting to stabilize? The Q2 2026 auction results, especially the early-May session, will answer more directly than any analyst report. Three signals to watch: whether 10-year winning yields break above 4.2%, the bid-to-offer ratio, and whether 20-30 year tenors recover demand. That's where the data basis for 2026 rate expectations will show up first.