The big picture is clear: last weekend was not a quiet weekend. Within 24 hours, Iran rotated its Hormuz policy axis from "fully open" back to "prior state" — meaning still under tight Iranian naval control. This is not just another news item added to the Middle East event stream: it is the trading thesis of Thursday evening, April 17, negated overnight, and the setup that makes Monday's April 20 open carry an unusually asymmetric risk for Vietnamese oil & gas investors.

The 24-hour rotation: from "fully open" to "prior state"

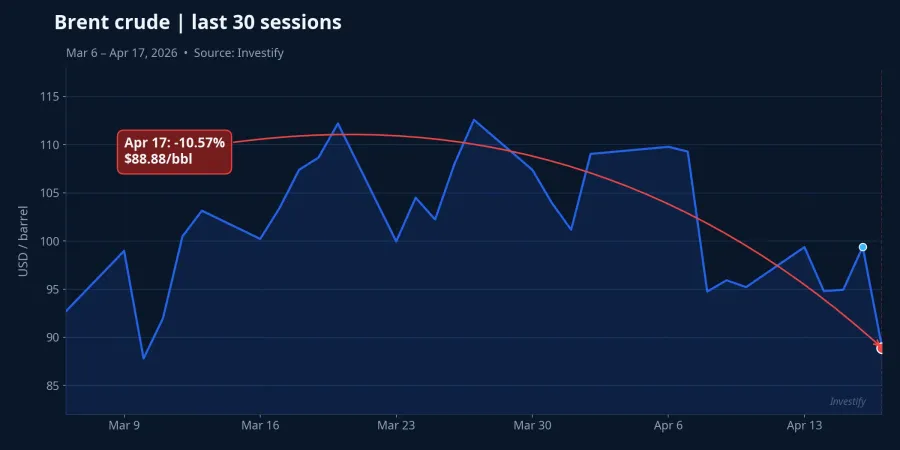

On the morning of April 17, Iran announced full reopening of the oil transit lane through Hormuz. That single headline was enough to knock Brent down 10.57% in one session — from $99.39/bbl to $88.88/bbl, the lowest level in nearly two months. Wall Street traded it as a risk-off exit: VIX fell to 17, the S&P 500 broke to new highs. In Vietnam, oil & gas stocks had already closed before the news hit: PVS held at VND 38,700, GAS at VND 80,100, BSR at VND 26,700, PLX at VND 39,950 and PVD at VND 33,350 — all modestly up on the April 17 session, and none had yet priced in Brent's overnight drop.

By April 18, Tehran reversed. When the U.S. refused to lift the naval blockade, Iran announced Hormuz would "return to the prior state" — which in practice meant the tanker corridor through the strait carrying roughly 20% of global crude would slip back into a gray zone: not absolutely closed, but not flowing freely either. Investors who reweighted their books overnight on April 17 based on the "Hormuz open" scenario now walk into the new week with one of their base assumptions erased.

Three Brent scenarios and portfolio paths for Apr 20-24

At this bifurcation point, the new week resolves into three distinct scenarios. Each has a specific confirmation trigger, and each points to a different portfolio tilt. The job in the first 48 hours of the week is not to pick a direction — it is to identify which scenario is actually playing out.

Scenario 1 — Hormuz stays restricted: Brent returns to $100+

Confirmation trigger: Iran maintains tanker restrictions beyond one week, the U.S. holds the naval blockade, and no negotiations are announced between April 20-22.

Brent could bounce sharply back to the $95-100 zone on the week's opening session and clear $100 on any naval incident or tanker interdiction. This is not an unfamiliar level: March data shows Brent trading at $112.19 on March 20 and $109.77 on April 6 during earlier escalations. A 4-6 week disruption makes these levels entirely plausible.

Flows in that case would concentrate in upstream. GAS is the most favored because its gas pricing formula is pegged to Brent — margins widen almost instantly when oil rises. PVS and PVD ride the E&P investment cycle with a lag of a few quarters, but day rates for rigs and M&C services should re-enter an uptrend if Brent stays elevated. On the opposite side, downstream is the pressure zone: BSR faces working capital risk and crack-spread compression, while PLX is exposed to retail pass-through risk under the 10-day pricing regime.

Scenario 2 — De-escalation within 3-5 days: Brent re-tests $85

Confirmation trigger: Announcement of U.S. - Iran talks before April 22, or Iran unilaterally reopens part of the tanker corridor under controlled conditions.

Brent continues its slide from $88.88 toward the $82-85 zone, rebalancing back to pre-crisis levels from early March. This is close to Goldman Sachs' published view — the bank sees Brent returning to the $75 zone over three months as supply normalizes.

