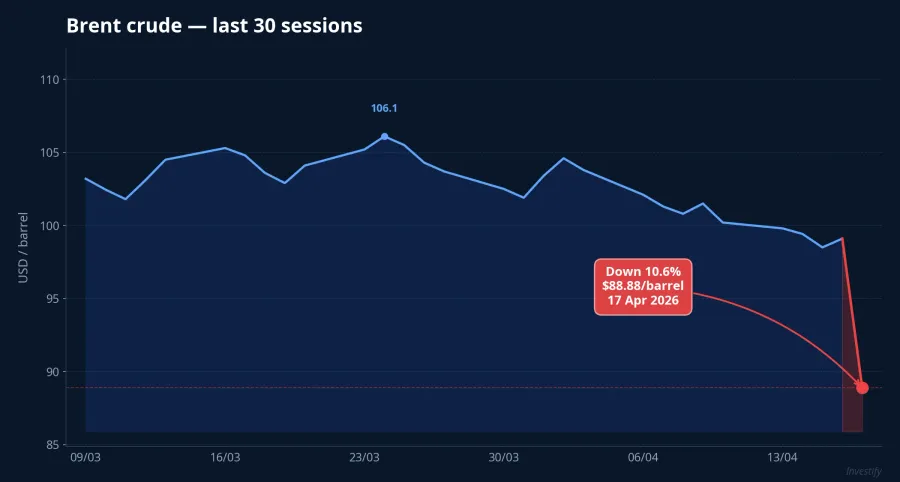

On the evening of 17 April 2026, Iran announced the full reopening of the Strait of Hormuz after exactly one week of blockade. Brent crude fell 10.6% in a single session to $88.88 per barrel — the sharpest one-day drop since early April. Wall Street set fresh highs across the board: the Dow closed at 49,352 (+1.6% on the day, +3.0% on the week), with the S&P 500 and Nasdaq also printing new records.

For Vietnamese investors, the timing matters. The news broke after HOSE's closing bell, which means the full Brent -10.6% shock will be repriced in Monday's session on 20 April. The 48 hours of the weekend are no longer about geopolitical commentary — they are about deciding the portfolio.

One-week context: from blockade to reopening

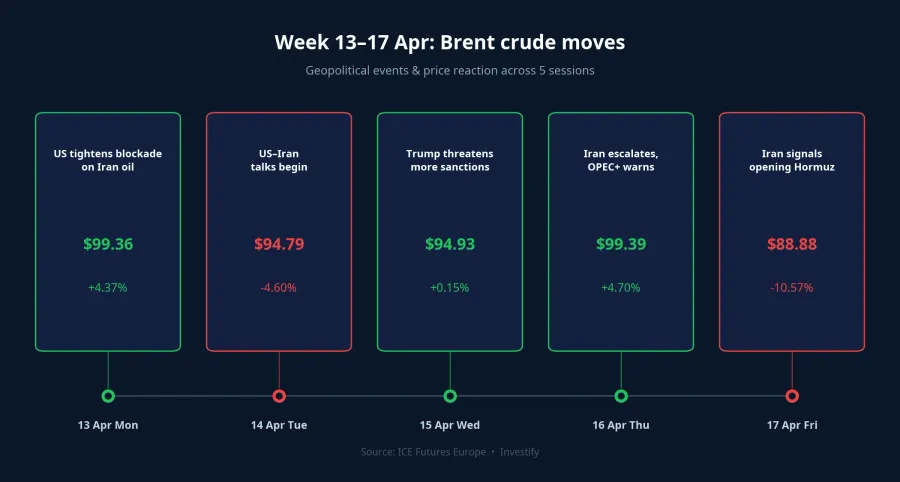

The event chain from 13–17 April moved fast. On 13 April, the US formally tightened its blockade on Iranian oil, and Brent jumped 4.37% to $99.36. The 14 April session corrected as signs of Pakistan-mediated talks emerged, sending Brent back to $94.79. On 15–16 April, Trump threatened potential strikes on Iranian infrastructure, pushing Brent back up to $99.39. Then on the evening of 17 April, Iran announced full reopening under a traffic-coordination arrangement — Brent collapsed to $88.88.

Looking at the numbers, Brent is now 14.1% below its $103.42 level on 17 March — the war premium has been almost entirely erased. US gasoline fell 7.1% on 17 April, confirming the cost-reduction trend is filtering through the supply chain. One thing to note: the US reaction is more cautious than the market's. Trump "thanked Iran" but kept the blockade on Iranian ports in place, pending a monitoring agreement. That means the market is pricing as if the conflict is over — but on paper, the US blockade is still technically active.

Five sectors in Vietnam, and where they stand heading into Apr 20

1. Upstream oil & gas (PVD, PVS, GAS, BSR): repricing risk

17 April revealed an interesting asymmetry: when Brent fell 10.6% after the HOSE close, Vietnamese oil & gas still closed in the green. PVD rose 1.37% to VND 33,350, PVS +1.04% to 38,700, GAS +2.17% to 80,100, and BSR +3.49% to 26,700 on volume of 10.4 million shares. The entire shock will land on the 20 April session.

Over the 10–17 April week, PVS fell 2.27%, PVD -1.77%, GAS -0.74% — but that was a slow pricing of the negotiation rhythm, not yet a reflection of Brent below $90. Four tickers carry idiosyncratic notes: PVD faces supply pressure after Dragon Capital cut its stake to 4.97% and with ~372m new shares pending issuance. PVS has the highest Brent beta in the group. GAS is less sensitive to spot Brent thanks to long-term contracts. BSR has a strong Q1 2026 earnings estimate but carries inventory risk if Brent stays near $85 next quarter.

Investors may consider: if prices gap up on opening momentum, it is an opportunity to trim overweight positions. Avoid adding leverage at current price zones.

