Deposit VND 500 million in a 12-month term at Vietcombank at 5.9% per year, and you receive VND 29.5 million in interest. Sounds decent. But with March 2026 CPI just reported at 4.65% year-on-year, rising prices have eroded approximately VND 23.25 million of purchasing power on that principal. Real interest remaining: VND 6.25 million, equivalent to roughly one-third of a tael of SJC 99.99 gold ring at the current price of VND 170.6 million per tael.

Put simply: nominal interest is the number on paper; real interest is the actual purchasing power you gain after 12 months. And that real number is very small right now.

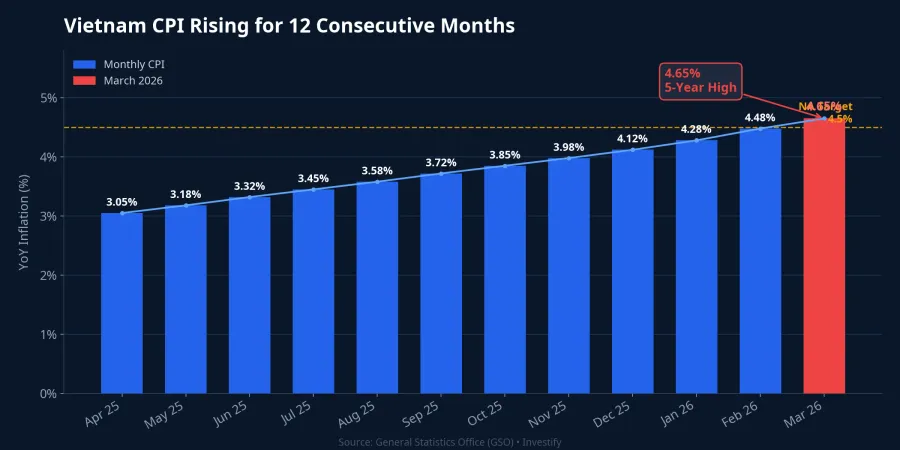

March 2026 CPI: 5-year high, exceeding National Assembly target

According to the General Statistics Office, March 2026 CPI rose 4.65% year-on-year, the highest March reading in five years, exceeding the 4.5% control target set by the National Assembly for 2026.VnEconomy Core inflation also rose 3.96% YoY. Compared to February 2026 (CPI up 3.35% YoY), the acceleration was sharp: from 3.35% to 4.65% in just one month. Average Q1/2026 CPI reached 3.51%.Tạp chí Công Thương

Main driver: energy and transportation

Transportation was the largest contributor, directly sensitive to fuel prices. The transportation group rose 12.85% month-on-month, contributing 1.28 percentage points to headline CPI. Within this group, gasoline prices surged 29.72% and diesel rose 57.03% compared to February.VOV

E5 RON92 gasoline jumped from approximately VND 18,630/liter (February 2026) to a peak of VND 30,110/liter (March 24) before adjusting down to VND 22,340/liter at the April 9 review. Brent crude also rose from $72.87/barrel (February 27) to $95.35/barrel (April 10), a roughly 31% increase in under six weeks, driven by tensions at the Strait of Hormuz.

Beyond transportation, the housing and construction materials group rose 5.69% YoY due to climbing rental and urban service costs. Food and dining services rose 4.55% YoY, mainly from pork prices and dining-out costs. A rare bright spot: the food staples group declined slightly (grains -0.06%, food products -1.41%).

Big4 savings rate at 5.9%: real yield just 1.25%

The Big4 banks (Vietcombank, BIDV, VietinBank, Agribank) all currently list 12-month savings rates at 5.9% per year, up significantly from 5.0-5.2% a year ago.VietnamBiz Vietcombank has also just announced a rate cut for 24-month terms to 6.0%, effective April 13, 2026.Kênh14

What does this mean for your wallet? With VND 500 million at Big4:

| Item | Amount |

|---|---|

| Principal | VND 500,000,000 |

| Nominal interest (5.9%/year) | VND 29,500,000 |

| Purchasing power lost (CPI 4.65%) | VND 23,250,000 |

| Real interest | VND 6,250,000 |

VND 6.25 million in real interest on VND 500 million, roughly one-third of a tael of SJC 99.99 gold ring at VND 170.6 million per tael. If you had deposited a year ago at just 5.0%, real interest would have been even worse: approximately VND 1.75 million (0.35%).

Some smaller banks are pushing rates higher. LPBank lists 7.4%/year, Techcombank 7.25%, PGBank and OceanBank 7.2% for 12-month terms.VietnamNet At 7.4%, real yield reaches approximately 2.75%; better than Big4 but still modest against current inflation.

