The "From boom to selectivity" report released by FiinRatings on April 19, 2026 places the banking sector at an inflection point.FiinRatings The growth cycle built on cheap credit has closed. From here on, each bank's profit will be determined by its own structure, not by the sector tide.

The timing is deliberate. The report lands the week before Q1/2026 earnings season peaks (April 20-24), when VCB, BID, CTG, ACB, TCB, and STB all release results. FiinRatings' message for investors walking into earnings week is clear: don't look at headline numbers, look at structure. To read the structure, FiinRatings offers a three-layer framework — capital strength, liquidity, and asset quality.

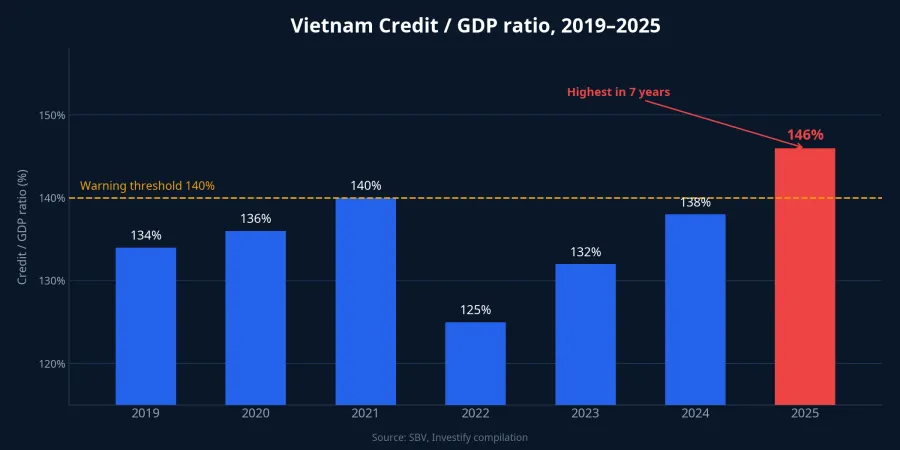

Why "selective" now: Credit/GDP hits 146%

The root number that explains everything else in the report is system-wide credit-to-GDP, which reached around 146% at end-2025.FiinRatings That is high relative to regional lower-middle-income peers, and it reflects a multi-year reality: credit has expanded faster than the real economy.

Once this ratio pushes clearly past the 140% threshold and continues to climb, the regulator has no choice but to throttle credit growth to contain systemic risk. The 2026 credit growth target is therefore set at around 15%, meaningfully below the roughly 19% recorded in 2025.FiinRatings The direct consequence: credit "room" becomes a scarce resource, and the State Bank of Vietnam (SBV) will allocate it toward banks with strong capital and healthy asset quality, steering flows into production and business rather than property and unsecured consumer lending.

This is the mechanism that explains why divergence will show up in Q1/2026 rather than late in the year. The system has been living with capped credit growth since the first quarter: banks that capture room will win, and banks that don't get more room will have to defend earnings by improving margins — not an easy task while deposit rates are drifting up. FiinRatings' three-layer framework is therefore not a theoretical construct; it is a practical map for reading the upcoming earnings season.

Layer 1: Capital strength — the threshold for room allocation

FiinRatings ranks capital strength as the first differentiator for a practical reason: to receive larger credit room when the total pie shrinks, a bank must prove its capital buffer can absorb risk. The report distinguishes two groups with fundamentally different capital-raising mechanics.

State-owned banks (VCB, BID, CTG) rely mainly on Tier 2 supplements — issuing capital-raising bonds, bounded by Basel III limits. That is why VCB and BID have for years required special approvals from the government to raise Tier 1 capital via stock dividends or private placements to strategic partners. Large private banks (VPB, TCB, MBB) are more flexible, with access to ESOP, issuance to foreign partners, international bonds, and higher retained earnings.

VPB's Q1/2026 numbers hint at the capital health of the large-private cohort: consolidated CAR of approximately 14% — a strong level among joint-stock commercial banks.VPBank When reading Q1/2026 statements next week, the indicator to watch is not CAR's absolute level but whether CAR has improved versus end-2025. Banks with improving CAR (not flat) will have the room to request additional credit allocation in the second half — they are the direct beneficiaries when the SBV allocates by quality.

