The big picture reveals a rare week across Asian financial markets. Two global-scale events occurred almost simultaneously: FTSE Russell confirmed Vietnam's upgrade to Secondary Emerging Market status, and the US and Iran reached a 2-week ceasefire agreement mediated by Pakistan. The result was an April 8 rally of 79 points on VN-Index, the largest absolute single-day gain in the index's history. But on the other side of the globe, US consumer confidence hit a 70-year historic low, reminding investors that this recovery is playing out against an unstable macro backdrop.

FTSE Russell Confirms Upgrade: $6 Billion in Potential Capital Flows

On Monday morning April 7, FTSE Russell officially confirmed that Vietnam meets all criteria for classification as a Secondary Emerging Market.CNBC Inclusion in the global index suite will take effect from the September 21, 2026 review, phased across 4 tranches through September 2027 with weightings of 10%, 20%, 35%, and 35% respectively.The Investor

FTSE Russell estimates this could redirect up to $6 billion in capital flows to Vietnam, with passive ETF flows alone accounting for approximately $500 million to $1 billion.Yahoo Finance However, actual disbursement will follow the 4-tranche schedule over 12 months, not all at once. Investors should distinguish between long-term expectations and short-term effects.

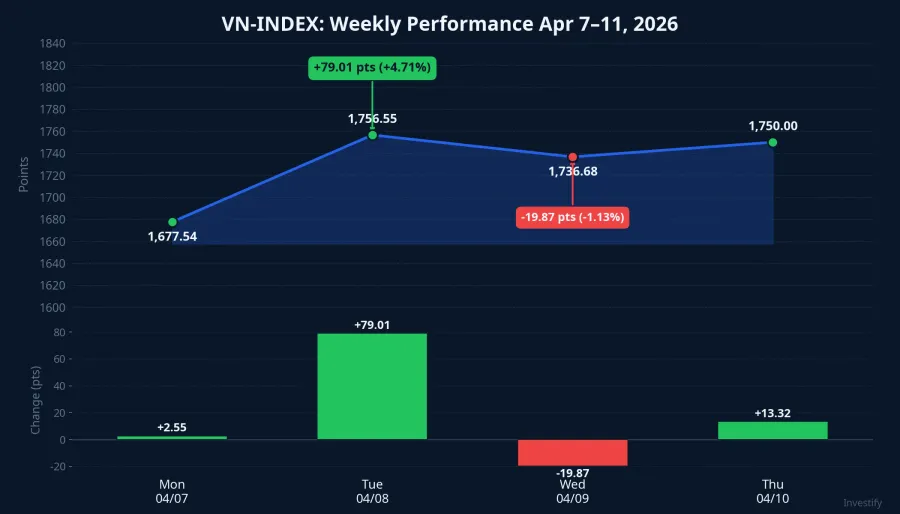

Monday's market reaction was cautious. VN-Index closed at 1,677.54 points, up just 0.15% on volume of 608.7 million shares. The market needed time to digest the news.

April 8: VN-Index Surges 79 Points, an All-Time Record

April 8 recorded the strongest session in VN-Index history. The index jumped 79.01 points (+4.71%) to 1,756.55, the largest absolute point gain ever recorded.VnExpress

Liquidity surged with 1.26 billion shares matched, equivalent to VND 34,921 billion, more than doubling the previous session.Petrotimes Market breadth was overwhelming: 322 stocks advanced, only 27 declined, and 25 hit the ceiling.Vietnam.vn

Two factors converged to drive the rally. First, the FTSE upgrade effect fully transmitted after Monday's cautious session, as domestic capital aggressively bought stocks likely to be included in the FTSE index. Second, the US-Iran 2-week ceasefire announcement came the same day, mediated by Pakistan, releasing geopolitical risk that had accumulated over 6 weeks of conflict.Al Jazeera The Strait of Hormuz was expected to reopen, causing Brent crude to plunge 13.3% from $109.27 to $94.75 per barrel in the session.

