SSI Research has just released its Q1/2026 earnings estimates for approximately 40 listed companies: 35 are projected to deliver positive profit growth, but the divergence spans from +465% (NT2) to -68% (KBC).CafeF The aggregate figures — profits up approximately 16% year-over-year but down approximately 26% from Q4/2025 — mask the real story: extreme sector-level divergence.VnEconomy

This analysis groups companies into three tiers: breakout (power, retail, fertilizer), stable (steel, banking), and under pressure (industrial parks). With the VN-Index at 1,758.96 points as of April 13, sector selection matters more than guessing overall market direction.

Breakout Group: Power, Retail, Fertilizer

NT2: Profit Up 465% on Output and Depreciation

Nhon Trach 2 Power (NT2) is projected by SSI Research to post approximately VND 209 billion in after-tax profit, up 465% year-over-year.VietnamBiz The figure is impressive but needs context: the Q1/2025 base was very low, and both key drivers are structural. Power output rose 50–60% on dry-season electricity demand, while depreciation costs dropped significantly as the plant nears the end of its equipment lifecycle.

NT2 shares closed at VND 26,550 on April 13, recovering from the VND 25,200 zone earlier in the month. The +465% reflects a rebound from a low base rather than a signal of a new sustainable growth cycle.

PNJ and MSN: Gold, Tungsten, and Retail Drive Multi-Fold Growth

PNJ is estimated to earn approximately VND 1,500 billion, up 121% year-over-year and 23% quarter-over-quarter. If confirmed, this would be PNJ's highest quarterly profit ever.CafeF The key driver: improved gold raw material supply boosted jewelry sales, combined with the advantage of low-cost inventory from previous periods. PNJ shares are trading around VND 110,000, up approximately 10% from the early April low.

Masan Group (MSN) is estimated to earn nearly VND 2,500 billion, up 154% year-over-year. Growth came from the tungsten segment (Masan High-Tech Materials) as tungsten prices maintained their uptrend, combined with recovery in food and beverage and improved efficiency in retail.CafeF MSN shares stood at VND 77,000 on April 13.

Mobile World (MWG) is projected to earn approximately VND 2,250 billion in after-tax profit, up 45% year-over-year and 8% quarter-over-quarter, continuing its streak of record quarterly profits driven by recovering tech consumer demand and improved margins at Bach Hoa Xanh.CafeF

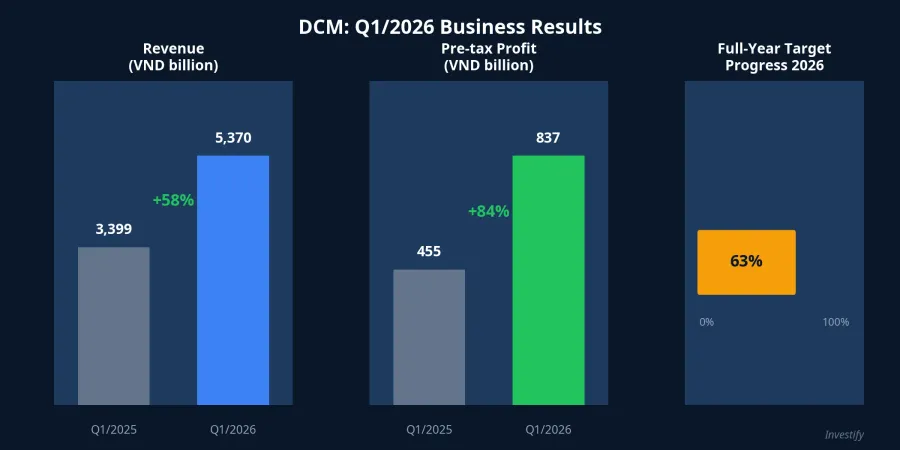

DCM: Actual Results Far Exceed Expectations

While most companies only have brokerage estimates, Ca Mau Fertilizer (DCM) has already released preliminary Q1/2026 results: revenue of VND 5,370 billion, up 58% year-over-year; pre-tax profit of VND 837 billion, up 84%.VietnamBiz Notably, DCM completed 63% of its full-year profit target in just the first quarter alone.Doanh nhân & Pháp luật

Three factors drove the strong results: improved margins on imported fertilizer as DCM sold through low-cost Q4/2025 inventory, higher agricultural demand during the early-year crop season, and a more diversified revenue mix with urea at 61%, imported fertilizer at 25%, and NPK at 7%. DCM shares reached VND 47,000 on April 13, up approximately 9% from the VND 43,000 low on April 6.