Layer 2: Liquidity and NIM — margin compression underway

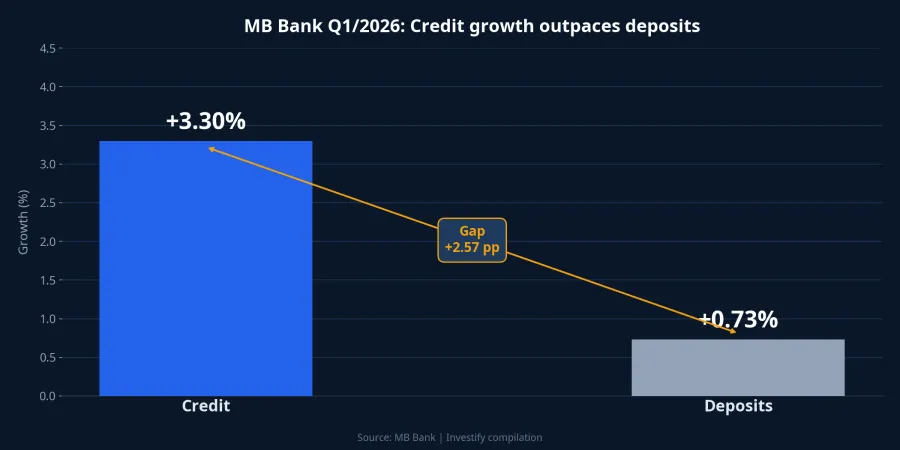

The second layer reflects a quieter compression, but Q1/2026 data already shows it plainly. At MB, management disclosed at the April 18 AGM that Q1 credit grew 3.3% to around 1,146 trillion VND, while deposits grew just 0.73% to around 1,070 trillion VND.CafeF MB's management stressed this was not a single-bank phenomenon but a system-wide pattern.

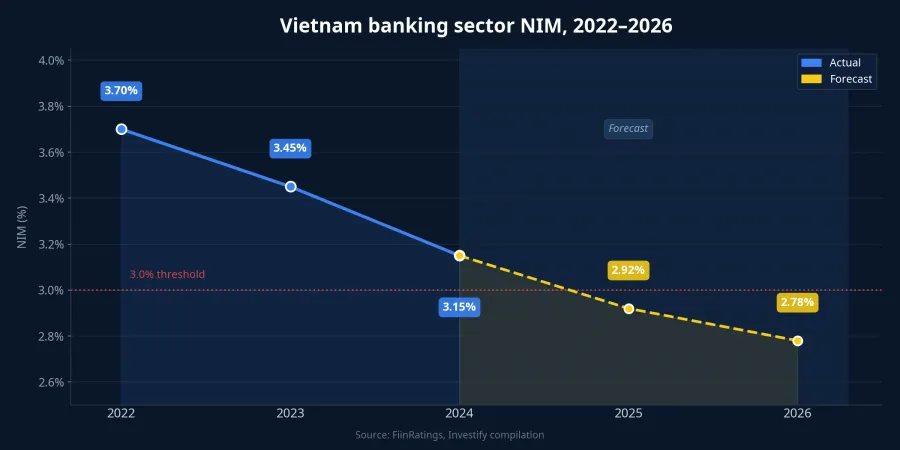

The impact on NIM is direct. When credit grows faster than deposits, a bank has two options: raise deposit rates to attract household and corporate funding, or borrow in the interbank market and issue valuable papers. Either choice lifts funding costs. FiinRatings estimates sector-wide NIM dropped to around 2.9% at end-2025 and will stay below 3% through 2026.FiinRatings

Within that picture, two liquidity indicators become decisive. CASA (ratio of demand deposits) — high CASA means low funding cost and no need to chase deposit rates. LDR (loans-to-deposits) — low LDR means a bank still has room to lend without sourcing more funds. MB reported LDR of around 79%, clearly below the industry average; VPB reported consolidated LDR of around 82.7%, also in safe territory.CafeF Smaller banks with LDR already past 100% will have to actively raise deposit rates or sell loans to source funding — the first group to feel NIM compression.

