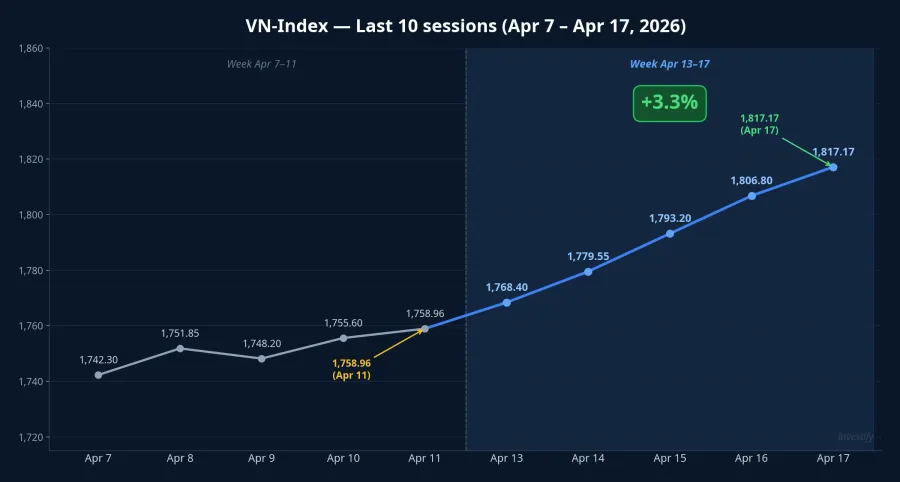

The big picture of April 13-17, 2026 contains a paradox many investors may have overlooked: VN-Index rose 3.3% to 1,817.17 points, yet foreign investors net-sold nearly VND 5,751 billion, concentrated on the two pillars of the VN30 basket. Reading each session, the trading sheet, and the stocks being accumulated, the story turns out to be not a retreat — but a deliberate rotation.

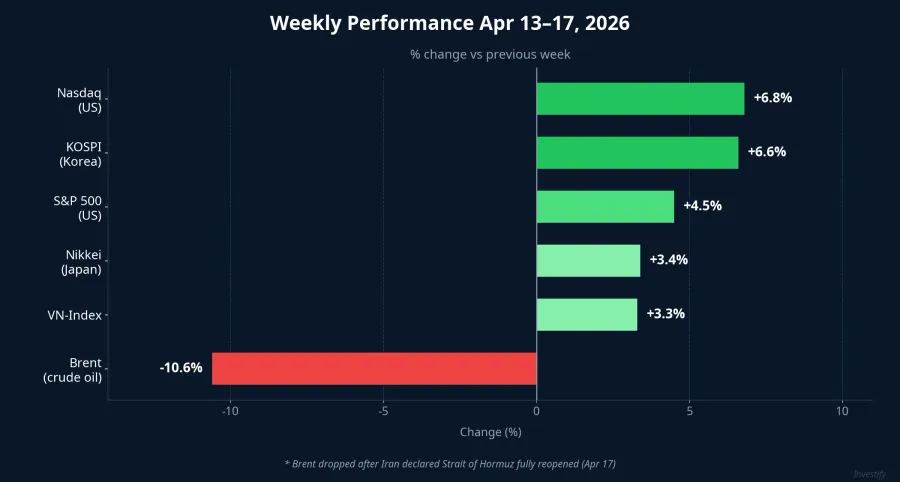

A globally favorable week: Brent -10.6%, S&P 500 +4.5%

Capital flows are shifting globally after Iran declared the Strait of Hormuz fully reopened on April 17. Brent dropped 10.57% in a single session to USD 88.88/barrel, easing energy-inflation concerns and clearing the path for equity inflows.Vietstock The S&P 500 closed above 7,100 for the first time (+4.5% for the week), Nasdaq +6.8%, Nikkei +3.4%, KOSPI +6.6%. DXY fell 0.9% to 98.24, VIX dropped to 17.48 — the lowest in about a year.

In that context, VN-Index +3.3% looks moderate next to developed markets, but liquidity holding above 850 million shares per session is a strongly positive signal from domestic capital. The real question is not "why did Vietnam rise less" — but "why did VN-Index still rise 3.3% while foreign investors were heavily selling VN30 heavyweights".

