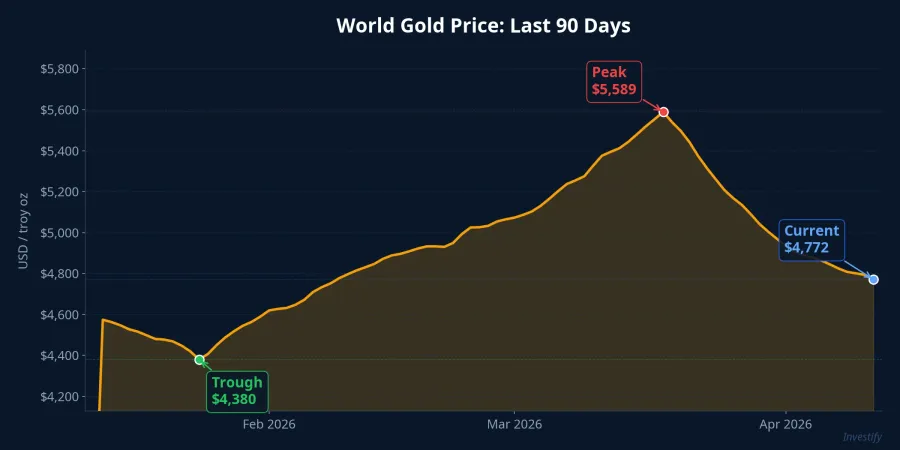

On January 28, 2026, world gold prices hit 5,589 USD/oz, crossing the 5,000 USD threshold for the first time ever.CBS News Just two months later, gold dropped sharply to 4,380 USD/oz on March 26, a decline of approximately 22% from the peak. The striking part: this crash occurred right in the middle of the US–Iran conflict at the Strait of Hormuz, a scenario where most people assume gold should surge.

The simple truth is that gold is not always a "safe haven" in every crisis. This article explains the three mechanisms behind this paradox, helping you understand gold's actual role in an investment portfolio.

Mechanism 1: "Buy the Rumor, Sell the News"

This is a classic effect in commodity markets, and the recent volatility illustrates it perfectly.

Gold surged 29% in January 2026 alone, from 4,332 USD/oz at the start of the year to the 5,589 USD/oz peak, largely driven by expectations of escalating geopolitical risk. In other words, investors "bought ahead" of the war risk, pushing gold to price in a worst-case scenario before the event even happened.

When the Hormuz conflict officially erupted in late February, gold had already accumulated excessive negative expectations. The peak was set before the war broke out. Specifically, on March 2 gold was still at 5,322 USD/oz, but just one day later it dropped 4.4% to 5,088 USD/oz. Investors took profits when "the rumor became the news."

If you've ever heard "buy the rumor, sell the news" in equity markets, this is the commodity version. The lesson: when a risk scenario is widely anticipated by the market, prices have already priced it in, and the actual event often becomes a profit-taking trigger rather than a buying opportunity.

Mechanism 2: The Liquidity Shock — When Gold Is Sold to Save Portfolios

This is the most important mechanism, yet it is rarely explained clearly for retail investors.

