The 2026 Annual General Meeting of Hoang Anh Gia Lai JSC (HOSE: HAG) takes place today, April 17, 2026 in Ho Chi Minh City. Looking at the balance sheet and the plan submitted to the AGM, this is HAGL's best financial position in more than a decade: accumulated losses cleared, debt down 78% from the 2015 peak, and record 2025 profit.

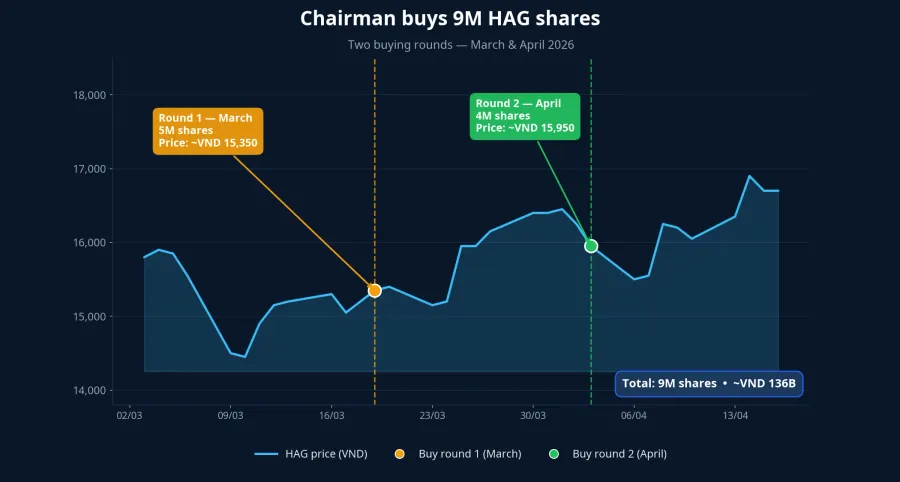

Ahead of the meeting, Chairman Doan Nguyen Duc spent about VND 136 billion to acquire 9 million additional HAG shares across two buying rounds in March and early April. The share price closed on April 16 at VND 16,700, up about 11% in one month. I'll walk through three core numbers investors need to understand before the AGM votes are tallied: the insider-buying signal, the basis for the doubled profit target, and the true state of the balance sheet.

1. Insider buying: The Chairman spends VND 136B on 9 million shares

In the two months before the AGM, the Chairman completed two buying rounds totaling 9 million HAG shares:

- Round 1 (Mar 11–18, 2026): purchased 5 million shares at an average price of about VND 15,100/share, worth about VND 76 billion. Ownership rose from 24.06% to 24.45%.VnEconomy

- Round 2 (Mar 26 – Apr 16, 2026): purchased another 4 million shares in the VND 15,000–16,700 range, worth about VND 60 billion. After the two rounds, he holds about 313.9 million HAG shares, or 24.77% of capital; the related-shareholder group controls about 29.94% of capital.Vietstock

Looking at the numbers, this is a move worth noting. VND 136 billion is no small sum, and it came right after HAGL disclosed record 2025 profit and an ambitious 2026 plan. However, insider buying is only one of many factors. HAG rose about 11% in the month before the AGM, so the second round was executed at a higher price band than the first. Investors should read this signal alongside the three financial numbers below, not in isolation.