Layer 3: Asset quality — the lesson from VPB consolidated

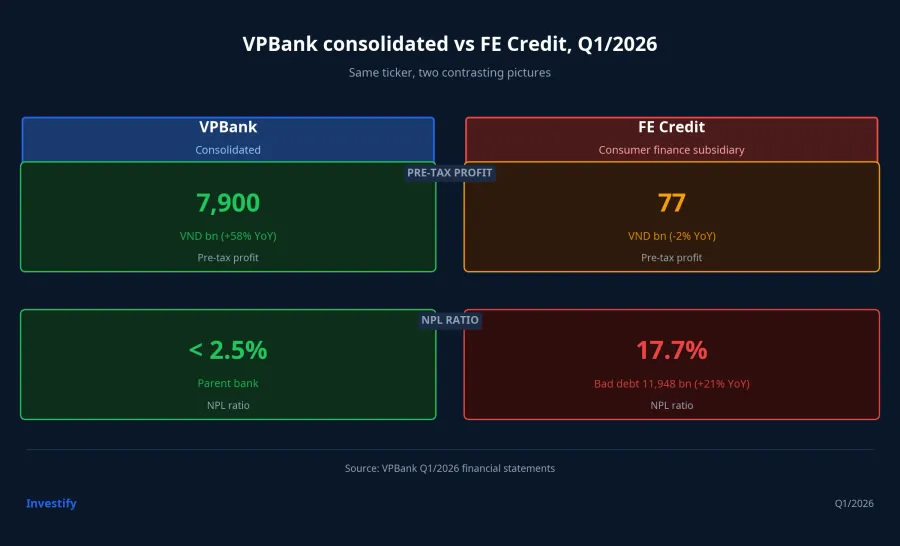

The third layer is where the three-layer framework proves its value most clearly, and it is also the layer where headline numbers can mislead. Take VPB Q1/2026 — one ticker, two contrasting pictures.

The parent bank VPBank reported consolidated pre-tax profit of around 7,900 billion VND, up 58% YoY, with credit outstanding exceeding 1 quadrillion VND (+10.2% YTD); net interest income reached 16,960 billion (+26.7%), fee income nearly doubled, and standalone NPL stayed below 2.5%.VPBank This is a parent bank benefiting from selective credit structure, focused on SMEs, large corporate clients, and affluent retail.

In the same Q1/2026, consumer-finance subsidiary FE Credit earned just 77 billion VND, down 2% YoY; bad debt reached 11,948 billion VND (+21% YoY), NPL rose to 17.7%; interest expense grew 21% and exceeded 1,000 billion VND.Elibook The low-income segment is still working through post-Covid bad-debt cleanup, and rising funding costs further erode whatever margin remains.

This is why FiinRatings insists on reading by sub-segment rather than headline. VPB consolidated NPL is much lower than FE Credit because FE Credit is only a small share of total group assets. But provisioning pressure from FE Credit still materially affects group-wide CAR and asset quality: in Q1/2026, VPB booked 7,669 billion VND in risk provisions, up around 15% YoY.VPBank The same principle applies to other groups with consumer-finance or securities subsidiaries: separate "the healthy parent bank" from "the subsidiary under pressure" to avoid misjudging stock quality.

Three indicators to watch during April 20-24

The week of April 20-24 is peak Q1/2026 reporting. VPB and MB have already disclosed numbers; VCB, BID, CTG, ACB, TCB, and STB will follow. When the reports land, three indicators matter most under the FiinRatings framework:

- CAR and equity growth. Banks with improving (not flat) CAR are the ones that will secure additional credit room in H2/2026.

- CASA and LDR. Rising CASA and stable LDR below 85% signal a bank that does not need to chase deposit rates — NIM is protected.

- NPL by segment. Separate the parent from the subsidiary. A stock that looks "clean" at the group level can still hide subsidiary risk that investors miss if they only read headline figures.

The "selective" phase does not mean banking has lost its appeal. It means the broad-basket trade of 2024-2025 is no longer enough. From Q1/2026 onward, the value of bank analysis lies in reading structure, not headlines. The decisive signals will appear in next week's reports: whether CAR is improving, whether LDR is being squeezed, and whether subsidiary NPL is quietly building. Those three questions, not headline profit, will separate winning banks from banks merely holding the line.