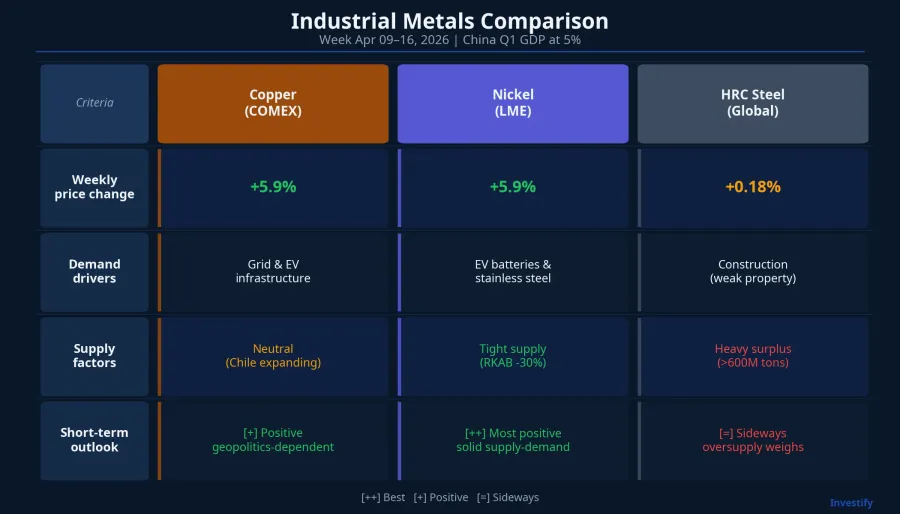

China's Q1 2026 GDP came in at 5% YoY, beating the Reuters consensus of 4.8% and recovering sharply from Q4 2025's 4.5%.China Daily The big picture shows growth tilting heavily toward manufacturing and infrastructure: industrial production rose 6.1% YoY in Q1 while retail sales managed only 2.4% YoY. But when this GDP figure is mapped onto commodity prices, three industrial metals reacted in entirely different ways.

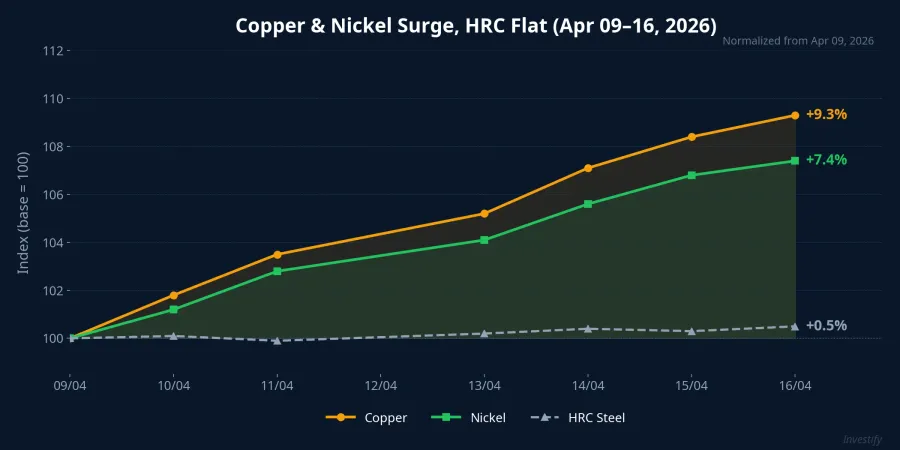

Copper +5.9%, Nickel +5.9%, HRC Steel +0.18%

During the week of April 9–16, 2026, COMEX copper rose from 5.75 to 6.09 USD/lb (+5.9%), LME nickel climbed from 17,215 to 18,228 USD/ton (+5.9%), while HRC steel barely budged at 1,086.93 USD/ton (+0.18%).

Same GDP catalyst, same improving Chinese industrial backdrop, yet copper and nickel surged nearly 6% while HRC steel stood still. The answer lies in the distinct supply-demand structure of each metal.

Copper: infrastructure demand pulls prices, supply is not the bottleneck

Copper has long been called "Dr. Copper" for its ability to reflect global economic health. Last week, copper prices recovered to a 2-month high above 6.1 USD/lb, fully erasing the decline triggered by Middle East tensions.TradingEconomics

Three main drivers fueled this rally. First, copper inventories at the Shanghai Futures Exchange (SHFE) fell over 30% during March–April 2026, with import premiums staying elevated, indicating real physical demand absorbing supply. Second, Hormuz peace expectations as Washington and Tehran prepare for a second round of talks before the 2-week ceasefire expires, reducing inflation concerns and supporting industrial metal sentiment. Third, China's infrastructure investment in power grids and renewables rose 11.4% YoY in January–February, creating direct demand for copper, an essential material in power grids, EVs, and electronics.Global Times

However, copper lacks a sudden supply squeeze. Chile, the world's largest producer, is accelerating new mining permits. Therefore, copper's rally is primarily demand-driven, and if US-Iran talks collapse, copper prices could face renewed pressure from global growth concerns.

Nickel: a dual supply-demand boost from Indonesia

Nickel was the strongest performer among the three metals, rising from 17,215 to 18,228 USD/ton during the week, equivalent to +5.9%. The current price sits within the average 2026 forecast range of 17,000–18,000 USD/ton from Mysteel and Macquarie. What gives nickel a clear edge over copper is the supply side.

