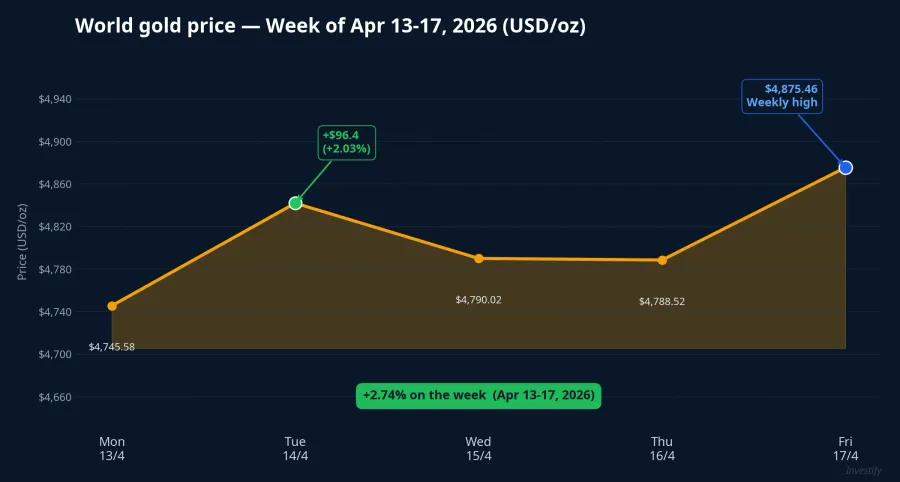

The week of April 13-17, 2026 recorded a rare phenomenon in the gold market: global capital flowed strongly into gold, yet the domestic market did not react in the usual direction. The SPDR Gold Trust bought 13.4 tonnes net over four consecutive sessions, world prices closed the week at USD 4,875/oz, up 2.74% for the week. Over the same window, SJC bars fell 0.29% and SJC 99.99% gold rings fell 0.41%. The spread between SJC and the converted world price narrowed by nearly 9 million VND per tael — and behind that number is not random volatility, but a policy being rewritten.

On the policy roadmap, Decree 24/2012/ND-CP — the document that has shaped Vietnam's gold market for 14 years — is entering its most significant reform phase since enactment. The State Bank of Vietnam (SBV) accepting 11 applications to produce gold bars outside SJC is no longer an administrative formality: it is a market signal that structural monopoly is set to be replaced by controlled competition. And the market has begun repricing the SJC premium well before the new decree takes effect.

Global institutional flows return to gold

On the global side, the picture is clear. SPDR Gold Trust — the world's largest gold ETF — bought 7.7 tonnes net in the April 17 session alone, extending a four-session buying streak totalling 13.4 tonnes. Total holdings now exceed 1,060 tonnes.Cafef This is a direct gauge of institutional flow, and SPDR's shift from net selling in late March to strong net buying in early April is an important signal for the new capital cycle.

World gold prices reflect this flow candidly. From USD 4,745.58/oz on April 13, prices climbed to USD 4,875.46/oz on April 17 — a 2.74% gain in one week. Two fundamental drivers operated simultaneously: the DXY index fell from 99.03 to 98.24, meaning the USD lost 0.80% of its value; and expectations that the Fed would hold or cut rates continued to revive in rates futures.

Under normal conditions, this should have pulled domestic gold prices in the same direction. But the past week offered no normal conditions.