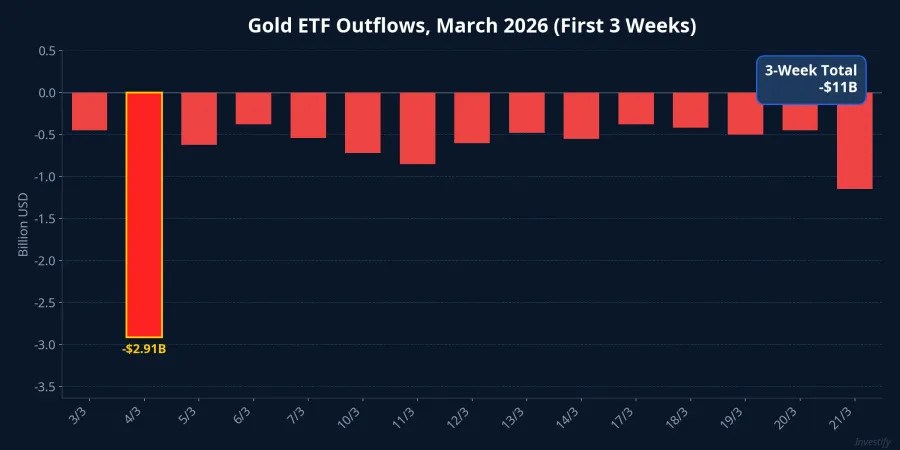

When oil prices surged after the Hormuz blockade, global equity markets plunged. South Korea's KOSPI index dropped 12% in a single session, triggering massive margin calls on leveraged hedge funds.MarketMinute When cash was urgently needed, funds were forced to sell their most liquid assets, and gold was the first target.

The result: SPDR Gold Trust (GLD), the world's largest gold ETF, recorded net outflows of 2.91 billion USD in a single day (March 4, 2026), the highest since 2016.MarketMinute In total, 11 billion USD was pulled from gold ETFs in just the first three weeks of March 2026.MarketMinute

On March 19, the gold market experienced a "flash crash" when 98% of order book depth vanished within 30 minutes, pushing the price to an intraday floor of 4,557 USD/oz.MarketMinute

This mechanism creates a negative feedback loop: falling prices trigger more margin calls, forcing further selling, which pushes prices down even more. Simply put, gold is too liquid — so when the market urgently needs cash, it gets sold first. That is exactly why gold "fails" as a short-term safe haven.

Mechanism 3: Opportunity Cost — Gold Loses to US Treasuries

The deepest layer of explanation lies in monetary policy. Fed Chair Kevin Warsh declared that interest rates would remain at 3.5–3.75% for the foreseeable future, extinguishing any expectations of monetary easing in 2026.Seeking Alpha

When real interest rates remain elevated, the opportunity cost of holding gold — an asset that generates no yield — becomes expensive. Think of it this way: if short-term US Treasuries offer attractive yields, capital flows toward bonds instead of "sitting idle" in gold. The stronger USD that results from capital flowing into US assets puts additional downward pressure on gold (since gold is priced in USD, a stronger dollar makes gold more expensive for international buyers, reducing demand).

The market is maturing in how it views gold: war does not automatically equal rising gold prices. Gold only rises sustainably when capital has no better alternative — and with US Treasury yields at current levels, that alternative exists.

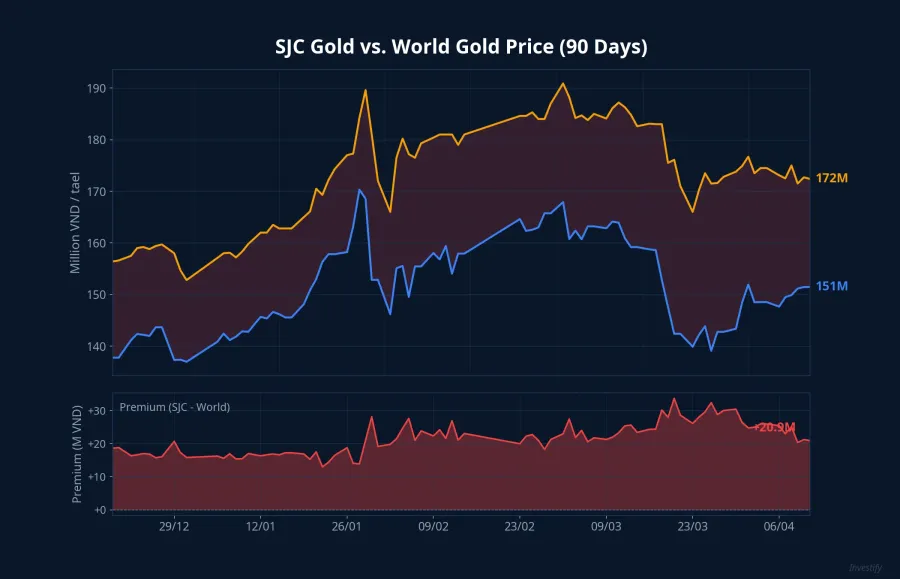

The Vietnam Perspective: SJC Premium of 21 Million VND Is a Double Risk

In Vietnam, gold investors face an additional layer of risk: the gap between the SJC price and the converted world price.

