Warren Buffett just admitted something rare: he was wrong. "I sold too soon," he said about cutting Berkshire Hathaway's Apple position by 75%. But the next sentence is the real lesson: "Not in this market." Knowing you sold too early yet still refusing to buy back isn't contradiction. It's valuation discipline.

This article analyzes 3 portfolio management principles from Buffett's strategy, and how Vietnamese investors can apply them as the VN-Index recovers strongly while macro risks persist.

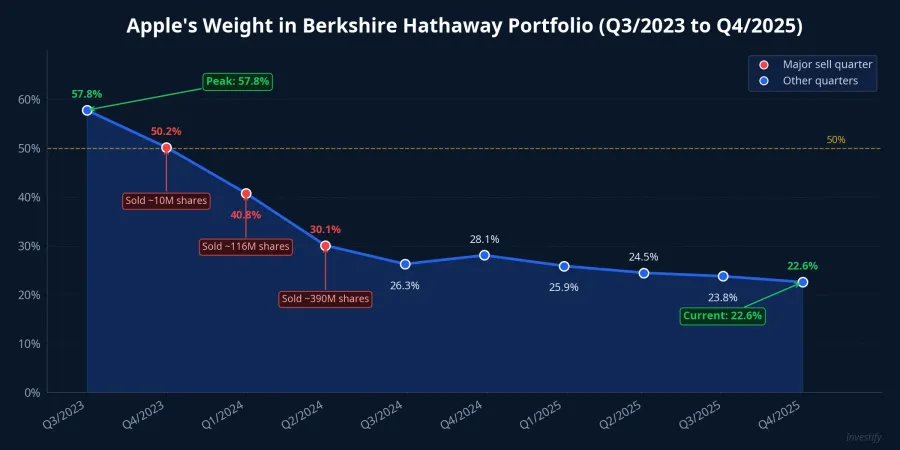

Context: From Over 50% Down to 22.6% of Portfolio

At the end of Q3/2023, Berkshire Hathaway held 915 million Apple shares, accounting for over 50% of its listed equity portfolio. Over the following 9 quarters, Berkshire sold approximately 687 million shares, reducing the position by 75%.Motley Fool

By end of 2025, Apple remained Berkshire's largest holding at $61.96 billion, approximately 22.6% of the portfolio.CNBC New CEO Greg Abel, in his first shareholder letter, confirmed Apple as a core position expected to see little change going forward.Motley Fool

So why sell? Buffett explained candidly: "I wasn't comfortable when it was as big as virtually everything else combined."

Lesson 1: Don't Let One Stock Dominate Half Your Portfolio

Think of it simply: even though Apple is an exceptional business, when a single stock occupies over 50% of your portfolio, any unexpected event could send half your wealth plunging in a few sessions. An antitrust ruling, supply chain disruption, or weakness in the Chinese market are all risks that cannot be predicted in advance.

Buffett wasn't bearish on Apple. He reduced the position based on principle: no single investment, however good, should dominate the entire portfolio. This is concentration risk management, not pessimism.

What does this mean for your portfolio? Many Vietnamese retail investors currently hold portfolios concentrated in just 1-2 stocks, especially during the period when VN-Index recovered from its low of 1,591 points (March 23) to 1,758.96 points (April 13), gaining approximately 10.5% in 3 weeks. When markets rise fast, the natural tendency is to pile into the "best performer." But this is precisely when position sizing needs review.

A simple rule: if any single stock exceeds 20-25% of your portfolio, consider trimming to a safer level, regardless of how much you believe in the business.

Lesson 2: When Earning Yield Falls Below the Risk-Free Rate, Stocks Lose Appeal

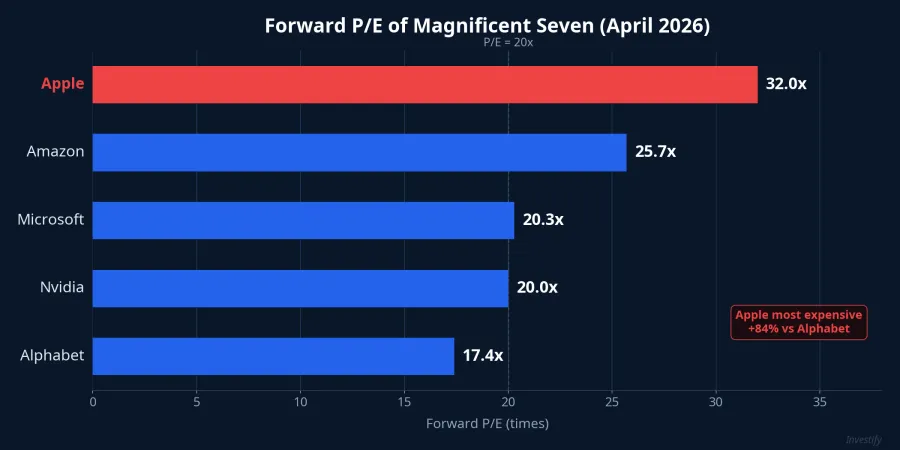

Put simply, earning yield is the "return" each dollar invested in a stock generates, calculated as the inverse of P/E. Apple currently trades at a trailing P/E of approximately 33x, equivalent to an earning yield of around 3.1%. Forward P/E is approximately 32x.CompaniesMarketCap