In this scenario, last week's tilt reverses again. Upstream names and GAS face profit-taking after a strong year-to-date run, while downstream gets priority as oil stabilizes lower: improved margins, reduced working capital risk. For investors who loaded upstream last week, this is the scenario that calls for a rotation into BSR or PLX.

Scenario 3 — Fog zone at $90-95, elevated volatility

Confirmation trigger: No clear military escalation and no announced negotiations. Iran maintains tight control without a full closure, the U.S. holds the blockade without tightening further.

Brent oscillates between $88-95 with daily ranges of 3-5%. The market lacks directional signal, demanding range-trading rather than trend-following. Flows rotate between upstream and downstream on each headline, with no durable winner.

In this scenario, GAS becomes the defensive anchor: long-term contract-based gas pricing makes it less exposed to short-term volatility than other names in the sector. BSR and PVS, by contrast, are the most two-way volatile. BSR printing -3.84% on April 14 and +7% on April 10 is a live example of the range risk at these levels — wide enough to trigger margin calls at elevated leverage ratios.

The VND 369B stabilization fund: which scenario can it absorb?

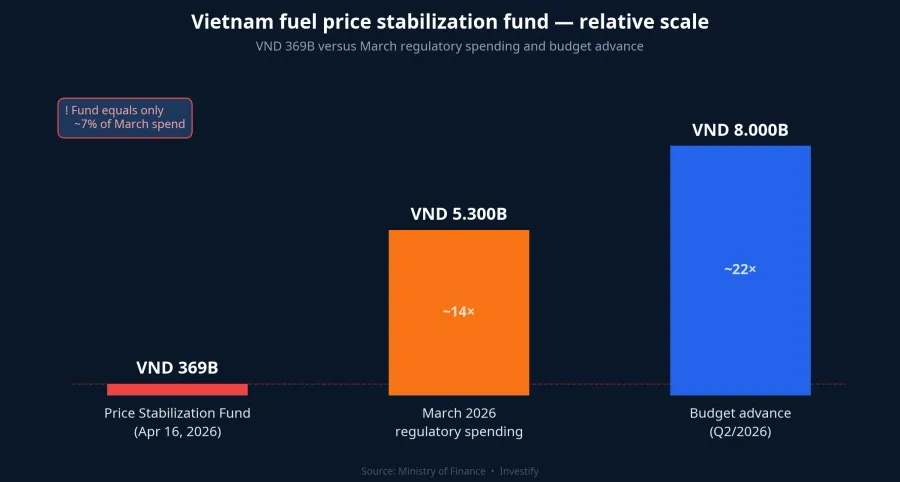

The fuel price stabilization fund closed at VND 369B on April 16 — up 25.2% from the prior week, but still thin compared to actual regulatory spending in volatile cycles. In March, the joint ministries deployed around VND 5,300B to stabilize retail prices; the current balance covers under 7% of that outlay.

In Scenario 1, the VND 369B fund has essentially no material role. Holding domestic pump prices will rely on the VND 8,000B budget advance already provisioned and the fuel tax-and-fee relief package running from April 16 through end-Q2. If Brent stays above $100 for a month, E5 RON 92 — currently at VND 22,590/liter and already up 17.5% over the last 30 days — is hard to shield from one or two more upward adjustments. In Scenario 2, pressure eases at the next pricing window and the fund can even rebuild. In Scenario 3, the fund likely gets activated intermittently alongside tax relief to keep retail prices inside a tolerable range — the scenario demanding the most delicate management.

Three checks before Monday's 9 a.m. open

For investors who sized positions on the April 17 "Hormuz open" thesis, three items to work through before the week begins:

1. Reassess Brent sensitivity in the book. If the portfolio is overweight downstream (PLX, BSR) bought on lower-oil expectations, consider setting stops or rotating a portion into GAS/PVS as a hedge against Scenario 1.

2. Track three signals Monday morning. Any tanker interdiction at Hormuz over the weekend; any announcement of U.S. - Iran talks; and where Brent opens in Asian trading (below $90 leans to Scenario 2, above $95 leans to Scenario 1).

3. Review margin. With daily ranges of 3-5% plausible in Scenario 3, elevated margin on oil & gas names is an asymmetric risk. Reducing leverage to a level that can survive one limit-down session is not a defensive option — it is a precondition.

The week of April 20-24 is not a week to bet direction. It is a week to identify which scenario is actually unfolding, then act. Scenario confirmation typically arrives within the first 24-48 hours of the week — and with Brent having moved more than 10% in a single session, early-week tape sensitivity should give the answer quickly. Two items to watch closely: any announcement of U.S. - Iran talks, and Brent's Asian open on Tuesday morning, April 21.