April marks the peak of Vietnam's 2026 annual general meeting (AGM) season. Hundreds of listed companies have presented their business plans, dividend proposals, and capital-raising strategies to shareholders. Looking at the numbers from dozens of AGMs over the past two weeks, the overall picture reveals a stark bifurcation between companies confidently going on offense and those pulling back into defensive mode.

This article distills the five most important signals from the AGM season, helping individual investors position their portfolios for the second half of the year.

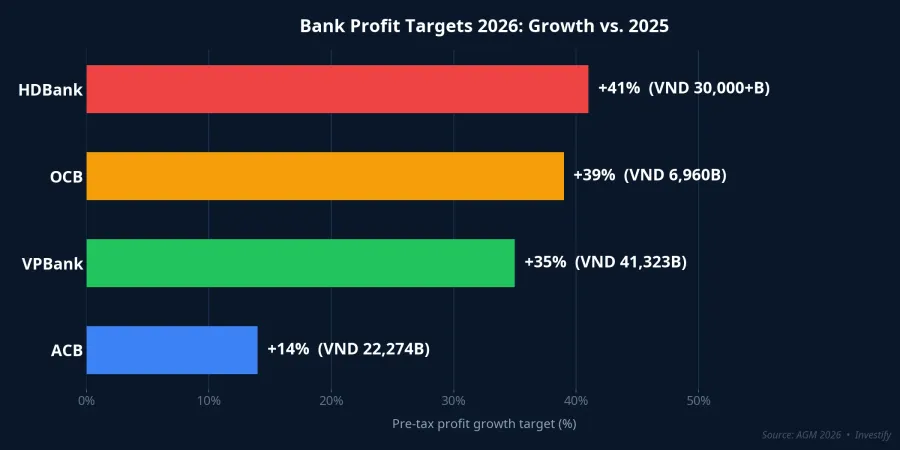

Banks race to raise capital, targeting record profits

The banking sector is the most confident group in the 2026 AGM season, with profit growth targets ranging from 14% to 41%.

HDBank targets pre-tax profit exceeding VND 30,000 billion, a 41% increase over 2025, with total assets aiming for VND 1,194,000 billion.NLĐ OCB targets VND 6,960 billion in pre-tax profit (+39%), while raising charter capital to VND 30,625 billion through issuing 399 million shares.CafeF VPBank sets consolidated pre-tax profit at VND 41,323 billion (+35%), while aiming to raise charter capital to VND 100,000 billion.MekongASEAN ACB presents a VND 22,274 billion pre-tax profit plan (+14%), built on an already high 2025 base.VnEconomy

The dividend race is equally noteworthy. This year, banks are pushing cash dividends harder than before: VPBank pays a total of 31% (5% cash + 26% stock), MBB distributes approximately VND 8,055 billion in cash dividends (10% ratio) plus 15% in stock, and ACB pays 20% (7% cash + 13% stock).CafeF HDBank maintains a 30% stock-only dividend.DNSE

Why do banks need to raise capital so aggressively? Two main reasons. First, meeting Basel III and capital adequacy ratio (CAR) requirements as credit growth accelerates. Second, preparing for FTSE Russell's upgrade of Vietnam to Emerging Market status (effective September 2026); banks are the most favored stocks by foreign investors in the FTSE EM basket. These two factors create capital-raising pressure, but also reflect genuine confidence in business prospects.

Real estate sets ambitious plans, but verification needed

The real estate sector impresses with plans showing revenue and profit growth in multiples, but investors need to distinguish between real capacity and aspirations.

Vinhomes (VHM) targets VND 50,000 billion in after-tax profit, a 15% increase over VND 43,335 billion achieved in 2025.FILI More notably, VHM plans to pay VND 24,644 billion in cash dividends (60% of charter capital, equivalent to approximately $1 billion), plus a 100% stock dividend.VietnamFinance This is the largest dividend payout in the history of Vietnam's stock exchange.

Taseco Land targets consolidated revenue of VND 11,062 billion, roughly 3x the 2025 level, with after-tax profit of VND 2,512 billion, nearly 4x growth, driven by 19 projects being developed simultaneously.CafeF Khang Dien (KDH) targets VND 1,500 billion in after-tax profit, with the main driver being the Gladia by the Waters project, a joint venture with Keppel.Vietstock Dat Xanh (DXG) targets VND 5,000 billion in revenue (+19%) and VND 268 billion in after-tax profit, while planning a name change and 34% bonus share issuance.Reatimes

Investors should note: real estate plans depend heavily on project legal progress and market liquidity. In 2024-2025, many real estate companies set ambitious targets but failed to deliver. Q1/2026 results (released in late April) will be the first reality check.

Blue chips lower targets: defensive or expectation management?

A series of large-cap companies set 2026 profit targets below their 2025 actual results, despite many having just recorded record-profit years.

Vincom Retail (VRE) targets VND 5,375 billion in after-tax profit, down 17% from the record VND 6,446 billion in 2025, even as revenue is projected to grow 16%.TNCK Vicostone (VCS) targets VND 744 billion in pre-tax profit, down 10.6%, citing slow global construction recovery.Báo Đấu thầu PV GAS (GAS) proposes VND 8,801 billion in after-tax profit, approximately 22% lower.TNCK GELEX (GEX) expects revenue to rise 13.2% but pre-tax profit to decline 21.8%.Tuổi Trẻ

Looking at the numbers, three main reasons explain the trend. First, macro uncertainty: Vietnam's CPI sits at 4.65%, with input costs rising due to Middle East conflicts. Second, expectation management strategy: setting low targets to easily exceed them and maintain credibility with shareholders. Third, sector-specific cost pressures: PV GAS faces gas price volatility, while Vicostone is squeezed by weak global construction demand.Tuổi Trẻ

An important distinction: for state-owned enterprises (SOEs) like GAS and PVT, setting conservative targets is a governance tradition — they routinely exceed plans in actual results. But for private companies like Vicostone, a 10-year profit low warrants more caution.

