Starting May 10, 2026, supplementary pension funds in Vietnam will be allowed to buy listed stocks on HOSE and HNX for the first time. Decree 85/2026/ND-CP, issued on March 25, 2026, formally opens a new investment channel for an institutional capital pool that has grown 26-fold in four years.Bao Chinh phu

The current VND 2,200 billion in total net assets represents roughly 0.007% of HOSE's market capitalization. The near-term supply-demand impact is virtually zero. But focusing only on the absolute size means missing two things that matter more: the policy signal and the growth velocity.

Investment Portfolio: Capital Preservation First, Returns Second

Decree 85 structures portfolios with a clear risk-tiering principle. Government bonds must account for at least 40% of total net asset value for funds with NAV of VND 5 billion or more.Tap chi Kinh te Tai chinh This forms the safest foundation layer, ensuring funds always maintain a liquidity cushion.

Listed stocks are permitted up to 30% of fund assets, subject to strict criteria: stocks must not be under warning, control, or trading restriction status, and must have been listed for at least 6 months. The sole exception is Top 5 market-cap stocks, which need only 3 months.Luat Nguyen

The remainder may be allocated to fund certificates, government-guaranteed bonds, investment-grade corporate bonds, and bank deposits. Speculative derivatives, direct real estate, and assets that cannot be marked to market are excluded entirely.

This "40% government bonds + max 30% stocks" structure shows the government prioritizes capital preservation for workers, while simultaneously opening the door for funds to access higher returns from equities.

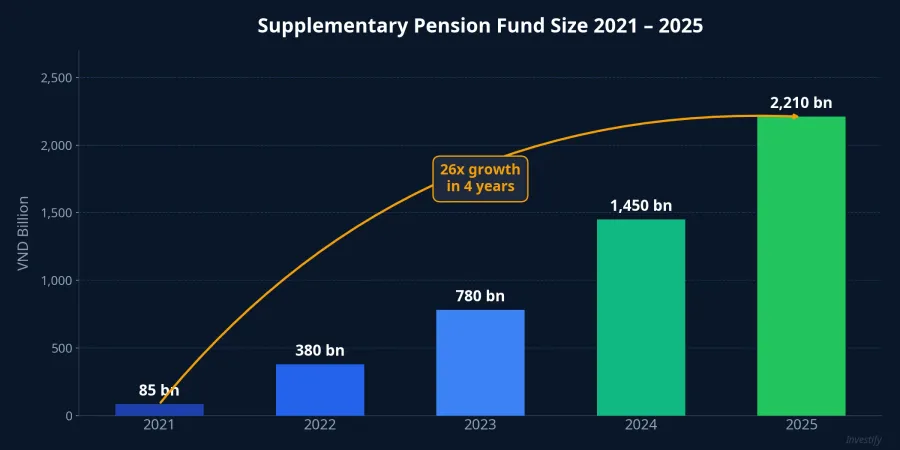

VND 2,200 Billion: Small in Absolute Terms, But Watch the Growth Rate

At the 30% equity limit, the maximum stock holdings across all 7 supplementary pension funds is currently about VND 660 billion. Compared to HOSE's total market capitalization of nearly VND 8.83 quadrillion as of February 2026, this is negligible.Dai bieu Nhan dan

However, the growth trajectory tells the real story. In 2021, the entire supplementary pension system held approximately VND 85 billion. By end-2025, that figure reached nearly VND 2,210 billion, a 53% increase in 2025 alone compared to end-2024. Participants grew 17.1% to 28,538 people, with total new contributions of VND 720.77 billion during the year.Bao Chinh phu

If roughly 50% annual growth is sustained thanks to clearer legal frameworks from the new Decree and the Social Insurance Law 2024 dedicating an entire chapter to supplementary pensions, fund size could reach approximately VND 5,000 billion by end-2027 and VND 10,000-15,000 billion by 2029. At that point, the 30% equity allocation would amount to VND 3,000-4,500 billion, beginning to meaningfully impact blue-chip liquidity. This is an optimistic scenario that depends on whether tax incentive policies are implemented.