SJC and gold rings move the other way — this is not trading noise

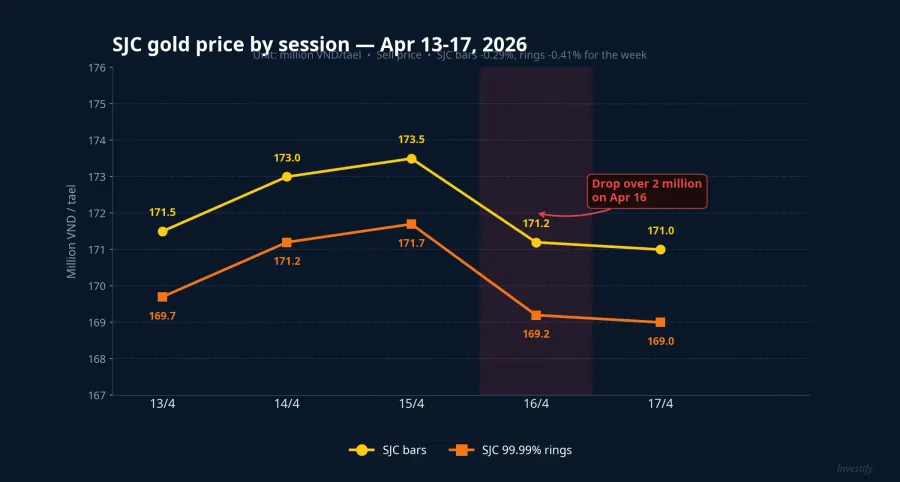

The SJC bar sell price moved along a trajectory almost independent of world prices. In the first two sessions, prices edged up from 171.5 to 173.5 million VND per tael, but from April 16 they dropped sharply: losing 2.3 million in a single session, then edging down to 171.0 million on April 17. By week's end, SJC bars were 500,000 VND below the week's open — a 0.29% decline while world prices gained 2.74%.

SJC 99.99% gold rings fell even more: from 169.7 million VND (April 13) to 169.0 million (April 17), losing 0.41% for the week. April 16 was a joint correction session when both formats lost over 2 million VND per tael in one trading day.

The USD/VND exchange rate was essentially flat — from 26,343 (April 13) to 26,340 (April 17) — so FX cannot be blamed. When a domestic asset moves against world prices while FX is stable, the cause must lie in domestic supply-demand, not external forces.

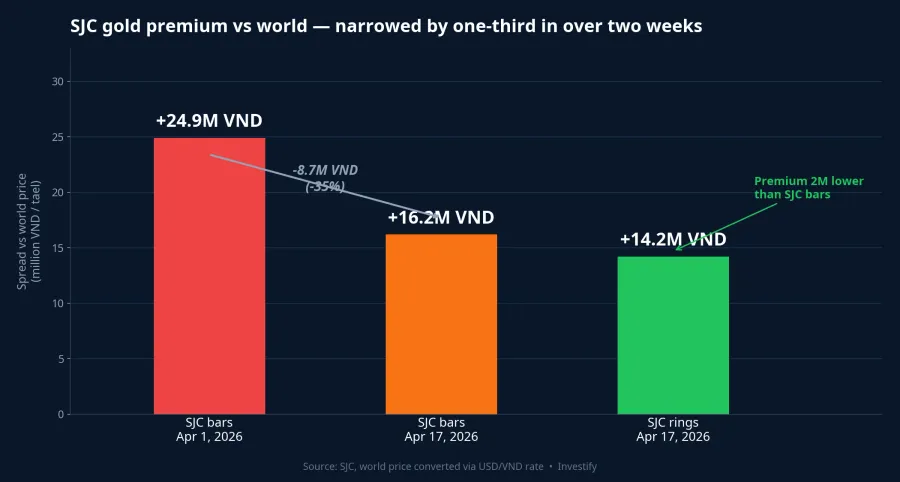

SJC-world premium: down nearly one-third in just over two weeks

This is the most important indicator in the story. Converting the world price via USD/oz × FX rate × (37.5/31.1035):

- April 1, 2026: world gold USD 4,785.25/oz, SJC sell 176.7 million → world converted ≈ 151.8 million → premium ≈ 24.9 million VND per tael.

- April 17, 2026: world gold USD 4,875.46/oz, SJC 171.0 million → world converted ≈ 154.8 million → premium ≈ 16.2 million VND per tael.

