On April 14, 2026, Petrolimex (HOSE: PLX) officially announced it no longer meets the requirements for public company status under the Securities Law 2019. The shareholding ratio held by non-major shareholders stands at just 9.4%, below the minimum threshold of 10%.Vietstock What the announcement doesn't spell out: 43,264 minority shareholders hold less than one-tenth of the voting rights in Vietnam's leading petroleum company, and they have exactly one year to wait before the delisting scenario becomes reality.

Ownership Structure: State and ENEOS Hold Nearly 89%

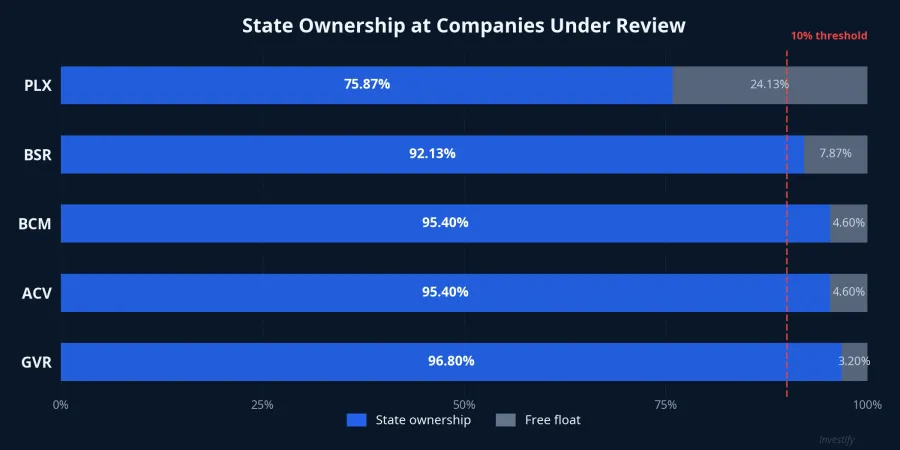

The real risk lies in the extremely concentrated ownership structure. The Commission for the Management of State Capital at Enterprises (CMSC) holds 75.87% of charter capital, plus ENEOS Corporation (Japan) with 13.08%. Together, these two major shareholders control approximately 88.95%, leaving just 11.05% for all 43,264 remaining shareholders.Vietstock

However, since some entities in the "non-major shareholder" group include institutions holding under 5% but not freely traded, the actual free float is only 9.4%. The absolute shortfall is modest: PLX needs approximately 7.8 million additional shares (0.6% of capital, worth roughly VND 313 billion at current prices) transferred from major to non-major shareholders to meet the threshold. But the real barrier lies in the state capital divestment decision-making process.

Stock Price Reaction: PLX Down 38% in 5 Weeks

PLX closed at VND 40,150 on April 14, down 1.35% from the previous session, corresponding to a market cap of approximately VND 51 trillion. More notably, PLX has declined from VND 64,700 (March 5) to VND 40,150 (April 14), a drop of approximately 38% over five weeks. Most of this decline relates to oil price volatility and broader market conditions; the public company status news may add short-term pressure, but there is insufficient data to precisely attribute the contribution of each factor.

Petrolimex's subsidiary, Petrolimex Import-Export (PIT), also fell 6.91% in the same session, indicating that concerns have spread across the Petrolimex ecosystem.

What Does the Law Say, and How Long Is the Clock?