SJC gold bars peaked at 190.9 million VND/tael on March 2, then dropped sharply to 166.0 million VND/tael on March 23, losing nearly 25 million VND/tael (approximately 13%) in just three weeks. Gold rings (99.99% purity) also declined similarly, from a peak of 187.9 million to 164.3 million (approximately 12.6%) over the same period.

As of April 11, SJC gold bars recovered to 172.4 million VND/tael, while gold rings stood at 170.6 million. The gap between bars and rings narrowed to just 1.8 million VND, reflecting the early impact of Decree 232/2025.

With international gold at 4,772 USD/oz and an exchange rate of 26,321 VND/USD, the converted gold price per tael is approximately 151.5 million VND. Meanwhile, SJC sells at 172.4 million, a premium of approximately 21 million VND/tael, equivalent to nearly 14%.Thanh Niên

What does this mean for your wallet? If you buy SJC gold today at 172.4 million, the world gold price needs to rise an additional 14% just for you to break even at international prices. If the premium narrows (due to Decree 232 expanding the legal supply of gold bars), you face a double loss: both the risk of falling world gold prices and the risk of a shrinking domestic premium.

Decree 232/2025: long-term hope, but results take time

Decree 232/2025/ND-CP, effective from October 10, 2025, officially dismantled the state monopoly on gold bar production that had been in place for 13 years since Decree 24/2012.Báo Chính phủ Under the new regulations, enterprises with capital of at least 1,000 billion VND and commercial banks with capital of at least 50,000 billion VND can be licensed to produce gold bars.Tạp san Luật sư Nội bộ

In theory, breaking the monopoly should increase the legal supply of gold bars, thereby narrowing the SJC premium toward the world price. However, as of April 2026 — nearly 6 months after the Decree took effect — the premium remains at approximately 21 million VND, indicating that the supply expansion process needs more time to take effect.

Three Lessons for Individual Investors

1. Gold is not a perfect "insurance" in every scenario. During liquidity crises, gold can decline alongside equities because it gets sold to meet margin calls. Gold serves its safe-haven role better during prolonged crises with declining interest rates — not during short-term shocks when the market needs cash.

2. The SJC premium is a hidden cost that must be factored into your purchase price. A premium of approximately 21 million VND/tael (14% above the world price) is a risk unique to Vietnamese investors. If buying gold as a long-term store of value, factor this premium into your entry cost rather than looking only at world gold price movements.

3. Portfolio diversification is essential. The March 2026 event shows that no single asset class performs well under all market conditions. In an environment of positive real interest rates and high volatility, fixed-income instruments (government bonds, deposits, fixed-income products) play a portfolio stabilization role that gold cannot replace.

Outlook

Gold has recovered 9% from its trough of 4,380 USD/oz (March 26) to 4,772 USD/oz (April 10), showing that demand for buying on deep corrections remains strong. Two factors will determine the next move:

- If the Fed shifts to easing: gold could return to the 5,000 USD/oz range as opportunity costs decline.

- If the Hormuz conflict is resolved and the Fed maintains high rates: gold may range between 4,500–4,800 USD/oz, and the SJC premium could narrow if Decree 232 takes effect.

The March 2026 episode is an important reminder: understanding the mechanisms behind gold market movements matters far more than trusting simplistic rules like "war equals rising gold." Key factors to watch in the coming weeks: the Fed's next policy signals and the progress of Hormuz negotiations.