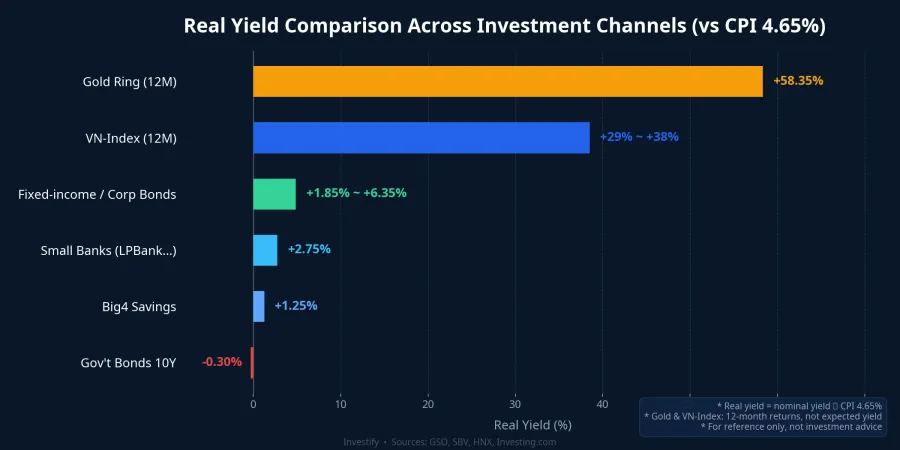

Real yield comparison: who's beating inflation?

With CPI at 4.65%, real yields (nominal return minus inflation) diverge sharply across channels.

Bank savings remain the safest channel (Deposit Insurance covers up to VND 125 million per depositor per institution), but real yields are low: Big4 offers approximately +1.25%, smaller banks approximately +2.35% to +2.75%.

Government bonds at the 10-year tenor yield 4.35%, the highest since March 2023.Investing.com However, after subtracting CPI at 4.65%, real yield is negative: -0.30%. The so-called risk-free channel is actually failing to preserve purchasing power.

Corporate bonds and fixed-income products available to retail investors through fintech platforms typically yield 6.5%-11% per year, producing real yields of approximately +1.85% to +6.35%. However, credit risk is higher, especially after the Vạn Thịnh Phát/SCB scandal; and private-placement corporate bonds are currently restricted to professional investors (assets ≥VND 2 billion, maintained for 180 consecutive days).

SJC 99.99 gold rings peaked at VND 187.9 million/tael (March 2, 2026) before declining to VND 170.6 million/tael (April 11). Over 12 months from April 2025 (approximately VND 104.4 million/tael), gold rings rose approximately 63%. However, this gain included a volatile period driven by Middle East conflict and Decree 232/2025 breaking SJC's monopoly. In just the most recent month, gold rings fell approximately 6.7%. Gold is highly volatile, and past returns do not guarantee future performance.

VN-Index closed at 1,750 points (April 12, 2026), up approximately 43% from 1,222 points at the same time last year. Most of this gain came from recovery off the April 2025 bottom when VN-Index fell to the 1,094-1,168 range during the global selloff. From the more stable late-March 2025 level (approximately 1,307 points), the gain was still approximately 34%. However, equities carry high risk: in the first week of April 2025 alone, VN-Index dropped over 13%.

Note: Gold and VN-Index figures are trailing 12-month returns, not expected yields. Savings and bond figures are current fixed rates.

Inflation outlook: pressure not over yet

Macro reports forecast average 2026 CPI in the 3.7%-4.3% range, with multiple risk factors still active.VnEconomy

Brent crude remains above $95/barrel as Middle East tensions show no signs of easing. Each domestic fuel price adjustment will continue to directly impact CPI. Additionally, electricity, water, and healthcare prices are scheduled to increase in 2026; the USD/VND exchange rate is also under pressure as the dollar strengthens, raising import costs.

The favorable factor is that food staples remain in decline, and domestic demand has not heated up enough to create demand-pull inflation. If oil prices ease, CPI momentum could weaken from late Q3. But if oil prices stay elevated and the exchange rate remains volatile, CPI could stay above 4% for most of the first half of the year.

Asset allocation instead of all-in savings

The 4.65% CPI story does not negate the role of bank deposits; they remain a safe, highly liquid channel suitable for emergency reserves. But when inflation outpaces deposit rates, keeping 100% of assets in savings means accepting gradual purchasing power erosion.

No channel is perfect. Gold rose approximately 63% over 12 months but also fell approximately 6.7% in just the most recent month. VN-Index gained approximately 43% but once dropped over 13% in a single week. Big4 savings are safe but yield just 1.25% real. The key lies in allocation, not choosing a single channel.

Inflation at 4.65% sends a clear signal: savings rates are losing the race against prices. For those keeping all assets in savings accounts, this is a moment to reconsider allocation. The decisive factors in coming months are oil prices and the State Bank's interest rate policy: if Brent falls below $80/barrel and the SBV continues raising the policy rate, real savings yields will improve significantly. Conversely, if oil stays elevated, purchasing power erosion will continue for at least two more quarters.

Three factors to monitor in April-May: the April CPI reading (released at month's end), the SBV's policy rate decision, and Brent crude developments around the Strait of Hormuz.