2. Aviation (HVN, VJC): the clearest beneficiaries

This is the group with the highest sensitivity to the jet-fuel drop. Fuel costs are estimated at ~10% of HVN's revenue. If jet fuel falls 10% and holds, HVN's operating profit could rise by roughly VND 1,214 billion — equivalent to 15.3% of current operating profit. That is a high operating-leverage impact.

Over the week, HVN closed at 22,850 and VJC at 177,800. VJC itself jumped 6.83% on 15 April — smart money has already started positioning. VJC has a higher fuel-cost share than HVN structurally, so its expected sensitivity to a jet-fuel drop is stronger. However, refined fuels typically lag crude by several sessions due to crack-spread dynamics and in-transit inventory — expecting the full 10% to flow through to this quarter's P&L may be early.

Investors may consider: if prices do not gap up too hard at the open, this is the priority allocation group. The short-term risk is chasing a move the market has already partially priced.

3. Shipping & logistics (GMD, VSC, HAH): divergent stories

The same macro tailwind (lower fuel + Hormuz opening), but three different reactions. GMD rose 2.75% to 74,600 this week; VSC fell 6.2% to 23,500; HAH fell 2.16% to 55,000. The cause lies in company-specific factors, not macro.

GMD benefits indirectly through its port business (not shipping fleet), with exports steady and no large-holder selling. VSC was dragged by a chain of individual-shareholder sales on 13–16 April and broke technical support at 24,800. HAH faces dilution pressure from its March issuance, even though insiders registered to buy before 10 April — the flow has not been absorbed yet.

Investors may consider: GMD is the safer choice for 20 April. HAH and VSC have higher bunker-cost sensitivity but need to absorb their internal pressure before the macro tailwind can take hold.

4. Fertilizers (BFC, DPM, DCM): the story ran ahead of the news

This group was the week's biggest surprise. BFC surged 6.90% on 17 April and is up 15.03% over the week to 66,600. Meanwhile, DPM went sideways at 28,900 (-0.69% weekly) and DCM fell to 45,400 (-2.47% weekly). Same fertilizer group, three different scripts.

The key is the correlation to urea: BFC +0.23 (nearly independent), DPM -0.93 (strong inverse), DCM -0.75. BFC rose on its own story — strong domestic NPK demand, earnings expectations — not because of urea. DPM and DCM are the opposite: they benefit when natural-gas input prices fall with a lag. If Brent holds around $85–90 for several weeks, gas prices will adjust accordingly and margins for DPM and DCM have room to turn in the following quarter.

Investors may consider: BFC has run hot — be cautious of short-term profit-taking. DPM and DCM offer better medium-term accumulation room for the "gas-cost down" thesis.

5. Chemicals & plastics (DGC, AAA): lag and margin expansion

DGC closed at 54,500 (-0.73%). AAA closed at 7,030 (-0.14%). When Brent collapsed 10.6% on 17 April, these two barely moved — consistent with the structural lag in domestic chemicals. Based on research, if naphtha falls 3–7% (a more direct input than crude), DGC's gross margin could improve by 0.9–2.8 percentage points in the following quarter. AAA benefits via the ethylene/propylene channel with a longer lag due to old-stock clearing.

Investors may consider: this is a medium-term accumulation group after Brent stabilizes for a few weeks, not a 20 April trade. Q2 2026 earnings will be the confirming signal for margin improvement.

Three scenarios for 20 April

VN-Index closed 17 April at 1,817.17 with RSI14 at 64.82 — room still to run, but nearing overbought. MA5 at 1,794 is holding; MA20 at 1,708 confirms the medium-term uptrend. This week VN-Index gained 3.84% over five consecutive green sessions.

Up scenario (highest probability): VN-Index tests 1,835–1,850 on Wall Street momentum. Flow rotates from oil & gas into aviation, logistics, chemicals. Neutral: VN-Index oscillates 1,805–1,825. Oil & gas corrects but banks and steel hold the tape. Down: VN-Index loses 1,800, pulls back to 1,770–1,780 on profit-taking after a hot week, or bad US–Iran weekend news.

The biggest unpriced risk: the US is still maintaining its Iranian port blockade. A fresh hard statement or an incident on the Hormuz route over the weekend could trigger the down scenario. Additionally, the market may follow the "buy the rumor, sell the news" pattern — money already front-ran the ceasefire signal during the week.

Four mistakes to avoid

- Chasing aviation on the ATO: VJC already jumped 6.83% on 15 April, HVN has accumulated. If the gap up is too strong, wait for an intra-session pullback for a better entry.

- Dumping all oil & gas at ATO: PVD, PVS, GAS may gap down, but not all deserve panic-selling. GAS is less sensitive to spot Brent than the market thinks; BSR has Q1 earnings support.

- Adding leverage because "the market is green": VN-Index is less than 5% below the 52-week high of 1,902. The 1,835–1,850 zone is real resistance.

- Ignoring US–Iran tail risk: the US blockade is still technically active. Keep some cash for adverse weekend news.

Bottom line

20 April is the largest repricing session for the energy complex since early April. Priority order for a balanced portfolio: trim upstream oil & gas on any gap up, allocate more to aviation and port logistics, gradually accumulate DPM/DCM and DGC on the "lower input cost" thesis. Maintain equity exposure at 50–65% and avoid heavy margin near the 1,850 zone. The question worth answering before ATO: is the current portfolio optimized for a Brent-at-$85–90 regime over the next several weeks?

Three signals to watch in the coming days: (1) whether Brent falls below $85 or recovers to $92–95, (2) whether the US lifts the Iranian port blockade, (3) Q1 2026 earnings from the oil & gas and aviation groups over the next two weeks.