The gap between broker forecasts and company plans

Securities brokers forecast overall market profit growth of approximately 18% for 2026, with VN-Index potentially reaching the 1,670-1,750 range by year-end.Tuổi Trẻ However, when examining individual company targets, the picture diverges sharply:

| Sector | Company targets | Broker forecasts |

|---|---|---|

| Banking | +14% to +41% | +15% to +20% |

| Real estate | +15% to 4x | +20% to +30% |

| Oil & gas | -19% to -22% | Depends on oil prices |

| Manufacturing (VCS, QNS) | -10% to -19% | Neutral |

| Consumer (VNM) | +4.4% | +5% to +8% |

When brokers are more optimistic than company targets, two scenarios emerge. Scenario 1: companies are being tactically conservative and will beat plans — a positive signal if Q1 results are strong. Scenario 2: brokers are too optimistic, risking forecast downgrades in the second half. Q1/2026 results will serve as the reality check for both scenarios.

Vinamilk: a defensive shield amid market bifurcation

Vinamilk (VNM) targets VND 66,477 billion in revenue (+4.3%) and VND 9,828 billion in after-tax profit (+4.4%), with a commitment to pay at least 50% of profits as cash dividends.CafeF Modest growth, but a high level of stability given rising CPI and volatile raw material costs.

In a bifurcated market, Vinamilk represents the defensive equity play: slow but steady growth, high cash dividends, few negative surprises. This is a fit for the stable capital portion of a portfolio, not for expectations of breakout growth.

Four common mistakes when reading AGM plans

Equating "ambitious plan" with "stock will rise." Real estate plans showing 3-4x growth sound exciting, but they depend entirely on project delivery timelines. If legal processes stall, revenue gets pushed to the following year.

Ignoring the "lowered target" signal. Lowered targets are not always negative. For SOEs like GAS, it is tradition. But for private companies like Vicostone, a 10-year profit low is a genuine warning sign.

Looking only at growth percentages without considering the base. HDBank's +41% sounds more impressive than ACB's +14%, but ACB's 2025 profit base was already very high (VND 19,500 billion). Absolute values matter.

Not distinguishing cash vs. stock dividends. VPBank pays 31% total, but only 5% is cash (equivalent to a yield of approximately 1.95% at VND 27,400/share). HDBank's 30% is entirely stock — no real cash flow for shareholders. Investors seeking income should prioritize MBB (10% cash, equivalent to VND 8,055 billion) or ACB (7% cash).DĐĐN

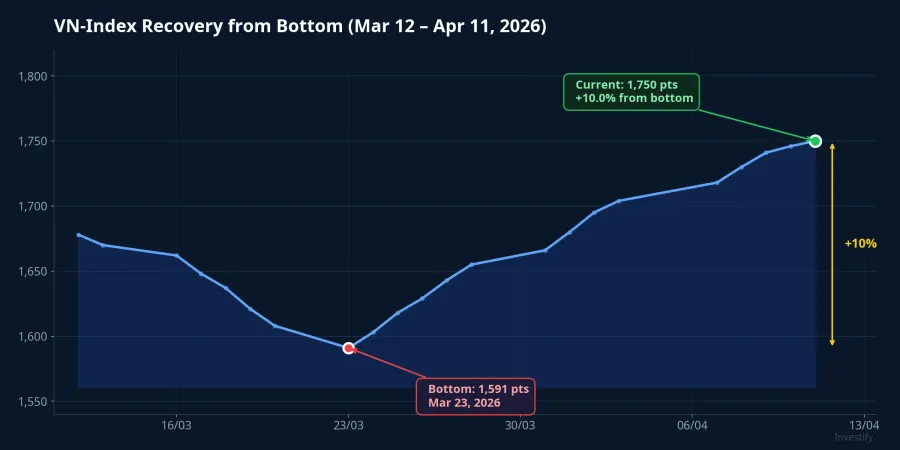

VN-Index: recovery underway, but expectations already priced in

VN-Index stands at 1,750 points, having recovered approximately 10% from the 1,591-point bottom on March 23. The market is trading right at the average broker forecast zone (1,670-1,750 points for year-end), suggesting expectations are largely priced in.

This means: upside from current levels depends on companies' ability to exceed plans, not on already-known expectations. Q1/2026 results, starting to be released from late April, will be the most important test.

Conclusion: bifurcation is the theme, Q1 is the test

The 2026 AGM season reveals two distinct groups. The offensive group includes banks and select real estate companies, setting aggressive growth targets, actively raising capital, and expressing confidence in the credit cycle and FTSE upgrade. The defensive group includes oil & gas, manufacturing, and retail, lowering expectations due to rising input costs and weak global demand.

Three factors worth monitoring in April and May: Q1/2026 business results (late April) will show who is on track; the State Bank's interest rate decisions amid 4.65% CPI pressure; and concrete progress on the FTSE upgrade roadmap ahead of the September effective date. The actual Q1 numbers will help distinguish between credible AGM plans and those that exist only on paper.