In just over two weeks, the premium contracted by nearly 9 million VND per tael, about 35% of its own value. Domestic media recorded a similar narrowing, with some sources estimating the premium fell from around 30 million early April to around 18 million VND per tael by April 17-18.Người Lao Động Differences between estimates reflect choices of reference FX and intraday price timing, but the direction of narrowing is consistent.

SJC 99.99% rings carry a premium about 2 million VND lower than bars: on April 17 the ring premium stood at about 14.2 million VND per tael. This is the lowest in many months and signals that the market is no longer willing to pay the full monopoly fee for SJC bar liquidity.

Mechanism: Decree 24 and two parallel markets

To understand why the premium exists and is now narrowing, return to the structure Decree 24/2012/ND-CP built. The decree gave SBV monopoly power over gold bar production — with SJC as exclusive processor — and tight control over raw gold import quotas. The consequence: world gold and SJC gold operate on two separate supply-demand mechanisms.

On the world side, XAU is priced by ETF flows, Fed decisions, inflation expectations, DXY, and geopolitical risk. When SPDR buys 13.4 tonnes in four sessions, that is a direct expression of institutional capital returning to gold as rate-cut expectations revive and the USD weakens.

On the SJC side, when world prices rise, producers cannot flexibly import more raw material to meet domestic demand. When world prices fall, SJC is not forced to adjust in tandem either. This hard quota mechanism has sustained a structural premium for years — at times exceeding 20 million VND per tael — and that premium is the fee buyers pay for legal assurance and liquidity inside a monopoly structure.

Reform is arriving on schedule. Early April, SBV accepted 11 applications to produce gold bars outside SJC and is reviewing licensing together with import quotas. This is not an abandonment of regulation, but a shift from single-entity monopoly to licensed competition — a model many Asian markets already operate. The expectation of gradually opening supply is what cools domestic demand: buyers no longer rush at elevated prices knowing legal supply is set to expand. Some experts say the premium could continue narrowing toward 10 million, even 5 million VND per tael if imports meet domestic demand.

Three paths for retail investors

Given current data, Vietnamese retail investors have three main approaches, each with its own trade-offs suited to different goals.

SJC bars (171 million VND/tael on April 17): highest liquidity, traded across the SJC network and several major banks, low legal risk. The 16-18 million premium is the cost of that liquidity. Core risk: if licensing of the 11 applications moves faster than expected, a sharp premium contraction will drag SJC prices down even if world gold is flat or rising slowly — bar holders could be stuck in a structural repricing.

SJC 99.99% gold rings (169 million VND/tael on April 17): premium about 2 million lower than bars while metal purity is equivalent. Liquidity is more localised, dependent on gold shops with a narrower resale scope. Suitable for long-term accumulators seeking lower premium cost and accepting lower liquidity.

Indirect access via funds or related equities: some open-end funds and ETF certificates have gold weight or positions in gold-mining/distribution companies. This path avoids the structural premium but trades it for equity volatility and fund management fees. Note: account-based gold trading via offshore brokers (gold forex) has no legal framework for Vietnamese individuals and should only be mentioned as a risk warning.

Monitoring: policy is the deciding variable

Over the next 3-6 months, two indicators will determine where the SJC premium heads: SBV's progress on the 11 gold-bar applications together with accompanying raw-material import quotas, and SPDR and major gold ETF net-buying streaks. The first shapes domestic supply, the second shapes the world price floor — and the premium sits at their intersection.

This is the direct result of structural expectations, not short-term trading noise. A week where the world rises and SJC falls does not happen often, but it reveals the nature of the two parallel markets clearly: retail investors are paying a premium for liquidity and legal assurance inside a monopoly structure that is about to be reformed. The true value of the premium will be repriced when Decree 24 is amended — not next week, but already within sight of both regulators and market. The question worth watching next quarter is not "will gold keep rising", but "how many of the 11 applications will SBV approve, and with how much import quota alongside".