VHM and VN30F1M: two very different stories

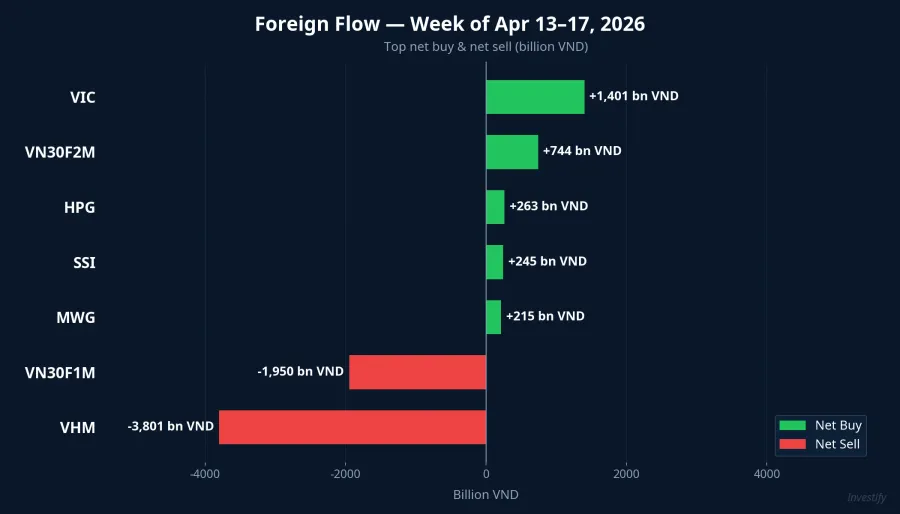

According to weekly trading data compiled by market channels, foreigners net-sold VND 3,801 billion of VHM and VND 1,950 billion of VN30F1M, accounting for nearly the entire weekly net outflow.Dan Viet But these are two instruments of entirely different nature, and must be separated to be read correctly.

VHM: VND 3,801 bn sold, price still rose 10.4% for the week. The largest net-sell session fell on April 15 at -VND 3,375 bn, the same day VHM closed +6.28% at VND 137,000/share. Session-by-session details reveal a striking absorption pattern:

| Date | VHM Net Sell (VND bn) | Close | % Change |

|---|---|---|---|

| Apr 13 | -58 | 122,900 | +1.49% |

| Apr 14 | +72 | 128,900 | +4.88% |

| Apr 15 | -3,375 | 137,000 | +6.28% |

| Apr 16 | -463 | 143,100 | +4.45% |

| Apr 17 | +23 | 135,700 | -5.17% |

VHM closed the week at VND 135,700, up 10.4% from VND 122,900. For every share foreign investors sold on April 15, a domestic buyer stood ready at ceiling or near-ceiling prices. This is one of the clearest signals of domestic capital strength in this cycle.

VN30F1M: VND 1,950 bn net-sold, but the bulk is rollover. This is the one-month VN30 index futures contract, not a stock. The entire net-sell concentrated on April 17, the day before expiry. In the same week, foreigners net-bought VND 744 bn of VN30F2M (two-month contract). Subtracting this rollover, the actual net withdrawal from derivatives is only about VND 1,200 bn — significant but far from the "retreat" the gross figure suggests.

Where did the foreign money go? VIC, HPG, SSI, MWG

While selling VHM, the top 5 stocks net-bought by foreigners were, in order:

- VIC: +VND 1,401 bn; Vingroup rose 17.4% for the week, from 160,000 to 187,900

- VN30F2M: +VND 744 bn (rollover from VN30F1M)

- HPG: +VND 263 bn; Hoa Phat traded flat (27,800 → 28,000), accumulation zone

- SSI: +VND 245 bn; beneficiary of record liquidity

- MWG: +VND 215 bn; retail holding momentum

This structure tells a very different story from the "VND 5,751 bn net-sold" headline. Foreign investors are not exiting Vietnam: they are taking partial profit on VHM (already up strongly year-to-date), shifting to parent company VIC (with the VinFast EV narrative and newly listed subsidiaries), accumulating cyclical steel (HPG), brokers (SSI), retail (MWG). In other words, this is rotation by narrative, not divestment.