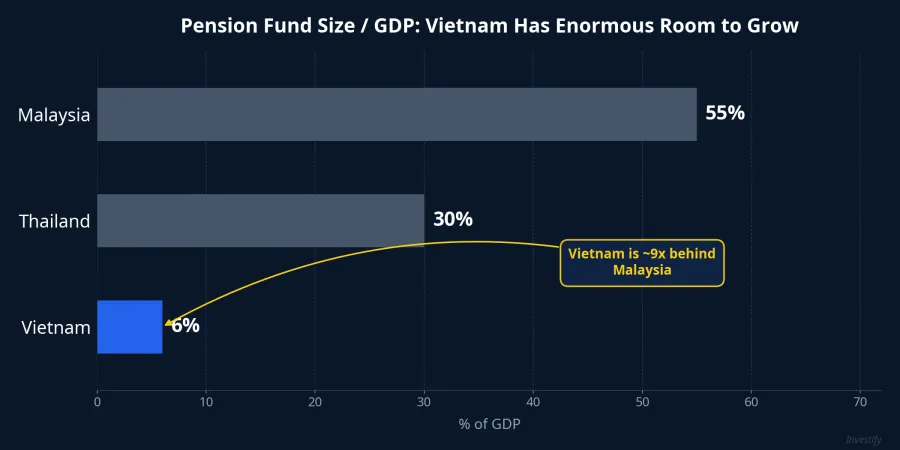

Regional Comparison: Enormous Room to Grow

Vietnam's pension funds are at a very early stage compared to the region. Malaysia's EPF has AUM equivalent to roughly 55% of GDP, making it the largest institutional investor on Bursa Malaysia. Thailand's GPF and Provident Funds manage AUM of approximately 30% of GDP.Tap chi Kinh te Tai chinh

Meanwhile, Vietnam's total fund management AUM equals roughly 6% of GDP, with supplementary pension funds accounting for just VND 2,210 billion of that total. The nearly 9x gap with Malaysia underscores the growth potential over the next 5-10 years, particularly if tax policies create sufficient incentives for companies and workers to participate.

The Convergence Effect: Circular 136 and FTSE Upgrade

Decree 85 does not stand alone. It coincides with two other major policy shifts creating a convergence effect for institutional capital flows in Vietnam's stock market.

Circular 136/2025/TT-BTC (effective February 12, 2026) expands the securities fund ecosystem with two new fund types: money market funds (MMF) and infrastructure bond funds.Vietstock It also introduces for the first time a "Liquidity Protection Level" mechanism following international standards, helping open-end funds reduce mass-redemption risk.VTV This provides critical legal infrastructure for supplementary pension funds to access safer capital allocation tools.

FTSE upgrade is expected from September 2026. According to FTSE representatives, passive ETF inflows are estimated at approximately USD 1.5 billion, disbursed in 4 tranches (10%, 20%, 35%, 35%) starting September 2026. Total capital flows including both active and passive could reach USD 6-8 billion over several years.CafeF

The combination of pension funds entering equities for the first time, an expanded fund ecosystem, and FTSE upgrade attracting foreign capital is building a thicker long-term institutional capital layer. This is a structural transformation unfolding over years, not a short-term event.

Don't Confuse "Small" with "Unimportant"

The common reaction to hearing "VND 2,200 billion" is to dismiss it as too small to matter. This assessment is correct regarding short-term market impact, but misses two factors.

First, the policy signal matters more than the number. Decree 85 marks the first time the government has officially allowed pension money into stocks. This is a mindset shift that paves the way for expansion as more funds are licensed and equity limits are potentially raised. Second, the growth rate determines long-term impact. Malaysia's EPF also started from a modest size in the 1950s. The decisive factor is whether the legal framework creates sufficient incentives for broad participation by companies and workers.

Three Signals to Watch After May 10

Rather than expecting immediate price impact, investors should focus on three signals for the remainder of 2026.

First, asset allocation reports from the 7 pension funds after May 10: the actual equity allocation percentages will reveal how ready the funds are. If most remain concentrated in bonds and deposits, it signals caution during the early phase.

Second, the number of newly licensed funds in H2 2026: currently only 4 companies manage 7 funds. If that grows to 10-15 funds, total system size will accelerate well beyond the current pace.

Third, tax incentive policies: if the government implements personal income tax deductions for supplementary pension contributions (similar to the US 401(k) or Malaysia's EPF model), growth rates could increase significantly beyond the current trajectory.

Decree 85/2026 is the first building block in constructing a long-term institutional capital layer for Vietnam's stock market. The policy signal is clear, and 26-fold growth in 4 years shows the foundation is being laid. The next decisive factors are tax policy and new fund licensing: these two variables will determine whether the supplementary pension system grows linearly or exponentially.