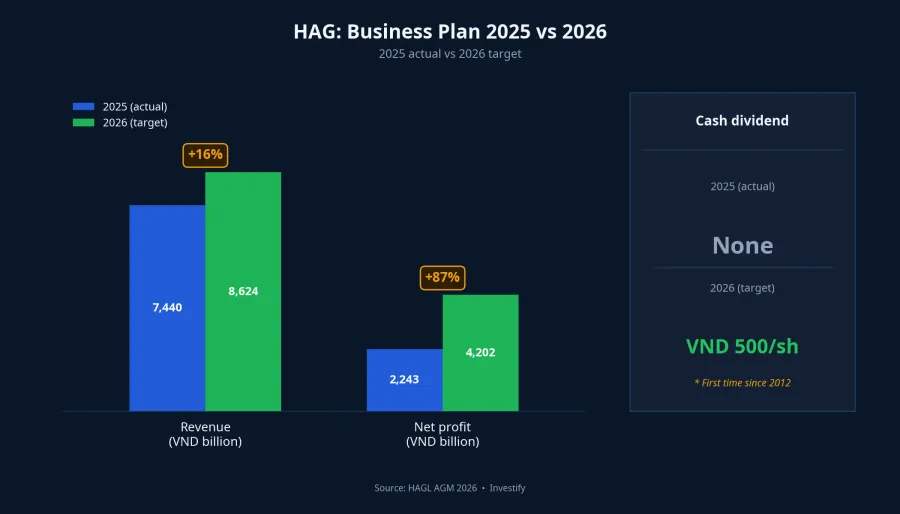

2. The 2026 plan: Revenue +16%, profit +87%

HAGL submits to shareholders a 2026 target of VND 8,624 billion in revenue (+16% vs VND 7,440 billion in 2025) and net profit of VND 4,202 billion, up 87% from VND 2,243 billion in 2025. If achieved, this would be the highest profit in the company's history.Doanh nghiep Hoi nhap

What stands out in this plan is the asymmetry: revenue grows only 16% but profit doubles. That means the profit gain comes not just from revenue growth but from margin expansion and lower finance costs. The plan rests on three specific pillars — each with a basis, and each with a condition.

Pillar 1 — Durian and banana. The fruit segment contributed about VND 5,780 billion in 2025 revenue, or 78% of the total, up 36% year-on-year.Doanh Nhan Sai Gon Banana remains the flagship crop with 7,000 hectares across Vietnam and Laos, with 40% of exports going to Japan and Korea. The 2026 growth driver is durian: about 80% of the durian acreage (roughly 2,000 hectares) is expected to enter harvest in 2026.24hMoney

Pillar 2 — Lower interest cost. DATC waived VND 1,534 billion in bond interest for HAGL.CafeF The debt-to-equity ratio fell from about 1.39 at end-2024 to 0.86 at end-2025. This is a meaningful profit boost but largely one-time — the 2026 margin expansion depends on whether the cost of capital continues to decline.

Pillar 3 — Pivot to coffee. HAGL announced plans to plant 7,000 new hectares of coffee, 1,000 hectares of mulberry, and 700 hectares of durian in 2026, along with 4 wet coffee processing plants and 1 coffee essence extraction plant. Total capital needed for the 2026–2028 coffee project is about VND 14,220 billion, expected to be raised via an IPO of the HGI subsidiary (VND 1,500 billion), bond issuance (VND 2,000 billion), and reinvested profits. This is HAGL's biggest "big bet" of the period and the item shareholders should press hardest on at the AGM.

3. The real risks sit in three places

A positive picture doesn't mean no risk. Reading the report carefully, three points are where pressure can build over the next 12 months.

First, the pork segment is still unprofitable. Pork revenue in 2025 was only about VND 209 billion, down 79% from 2024. HAGL suspended pig farming and is restocking with 15,000 sows, but the recovery is unproven. This segment now contributes just 3% of revenue, so direct profit impact is limited — but it shows HAGL's diversification capacity outside fruit is still constrained.

Second, receivables account for 83% of short-term assets. End-2025 short-term assets reached VND 8,802 billion, but VND 7,292 billion sits in receivables.VietNamNet This number needs clarification at the AGM: receivable from whom, collection progress, and loss risk. Collection quality will determine whether accounting profit converts to real cash flow.

Third, VND 14,220 billion of coffee capital is a heavy lift. The IPO and bond issuance plan depends on market conditions. If capital markets are unfavorable, HAGL may have to delay the timeline or restructure the funding mix — something to monitor over the next four quarters.