Profit-Taking and Foreign Flows: Mixed Signals

On Wednesday April 9, profit-taking pressure emerged. VN-Index corrected 1.13% to 1,736.68 points, though liquidity remained above 1 billion shares. For the full week, foreign investors were net sellers of approximately VND 3,100 billion on HOSE, reflecting portfolio restructuring ahead of the official upgrade.Dân Việt

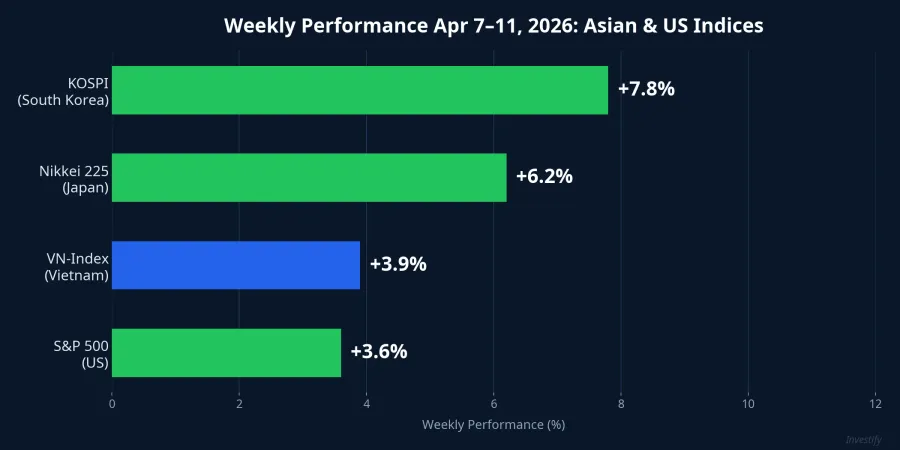

However, Thursday's final session (April 10) brought a reversal signal. Foreign investors turned net buyers at approximately VND 940 billion, concentrating on TCB (+VND 217B), HPG (+VND 179B), MBB (+VND 100B), and VNM (+VND 94B). Proprietary trading desks also bought a net VND 400 billion.Vietstock VN-Index closed the week at 1,750 points, up 3.9% from the prior week.

The question remains: was Thursday's net buying the beginning of "front-running" flows ahead of the upgrade, or merely a technical rebalancing after three sessions of net selling? The evidence is insufficient to confirm a clear direction.

Asia-Wide Recovery

VN-Index was not the only market to surge. KOSPI (South Korea) gained approximately 7.8% for the week, with Wednesday's 6.87% jump marking the strongest session in over 17 years.KED Global Nikkei 225 (Japan) rose approximately 5.4% on Tuesday, leading Asia's recovery as plunging oil prices reduced energy costs for the import-dependent economy.Japan Times The S&P 500 also gained approximately 3.6%, with the Dow Jones up 3.0%.

Three key drivers: reduced geopolitical risk as Hormuz was expected to reopen; expectations of cooling inflation from lower oil prices; and market-specific factors, with KOSPI benefiting from the chip/AI sector, Nikkei from semiconductors, and VN-Index from the FTSE catalyst.

Warning Signal: Michigan Sentiment Hits 70-Year Low

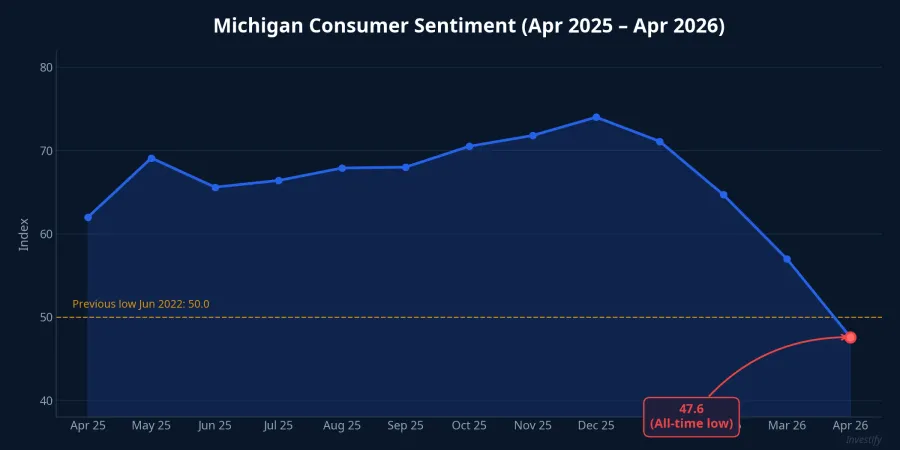

Amid the Asian optimism, a concerning signal emerged. The Michigan Consumer Sentiment Index for April 2026 (preliminary) fell to 47.6 points from 53.3 the previous month, the lowest reading in the survey's entire 70-year history, below even the 2022 inflation crisis trough of 50 points and the 2008 financial crisis.CNBC

