On April 14, 2026, Hui Ka Yan officially pleaded guilty to fraud at a Shenzhen court. The man who once held $42.5 billion and topped Asia's billionaire list now faces multiple charges: fundraising fraud, embezzlement of corporate assets, and fraudulent securities issuance.HKFP The journey from peak power to the courtroom took 9 years, leaving behind approximately 1.4 million undelivered apartments and $332 billion in debt. Evergrande's collapse is not just China's story.

The core fraud: homebuyers' money never built homes

What financial reports never made clear to investors: Evergrande didn't collapse because the market turned. Evergrande collapsed because it systematically misappropriated presale deposits.NBC News

Instead of using buyers' deposits to build the projects they'd committed to, Evergrande diverted cash flows to launch new projects. The operating model resembled a real estate Ponzi scheme: money from Project A funded Project B, money from Project B funded Project C. The result was approximately 1.4 million apartments sold but never delivered, spanning over 1,300 projects across 280 Chinese cities.Marketplace

Before the trial, Hui Ka Yan had already been fined $6.5 million and permanently banned from securities markets for inflating profits.CafeBiz Chinese securities regulators determined that Hengda Real Estate inflated approximately 564 billion CNY (about $78 billion) in revenue over 2019-2020, with the 2020 inflation accounting for 78.5% of actual revenue.VnEconomy

9 years of collapse: from $42.5 billion to the courtroom

In 2017, Hui Ka Yan stood atop the world with an estimated personal fortune of $42.5 billion.CNBC Evergrande had a market cap of approximately $50 billion and owned over 1,300 projects. Its growth model relied entirely on leverage: borrow big, buy land, sell apartments on paper, then use presale deposits to borrow more.

In September 2021, the bomb detonated. Evergrande failed to meet bond interest payments, triggering the largest debt crisis in Chinese real estate history with total liabilities of approximately 2.39 trillion CNY ($332 billion).WEF In January 2024, the Hong Kong court ordered liquidation when the group failed to present a viable restructuring plan.Dân Trí By August 2025, Evergrande was officially delisted from the Hong Kong exchange, with shares at just HKD 0.163 and market cap around $282 million versus the $50 billion peak.Tuổi Trẻ

Vietnam RE on April 14: sector leads the market

On the same day as the Shenzhen trial, the VN-Index closed at 1,775.65 points, up 16.69 points (+0.95%) for its third consecutive gaining session. The real estate sector recorded the strongest gains, with VIC (Vingroup) rising 5.47% and contributing nearly 14 points to the index, while CII hit the ceiling on Thu Thiem land bank news.24hMoney

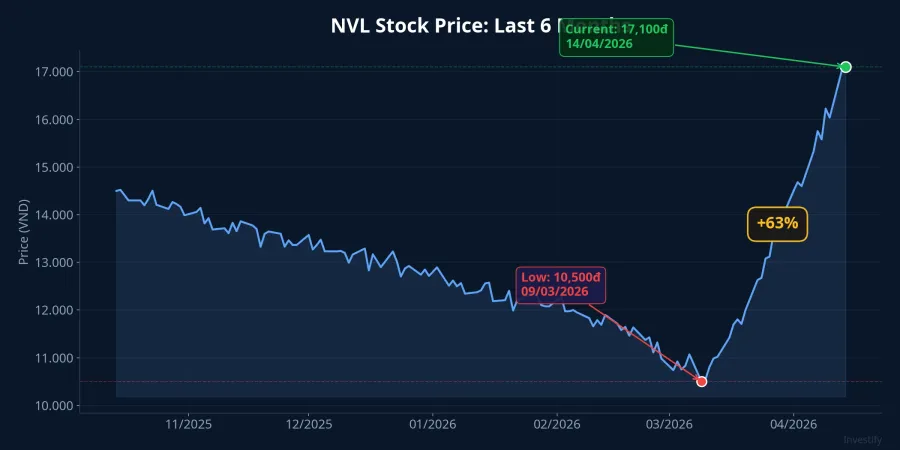

Novaland (NVL) shares surged approximately 63% in just 5 weeks, from VND 10,500 on March 9 to VND 17,100 on April 14. Year-to-date in 2026, NVL is up approximately 28% (from VND 13,350 on December 31, 2025). This is the company that was once compared to "Vietnam's Evergrande" during the 2022-2023 bond crisis.