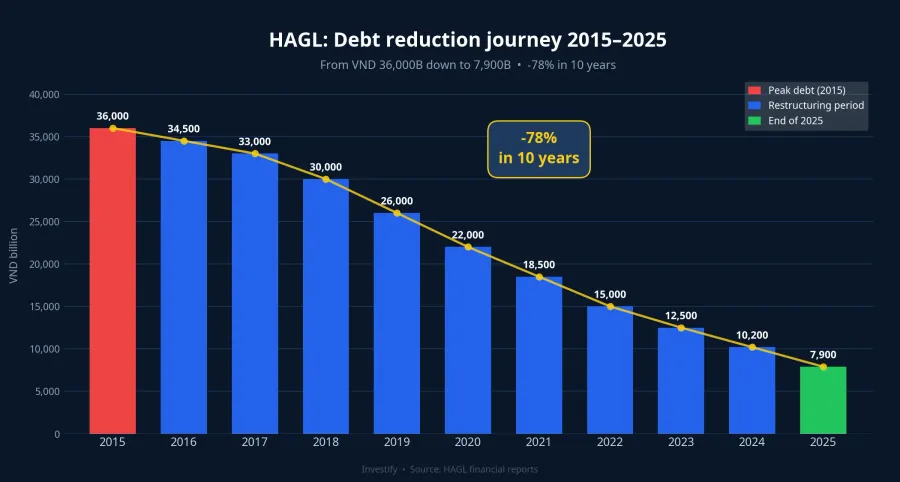

4. Debt-reduction journey: From VND 36,000B down to VND 7,900B

One of the less-discussed but most notable stories is HAGL's completion of its financial restructuring. What stands out in the 2025 financial report is that debt fell to about VND 7,902 billion — the lowest in more than a decade. Cash reached VND 680 billion, four times the prior period.Tinnhanhchungkhoan

Looking at the numbers: total liabilities peaked in 2015 at VND 36,000 billionMekongASEAN, on total assets of just over VND 50,000 billion. Over the following 10 years, HAGL divested a long list of real estate, hydropower, sugar, hospital, and hotel assets to repay debt. In early 2026, the company sold its entire 91.4 million shares of HAGL Agrico for about VND 594 billionCafeF. At the end of 2025, for the first time in more than 10 years, HAGL cleared its accumulated losses entirelyTap chi Cong Thuong, opening the door to resume dividend payments.

VND 500/share dividend: More symbol than sum

If approved, HAGL will pay a cash dividend of VND 500/share, the first since 2012.Tinnhanhchungkhoan With about 1.267 billion shares outstanding, total payout is estimated at VND 634 billion. Yield is about 3% at the current price — not high in isolation, but symbolically large: HAGL has officially emerged from the restructuring phase and entered a phase of returning cash to shareholders.

Three items to watch at today's AGM

- Coffee capital detail. The first-year 7,000-hectare rollout progress, offtake partners, and where the VND 14,220 billion comes from if IPO/bond markets are unfavorable.

- Receivables roadmap (VND 7,292 billion). Receivable from whom, progress, and loss risk.

- Export outlook amid US–China trade tension. HAGL exports mostly to China, Japan, Korea — will the supply chain benefit or be indirectly affected.

Bottom line

The quantitative picture shows HAGL enters the 2026 AGM in its best financial position in more than a decade: debt down 78% from peak, accumulated losses cleared, record profit, and leadership adding to ownership with real cash. The doubled profit target is ambitious but has basis: durian entering mass harvest and interest cost dropping via the VND 1,534 billion DATC waiver.

Main thesis: HAGL is at an inflection point from "recovery" to "growth". Three items to monitor over the next 12 months to confirm or refute this view: (1) Q1 and Q2 2026 profit margins to test the VND 4,202 billion target; (2) the collection pace of the VND 7,292 billion in receivables to gauge earnings quality; (3) progress on raising the VND 14,220 billion in coffee capital to measure funding-mix risk. The outcome of today's AGM — especially the discussion on the coffee plan and funding — will be the first data point to establish direction.