Indonesia, the world's largest nickel producer, cut its 2026 RKAB mining quota to approximately 250–270 million wet metric tons, a roughly 30% reduction from 379 million tons in 2025.Argus Media Indonesia's Ministry of Energy and Mineral Resources (ESDM) confirmed a target of approximately 250–260 million tons.Mysteel

This figure falls significantly below the estimated nickel ore consumption of approximately 330 million tons for 2026, creating a gap of approximately 77 million tons.Metalnomist This is precisely why nickel has supply-side momentum that copper lacks. On the demand side, nickel benefits from two major segments: NMC (nickel-manganese-cobalt) EV batteries riding on China's industrial production growth, and stainless steel accounting for roughly 65% of total global nickel demand.

It's worth noting that the new RKAB only took full effect in April, and supplementary quota approvals may come in Q2. If Indonesia loosens quotas, supply-side support will weaken. However, in the short term, nickel has the strongest supply-demand foundation of the three metals.

HRC Steel: China's oversupply crushes all growth catalysts

While copper and nickel gained nearly 6%, HRC steel barely moved from 1,085 to 1,086.93 USD/ton during the week. A 5% GDP beat generated virtually no price reaction. The core reason is structural oversupply from China.

China has over 600 million tons of excess steel capacity, a condition persisting since 2022 when the property sector weakened.American Manufacturing Domestic steel consumption fell 2% in 2025, with a further 1% decline forecast for 2026 as the housing market has yet to recover.MEPS International China's steel exports reached 110.7 million tons in 2024, nearly double the 2017–2022 average of 70 million tons per year, pushing international HRC prices to their lowest since 2016.Breakwave Advisors

In other words, the 11.4% increase in infrastructure investment primarily consumes construction steel (rebar), not HRC used in automotive and manufacturing. Demand growth in this segment is insufficient to offset the oversupply pressure from property and cheap exports. The 4% production cut policy is enough to ease pressure, not reverse the trend.

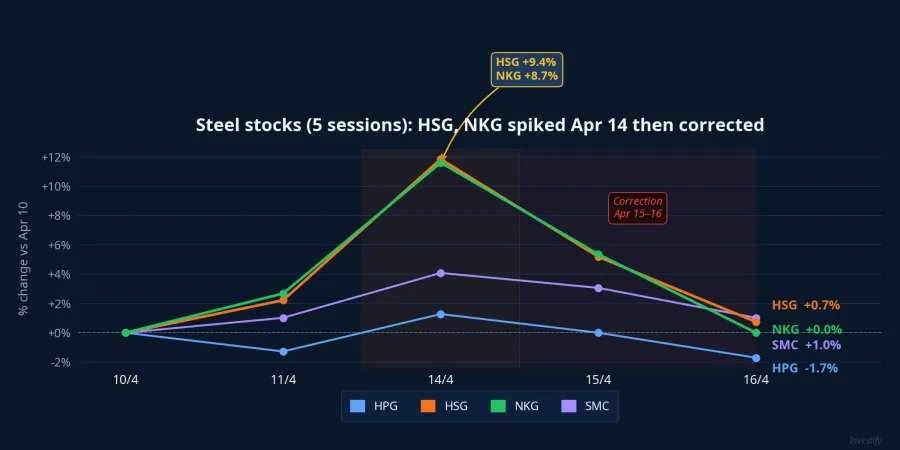

In Vietnam: steel stocks diverge from global metal prices

The VN-Index gained 18.09 points (+1%) to 1,818.74 in the morning session on April 16. However, the metals sector fell 1.66%, moving in the opposite direction to the global copper and nickel rally. HPG was flat at 28,050 VND, HSG fell 0.31%, NKG dropped 0.34%, and SMC declined 0.72%.

The critical distinction: HPG, HSG, NKG, and SMC are steel companies, not copper or nickel producers. When global copper prices rise 5.9%, this does not directly improve profit margins for Vietnamese steelmakers. The decisive factor for this group is HRC pricing, and HRC gained only 0.18%.

Additionally, HSG and NKG had already surged on April 14 (HSG +6.84%, NKG +6.74%), making a technical correction on April 16 natural. HSG has a 30% stock dividend plan and NKG has an ESOP plan, creating cautious sentiment around dilution. The VN-Index rose 1% but only 94 stocks advanced versus 216 declining, with money flowing into real estate (VIC, VHM) rather than steel.

One notable bright spot: foreign investors were net buyers of approximately 3.58 million HPG shares in the morning session, suggesting foreign capital maintains a positive medium-term outlook for Hoa Phat.

Nickel has the strongest foundation, HRC steel awaits new signals

The big picture shows that China's Q1 GDP reaching 5% is positive news for industrial metals, but the market did not respond uniformly. Nickel holds a dual advantage from both supply (Indonesia's RKAB cutting 30%) and demand (EV batteries + stainless steel), creating the strongest foundation among the three metals at least until new information emerges about supplementary quotas. Copper gained well on infrastructure demand but lacks supply-side momentum, making its outlook dependent on US-Iran negotiation outcomes. HRC steel remains virtually immune to positive GDP signals because structural oversupply is too large; unless China cuts production deeper than the committed 4%, HRC prices will continue to trade in a narrow range around 1,060–1,120 USD/ton.

Three factors worth monitoring over the next 4–6 weeks: (1) Indonesia's Q2 supplementary RKAB quota approval, (2) the outcome of the second round of US-Iran talks on Hormuz, and (3) whether Chinese steel inventories show a significant decline. These signals will determine whether the divergence among the three metals continues to widen or narrows.