The real risk lies here: a stock price recovery does not mean the financial foundation has recovered. And this is where Evergrande's lessons become valuable.

NVL: record revenue targets, but leverage remains very high

Novaland has set a 2026 revenue target of VND 22,715 billion, a 3.26x increase over 2025, with projected after-tax profit of VND 1,852 billion.Thời báo Tài chínhVietnamBiz To achieve this, NVL plans to deliver over 5,200 units, concentrated at Aqua City, NovaWorld Phan Thiet, NovaWorld Ho Tram, and The Grand Manhattan. The company is also pursuing capital raises through private placement of 350-800 million shares and negotiating the extension of a $300 million international bond.

However, according to Novaland's Q4/2025 earnings presentation, net debt stands at approximately VND 186,600 billion with a net debt-to-equity ratio of approximately 3.17x.Novaland IR Multiple quarters in 2024-2025 recorded deeply negative operating cash flows, reflecting payment pressures and prolonged project inventory. This leverage level is not at Evergrande's extreme, but it is firmly in the warning zone.

5 Evergrande structural risks: where does Vietnam RE stand?

From Evergrande's 9-year collapse, there are 5 structural risk categories that Vietnam RE investors should monitor.

First: short-term leverage funding long-term assets. Evergrande borrowed short to fund multi-year development projects. When credit tightened, the capital cycle broke immediately. In Vietnam, NVL has the highest debt-to-equity ratio among major RE stocks, while VHM and KDH maintain better leverage with positive cash flows.

Second: excessive dependence on presale deposits. This is the exact fraud mechanism Hui Ka Yan just pleaded guilty to: using Project A deposits to fund Project B. In Vietnam, the amended Real Estate Business Law has tightened homebuyer capital mobilization rules, but actual enforcement effectiveness still needs verification.

Third: prolonged negative operating cash flow. NVL recorded multiple quarters of negative operating cash flow in the tens of trillions of VND. When sales revenue cannot cover operating costs and debt service, companies must continuously raise new capital. This is the spiral that Evergrande fell into before breaking.

Fourth: concentrated bond maturities. 2026 is a major RE bond maturity year in Vietnam. NVL is negotiating the extension of its $300 million international bond. The negotiation outcome will be a crucial signal of the company's ability to roll over debt.

Fifth: lack of transparency in related-party transactions. Evergrande inflated revenue by approximately $78 billion over 2 years without auditor PwC detecting it. In Vietnam, transactions between parent and subsidiary companies, and the use of cross-collateralized assets, require closer investor scrutiny.

Recovery does not mean risk-free

Vietnam's RE market in Q1/2026 showed improvement signals: increasing liquidity, outperformance in leading RE stocks, and a supportive legal framework with the new Land, Housing, and Real Estate Business laws. However, according to assessments from multiple securities firms, the recovery remains uneven and heavily influenced by policy and credit factors, not yet reflecting sustainable growth in end-user demand. Mortgage rates remain high, suppressing primary market transactions.

The Evergrande story shows that the distance from "largest RE conglomerate" to "bankruptcy" can be just a few years if debt-driven growth loses control. NVL's 63% surge in 5 weeks is a notable price movement, but stock prices reflect expectations while cash flows and leverage reflect reality. When these two diverge too widely, the risk always tilts toward latecomers.

Three signals worth monitoring next quarter: actual delivery progress at Aqua City and NovaWorld, the outcome of NVL's $300 million international bond extension negotiations, and the Q1/2026 financial report. These will be the data points revealing whether this recovery has substance or is merely expectations outrunning reality.