How domestic capital absorbed the selling

With nearly VND 5,000 bn net-sold in large-caps yet VN-Index still +3.3% for the week, domestic capital was clearly concentrated in four focal points: (1) banks balanced the index during heavy foreign selling sessions, notably April 15 when VHM was dumped for VND 3,375 bn yet VN-Index still closed +1.41%; (2) steel (HPG) was accumulated by both locals and foreigners ahead of Q1 results; (3) retail – consumer (MWG) held steady; (4) brokers (SSI, VCI, HCM) benefited from record liquidity.

Two events shaping April 21-25

Next week's macro picture will be shaped by two independent variables: one international capital-flow factor, one domestic corporate-earnings factor.

CAPE begins USD 166 bn tariff refunds on April 20. The Consolidated Administration and Processing of Entries system of U.S. Customs goes live April 20, 2026, refunding around USD 166 billion to more than 333,000 importers following the Supreme Court's ruling on IEEPA tariffs.Newsweek Vietnam's US-facing exporter groups (textiles TCM, MSH; seafood VHC, ANV; wood products PTB; electronics) could benefit indirectly: importer margins improve, orders return faster in Q2-Q3. This is a macro driver that could pull foreign capital back into exporters.

Q1 earnings season and major AGMs. HPG holds its AGM on April 21, DCM on April 22 (already disclosed strong Q1 profit estimates), SMC on April 24 (new board election), VCG on April 25. In parallel, VN30 banks (VCB, CTG, BID, MBB, TCB, ACB…) are expected to begin reporting Q1 results from mid-week onward. Three key indicators to watch are credit growth, NIM (net interest margin), and asset quality. Banks hold a large weight in the VN30 basket, so Q1 results will directly influence domestic sentiment.

Three conditional scenarios for April 21-25

The three scenarios below are not probability forecasts, but a signal map: each requires a specific confirming trigger.

Scenario A: Foreign investors return, VN-Index heads toward 1,850. Triggers: CAPE refunds proceed on schedule from April 20 without administrative delay; Q1 bank earnings (especially VCB, TCB) beat NIM expectations; DXY stays below 98.5. Foreign capital may return to exporters (TCM, MSH, VHC, ANV, PTB) and top banks. Early confirmation: matched-order value above VND 25,000 bn/session for the first three sessions; foreigners net-buying in 2 of the first 3 sessions; DXY not breaching 99.

Scenario B: Selling continues, VN-Index retests 1,800. Triggers: Q1 bank earnings below expectations (NIM compression from funding competition); DXY breaks above 99; foreign net-sell of VN30 > VND 500 bn/session in the first two sessions. VN-Index could retreat to support at 1,795-1,800, especially if VHM and VIC correct after 10-17% weekly gains. Confirmation: VHM breaks 130,000; VIC loses 180,000; liquidity drops below VND 18,000 bn/session.

Scenario C: Rotation from blue chips to mid/small caps. Triggers: foreign flows neutral (no strong buying or dumping); Q1 results mixed, with exporters and raw materials beating while banks and real estate stay flat; Brent holds 85-90 USD. Capital leaves VN30 (overheated) for mid-caps with clear narratives: textiles, seafood, logistics (GMD, HAH), mid-tier steel (HSG, NKG). VN-Index trades sideways around 1,810-1,820 but market breadth improves.

Three indicators to monitor over the next two weeks

Rather than guessing which scenario plays out, investors should focus on three key signals to confirm triggers:

- Foreign flow in VHM and VIC: a reversal here will be the earliest signal of foreign behavior after the rotation week.

- DXY and USD/VND exchange rate: the 98-99 DXY zone is pivotal. Above 99, FX pressure forces further foreign selling; below 98.5, flows can return.

- HOSE matched-order liquidity: below VND 18,000 bn/session signals domestic capital cooling off, unable to absorb further foreign selling.

Foreign investors net-selling nearly VND 5,751 billion does not mean they are leaving the market. In the same week, they net-bought more than VND 1,400 bn of VIC, VND 263 bn of HPG, and rolled over futures — this is rotation by narrative, not retreat. Q1 earnings season starting next week will be a major catalyst for divergence, and the CAPE refund from April 20 is an external macro variable that could reshape capital flows. The question worth watching is not "which scenario will play out", but "which trigger appears first".