Goldman Sachs just posted one of its best quarters in years: EPS came in at $17.55, beating the consensus estimate by 6.4%. Revenue reached approximately $17.23 billion, with net profit up 19% year-over-year. Yet on April 13, GS shares fell roughly 4%, closing around $907.80. The numbers tell the story: it's not the profit level that disappointed Wall Street, but the quality of that profit.CNBC

Record equities revenue driven by market volatility

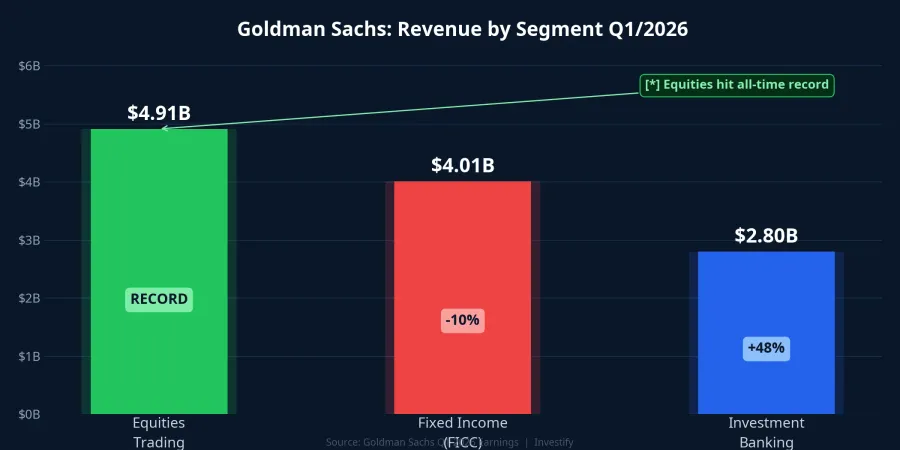

The equities trading division generated approximately $4.91 billion in Q1/2026 revenue, up about 17% year-over-year — an all-time record for Goldman Sachs. Equities intermediation revenue surged 27%, reflecting a sharp increase in hedging demand from institutional clients.

The primary driver was elevated market volatility amid the Strait of Hormuz crisis. Brent crude jumped to $101.66/barrel on April 13, a 6.78% single-day gain. The VIX rose 11.9% to 21.58 points. When volatility spikes, institutional clients trade more actively to hedge and rebalance portfolios, generating record revenue for Goldman's trading desks.

This wasn't a Goldman-specific phenomenon. Analysts had forecast total Q1 trading revenue for the five largest banks (Goldman Sachs, JPMorgan, Morgan Stanley, Bank of America, Citigroup) could reach $40 billion, the highest in years.Seeking Alpha Goldman, as the first to report, confirmed this trend.

FICC disappoints, exposing structural imbalance

While equities surged, FICC (fixed income, currencies, and commodities) moved in the opposite direction. FICC revenue came in at $4.01 billion, down 10% year-over-year. This is a significant decline for a division that typically accounts for a large share of Goldman's trading revenue.

The key insight here: high volatility does not guarantee high profits across all divisions. The bond market in Q1 saw reduced trading activity as investors adopted a "wait and see" posture amid Fed rate policy uncertainty. A flatter yield curve compressed interest rate spread opportunities. While commodities saw sharp oil price swings, the volatility was concentrated at quarter-end and didn't generate enough cumulative trading revenue.

Wall Street pays particular attention to FICC because it's considered a measure of defensive earnings quality for investment banks. When FICC weakens, the question becomes: is the record equities profit sustainable, or just a product of an abnormal volatility phase unlikely to repeat in Q2?

Expectations ran ahead: when "beating" isn't enough

This is the most important layer. Goldman reported EPS of $17.55 versus the $16.49 consensus — a 6.4% beat. Normally, the stock should have rallied. But markets operate on a "buy the rumor, sell the news" dynamic.Yahoo Finance

Before the announcement, analysts had been steadily raising expectations based on extreme Q1 market volatility. "Whisper numbers" — the unofficial expectations that traders actually position around — were likely significantly higher than the $16.49 consensus. In other words, GS shares had already priced in strong results before the official release.

Adding to the concern, earnings quality was questioned. Most of the EPS beat came from equities trading — a revenue source that fluctuates sharply with market cycles. In a period when investors prioritize stability, fee-based revenue from advisory and asset management carries more weight than trading profits. While investment banking rose an impressive 48% year-over-year with advisory fees reaching approximately $2.8 billion, the FICC shortfall still dominated the overall assessment.

Macro context: Hormuz pressure overshadowed April 13

GS didn't decline in a vacuum. The April 13 session saw broad selling pressure across U.S. markets as Hormuz tensions escalated. Brent crude surged to $101.66/barrel, up 6.78% on the day — the sharpest gain in weeks.

In this environment, even record results weren't enough to counter defensive sentiment. Investors chose to take profits on financial stocks — which had already rallied in anticipation of strong earnings — to reduce exposure ahead of geopolitical volatility. Three factors converged in a single session: FICC disappointed, whisper numbers exceeded consensus, and Hormuz-driven risk-off dominated positioning.

Implications for JPMorgan and Morgan Stanley

Goldman Sachs is often viewed as the bellwether for big bank earnings season. Its Q1 results raise two key questions for banks reporting next.

JPMorgan Chase — with a larger FICC operation than Goldman — will face intense scrutiny on this division. If JPMorgan's FICC also decelerates, it confirms that the Q1 bond market was genuinely challenging industry-wide, not just a Goldman-specific issue. However, JPMorgan benefits from its retail banking and asset management divisions, which provide revenue stability.

Morgan Stanley — more dependent on investment banking and wealth management — could benefit from the positive IB signal (48% growth at Goldman). But if FICC weakness persists across the industry, cautious sentiment will likely continue to dominate.

Lessons for Vietnamese investors

Goldman Sachs' results carry two messages for investors in the Vietnamese market.

First, volatility creates opportunities for some sectors, but not all. The VN-Index closed at 1,758.96 points on April 13, up a modest 0.51%. Amid rising global volatility, oil and gas stocks (GAS, PVD, PVT) and fertilizer companies could benefit similarly to how Goldman's equities trading profited from volatility. But sectors facing high fuel costs (airlines, logistics) will come under pressure.

Second, expectations running ahead is always a risk. In Vietnam, the official FTSE upgrade on September 21, 2026 has already been partially priced into many blue-chip stocks. The Goldman lesson — beating consensus but missing whispers — is a reminder that stocks can decline even on positive news, if that news was already priced in.

Conclusion

Goldman Sachs Q1/2026 reveals a picture that is strong but structurally imbalanced. Equities broke records, investment banking rose 48%, but FICC fell 10% and expectations had already outrun the stock price. The core issue is earnings quality: when most of the EPS beat comes from volatility-dependent trading, the market is justified in questioning sustainability. FICC weakness and Hormuz risk-off are specific short-term risks, but they don't reverse the conclusion that Goldman remains well-positioned if volatility persists.

Q1 earnings season on Wall Street has only just begun. Three factors to watch next week: JPMorgan's FICC results, Morgan Stanley's M&A outlook, and whether Hormuz tensions will translate into higher global cost of capital.