Stable Group: Steel and Banking

HPG: Big Numbers, But Wide Divergence Among Estimates

Hoa Phat (HPG) is estimated by SSI Research to post approximately VND 5,500 billion in after-tax profit, up 64% year-over-year. However, there is significant divergence among brokerages: VDSC estimates approximately VND 5,100 billion (+52%), while another firm projects only approximately VND 3,257 billion (down 2.6%).CafeF

The wide gap stems from an expected extraordinary gain of approximately VND 2,000 billion from the transfer of the Pho Noi Urban Development project.Elibook Stripping out this one-off, core steel operations may show much more modest growth — or even a decline by some estimates. This is the critical distinction investors need when reading HPG's Q1 financials: extraordinary real estate profit does not reflect the health of the steel business.

HPG shares stood at VND 27,800 on April 13, down 0.71% from the previous session.

Banking: Positive Growth But NIM Under Pressure

Major banks in SSI Research's coverage are projected to maintain positive year-over-year growth, but the pace has slowed notably. The main driver: rising deposit interest rates since late 2025 are squeezing net interest margins (NIM).CafeF

Several banks are projected to see quarter-over-quarter profit declines from Q4/2025: CTG down approximately 41%, BID down approximately 42%, VPB down approximately 27%, MBB down approximately 26%. However, these figures compare against Q4 — a seasonally strong quarter — not against the same period last year. If the upward trend in deposit rates continues through the second half, smaller banks will face greater pressure than the Big4 due to their limited access to low-cost funding.

Under Pressure: Industrial Parks

KBC and SZC: Sharp Drops From High Base and Slow Revenue Recognition

Kinh Bac (KBC) is projected by SSI to post only approximately VND 268 billion in Q1/2026 profit, down 68% year-over-year.24hMoney The reason: Q1/2025 set a very high base with large land lease contracts, while Q1/2026 only recorded the transfer of 12 hectares at Nam Son Hap Linh Industrial Park and some social housing products.

Sonadezi Chau Duc (SZC) is also projected to see profits decline approximately 50% year-over-year to approximately VND 63 billion. Despite rental prices expected to rise to around USD 100/m² and margins remaining healthy, slow revenue recognition from land leases was the primary drag.VietnamBiz

The broader picture: northern industrial park supply has expanded aggressively to nearly 24,000 hectares, but supply growth outpaces revenue recognition speed, weighing on short-term profits. FDI tenants are also more cautious amid rising production costs from regional geopolitical tensions. The medium-term outlook remains positive thanks to 2026–2029 FDI flows favoring green industrial parks, but profits will follow handover schedules rather than arriving smoothly each quarter.

KBC shares stood at VND 34,000 on April 13, with SZC at VND 29,050.

MBS: Lessons From the First Actual Results

MB Securities (MBS) was among the first to release Q1/2026 financials, with operating revenue of VND 1,019 billion, up 52% year-over-year.CafeF Brokerage revenue surged 81% to VND 241 billion, reflecting notably improved market liquidity in the first quarter.Thương hiệu & Công luận

However, after-tax profit rose only 9% to VND 292 billion, as the proprietary trading portfolio lost more than 22%.Tuổi Trẻ This is a clear illustration of intra-company divergence: core operations (brokerage) grew strongly, but proprietary trading, subject to market volatility, dragged down total profit. Margin lending outstanding reached approximately VND 15,520 billion, up nearly VND 500 billion from the start of the year, indicating investors remain willing to use leverage.

Five Factors to Watch Over the Next Two Weeks

Q1/2026 earnings season has only just begun. Brokerage estimates are just the starting point; actual results will confirm or refute expectations. Five factors will determine the full picture:

Power sector: LNG prices and dry-season capacity deployment plans. NT2 and other gas-fired thermal power companies depend heavily on April–May weather developments.

Retail: PNJ benefits from high gold prices, but a sharp gold price correction would reverse inventory margin gains.

HPG: Actual financials will answer this season's biggest question — is core steel profit genuinely growing, or is it propped up by a one-off real estate transaction?

Industrial parks: KBC and SZC face short-term declines, but actual occupancy rates and FDI flows into electronics and semiconductors will determine the second-half outlook.

Banking: NIM is being squeezed by rising deposit rates. If this trend continues, smaller banks will face greater pressure than the Big4.

Q1 earnings season is when real data tests expectations. With divergence this extreme, picking the right sector matters more than guessing the market's overall direction.