One-year inflation expectations surged to 4.8% from 3.8%, the largest single-month increase since April 2025.Benzinga Long-term inflation expectations rose to 3.4%, the highest since November 2025. Notably, 98% of the survey was conducted before the ceasefire agreement, meaning the data reflects sentiment during peak conflict.FinancialContent

This signal has two implications for Vietnam's market. First, if US consumer spending weakens in Q2, Vietnamese exports to the US could be affected. Second, the Fed will find it difficult to cut rates while inflation expectations remain elevated, narrowing the scope for monetary easing and potentially pressuring capital flows to emerging markets. However, if peace talks progress and oil prices continue to decline, this index could improve in the end-of-month survey.

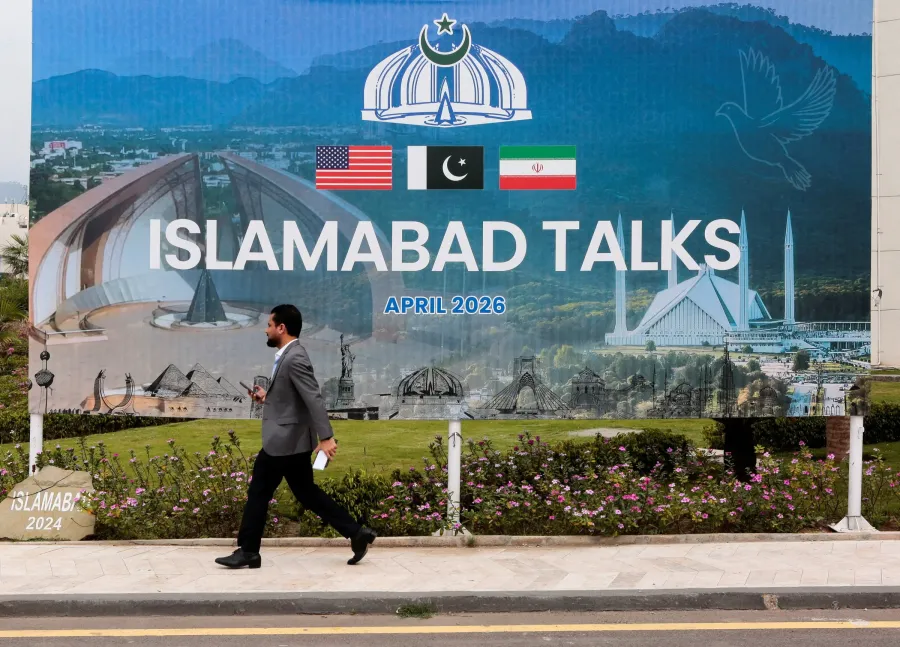

Pakistan Talks: The Biggest Variable

The US-Iran peace process is underway in Islamabad. US Vice President J.D. Vance met with Pakistani Prime Minister Shehbaz Sharif in the highest-level negotiations between the US and Iran since 1979.CNBC Key negotiating points include: Iran's nuclear program, missile restrictions, reopening the Strait of Hormuz, and sanctions relief.

However, Iran rejected the 45-day ceasefire framework draft proposed by Pakistan on April 5, and put forward its own 10-point peace plan instead.Wikipedia The weekend talks will determine whether the ceasefire gets extended or proves to be a temporary pause. Brent crude closed the week at $95.35 per barrel, down approximately 12.5% from the start of the week ($109.03).

Next Week: Three Determining Factors

The week of April 7-11 confirmed that the FTSE upgrade and the US-Iran ceasefire were catalysts powerful enough to produce a historic rally. But whether the momentum is sustainable depends on three factors in the week of April 14-18.

First, the outcome of the Pakistan talks. If an extended agreement is reached, Brent could continue declining toward $90/barrel; if talks collapse, oil could return above $100. Second, the Fed's response to rising inflation expectations. Any rhetoric suggesting higher-for-longer rates would affect emerging market capital flows. Third, foreign investor flows. VN-Index sits at the MA50 technical resistance zone (1,750 points); if it breaks through and holds, the probability of a short-term uptrend increases.

The current picture leans positive thanks to two major catalysts, but Michigan Sentiment at 47.6 and the weekly net foreign selling of VND 3,100 billion are two factors that demand close monitoring. The Pakistan talks outcome and early next week's foreign flow data will provide clearer answers.