Under Article 32 of the Securities Law 2019, a public company must simultaneously meet three conditions: paid-up charter capital of at least VND 30 billion, equity of at least VND 30 billion, and a minimum of 10% of voting shares held by at least 100 investors who are not major shareholders.Legal System

PLX satisfies the first two conditions (charter capital of nearly VND 12,940 billion, equity of over VND 29,000 billion) but violates the third. When non-compliant, the enterprise must make an extraordinary disclosure and has a one-year deadline to remediate. If after one year the threshold is still not met, the enterprise must file for revocation of public company status, potentially leading to delisting.Legal Library

Not Just PLX: Multiple State-Owned Giants in the Same Situation

Petrolimex is not alone. The State Securities Commission has ordered a review of multiple state-owned listed enterprises that fail to meet public company requirements.An ninh Thủ đô Notable cases include:

- GVR (Vietnam Rubber Group): Ministry of Finance holds 96.8%, free float just 3.2%

- ACV (Airports Corporation): Ministry of Finance holds 95.4%, free float 4.6%

- BCM (Becamex IDC): Binh Duong Province owns 95.4%, free float 4.6%

- BSR (Binh Son Refining): PVN owns 92.13%, free float just 7.87%, already announced loss of public status in March 2026Dân trí

This is a direct consequence of incomplete equitization: the state reduced ownership below 100% for listing purposes but never sold enough for free float to meet legal thresholds. As the Securities Law 2019 tightened requirements and the SSC began actual reviews, the issue has come to light.

Precedent Exists: Viet Y Steel Left the Exchange After 15 Years

The delisting risk is not theoretical. Viet Y Steel (VIS) was delisted from HOSE on April 22, 2022, after 15 years of trading, when two major shareholders held 93.81% of capital, leaving just 6.19% free float.VietnamFinance More recently, Sovi (SVI) also had its public company status revoked in 2026 when controlling shareholders held 94.11%.CafeF

The common thread: when free float is too low, liquidity dries up, minority shareholder rights suffer, and eventually the company is forced off the exchange.

Three Scenarios for PLX Over the Next Year

Scenario 1: Partial state divestment. This is the most thorough solution but also the most complex. PLX only needs the state to divest approximately 0.6% of capital (about 7.8 million shares, worth roughly VND 313 billion) to meet the 10% free float threshold. The absolute amount is modest, but according to experts, 2026 is still the procedural preparation phase, with actual divestment potentially stretching to 2027–2028.Saigon Times

Scenario 2: ENEOS adjusts its stake. ENEOS could sell a portion of its shares (from 13.08% to below 5%), shifting from major to non-major shareholder status and thereby increasing the free float ratio. However, as of April 2026, there is no information about any ENEOS plan to reduce its PLX holding.

Scenario 3: Failure to remediate, loss of public company status. If by April 2027 PLX still hasn't raised its free float above 10%, the company could lose its public company status. Consequences: potential delisting from HOSE, liquidity freeze, 43,000 shareholders losing their primary trading channel, and likely sharp price declines ahead of delisting due to selling pressure.

Business Operations Remain Solid — This Is Purely a Legal Risk

An important distinction: this is a legal risk related to ownership structure, not a business risk. PLX remains Vietnam's leading petroleum enterprise with 2025 revenue of VND 309,875 billion and pre-tax profit of VND 3,643 billion.Vietstock The 2026 plan targets revenue of VND 315,000 billion.VietnamBiz

But that is precisely what makes this concerning: a well-performing enterprise could be forced off the exchange simply because the state hasn't completed its equitization process. Minority shareholders have done nothing wrong, yet they stand to lose the most if the delisting scenario materializes.

Conclusion: Clear Legal Risk, Resolution Depends on Political Will

The PLX situation is not an isolated incident but a systemic consequence of Vietnam's incomplete state-owned enterprise equitization. The Securities Law 2019's 10% free float threshold is the mechanism forcing this process to its conclusion: either the state divests further so the company is truly "public," or the company exits the exchange.

For PLX, the most feasible remediation scenario is state divestment of 0.6% capital, but procedural barriers may extend beyond the one-year deadline. The delisting risk is low-probability in the short term but cannot be ruled out, especially given the VIS precedent showing that HOSE does not hesitate to enforce regulations.

Three factors to monitor in coming months: the 2026 AGM resolution on ownership restructuring plans, CMSC's timeline for divestment, and the SSC's review progress across similar state-owned enterprises.