Among the Magnificent Seven, Apple is the most expensive:

| Stock | Forward P/E | Estimated Earning Yield |

|---|---|---|

| Alphabet | ~17.4x | ~5.7% |

| Nvidia | ~20x | ~5.0% |

| Microsoft | ~20.3x | ~4.9% |

| Amazon | ~25.7x | ~3.9% |

| Apple | ~32x | ~3.1% |

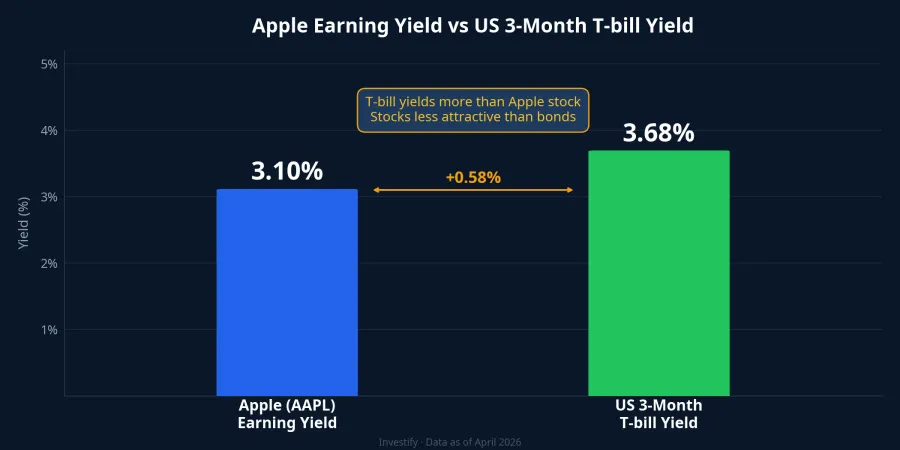

Apple's earning yield (~3.1%) is lower than the US 3-month T-bill yield at 3.68%.Trading Economics In other words, each $1 invested in Apple "earns" less than $1 parked in near-zero-risk US Treasury bills.

This is Buffett's logic: when stock earning yield falls below the risk-free rate, the incentive to buy stocks decreases significantly, unless investors expect very strong future earnings growth.

What about Vietnam? The VN-Index has an estimated P/E of around 12-13x, translating to an earning yield of approximately 7.7-8.3%. The 12-month savings rate at major banks is currently around 5-5.5%. The spread remains fairly wide, suggesting Vietnamese equities are not "expensive" by this metric compared to the US market. However, this is an index-level comparison. Many individual stocks trade at P/E of 25-30x with earning yields of just 3-4%, not far from savings rates. Investors should check the earning yield of each stock in their portfolio rather than relying solely on the VN-Index.

Lesson 3: Cash With Yield Is a Weapon, Not a Waste

This is perhaps the most important lesson and the one least noticed by retail investors.

As of end 2025, Berkshire held $369 billion in cash and equivalents, with approximately $305 billion in short-term US Treasury bills (T-bills).Berkshire Hathaway Berkshire now holds approximately 5% of the entire US T-bill market, making it one of the four largest T-bill holders in the world.CNBC

At a 3-month T-bill yield of approximately 3.68%, this asset pile generates an estimated $11+ billion in annual interest income for Berkshire, virtually risk-free. For context, the total net profit of many large Fortune 500 companies is lower than this figure.

More importantly, T-bills give Berkshire "free optionality": when markets collapse and stocks become cheap, Berkshire has hundreds of billions ready for immediate deployment. This is how Buffett earned outsized returns during the 2008-2009 crisis by investing in Goldman Sachs, Bank of America, and General Electric on favorable terms.

The takeaway is simple: idle cash shouldn't "die" in a brokerage account earning near-zero interest, nor should 100% of capital be allocated to stocks. Allocating a portion of the portfolio to fixed-income instruments (bank savings at 5-5.5%/year at major banks, or fixed-income products with higher yields) both generates passive income and maintains liquidity to seize opportunities during market corrections.

With the VN-Index having recovered 10.5% from its low yet breadth on April 13 remaining weak (140 advancing vs. 187 declining stocks), keeping a portion of capital in safe yield-bearing instruments is not pessimism. It is discipline.

Three Rules Summarized

Don't let any single stock exceed 20-25% of your portfolio. Concentration risk is real, regardless of conviction. Buffett trimmed Apple not because he was bearish, but because 50% was simply too large.

Compare earning yield to the risk-free rate. When the spread narrows or inverts (stock yield falls below bond yield), that's a signal to reassess positions. In Vietnam, check individual stocks, not just the index P/E.

Cash with yield is a strategic weapon. Allocate a portion to fixed-income instruments to both earn returns and maintain the ability to act when opportunities appear.

Buffett doesn't fear missing out (FOMO). He fears overpaying. Berkshire's Q1/2026 report (expected in May) will reveal whether Berkshire continued trimming Apple or began buying back at lower prices following the March correction. That is a signal worth watching next month.