Here's what the reports don't make clear: Vietnam's bond market just surpassed the 3.8 quadrillion VND mark, but most of that growth comes from issuances that retail investors cannot access. Meanwhile, the maturity pressure of 141 trillion VND in real estate bonds is concentrating right in Q2/2026, creating a serious liquidity test for many enterprises.

The real risk lies in the fact that impressive growth figures obscure deep fragmentation within the market. Let's peel back each layer to understand who benefits, who faces pressure, and where retail investors stand in this picture.

3.84 Quadrillion VND: Government Bonds Lead, Corporate Bonds Follow

According to Vietnam Financial Times, Vietnam's bond market surpassed the 3.8 quadrillion VND mark by the end of Q1/2026.Vietnam Financial Times Government bonds accounted for 2.67 quadrillion VND, equivalent to 20.8% of GDP. Corporate bonds reached approximately 1.17 quadrillion VND, representing 9.1% of GDP.

Combined, the bond market now equals nearly 30% of GDP. That sounds impressive, but what's worth noting is that government bonds still make up nearly 70% of total market size. Corporate bonds account for less than a third, and most of those are not available to retail investors.

In Q1/2026 alone, the State Treasury raised 80,101 billion VND in government bonds, equivalent to 16% of the full-year plan of 500,000 billion VND.Vietnam Financial Times Government bond yields for 5 to 10-year maturities rose slightly on both primary and secondary markets. When the government has to pay higher yields to raise capital, interest rates across the entire market get pulled upward.

Corporate Bonds Issue 30,600 Billion: Real Estate Takes Over Half

The corporate bond market in Q1/2026 recorded new issuances worth 30,600 billion VND, up 22% year-on-year. The real estate sector dominated with 53% of total issuance value.Journal of Economics & Finance

But who is issuing, and at what price? The fragmentation is clear from the largest deals in March 2026. Marina Center issued 10,195 billion VND in private placement bonds with a 10-year term, featuring a rare "step-up" interest structure: starting at just 4%/year then gradually increasing before switching to floating rates. The purpose was to acquire all shares of Capitaland Central Tower at the Saigon Ba Son complex.VietnamBiz HDBank publicly issued over 4,600 billion VND, among the most active bank issuers in the quarter.Vietstock

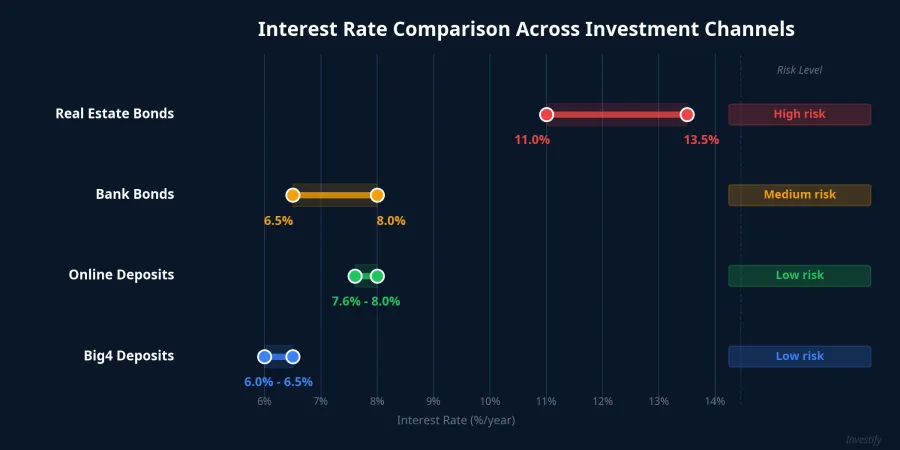

On the other end, Phat Dat issued approximately 5,600 billion VND at interest rates up to 11%/year. Banks issued around 6.5 to 8%/year, while real estate companies had to offer 11% to 13.5%/year, the highest level in nearly 2 years.Dan Viet This interest rate gap isn't an "attractive offer" for investors; it directly reflects the credit risk that the market prices into the real estate sector.

Notably, Techcombank plans to buy back 6 bond lots worth a total of 13,500 billion VND in April 2026 to restructure its capital as deposit rates trend upward.DNSE

Savings Rates Exceed 8%: Spread Narrows, Risk Emerges

Deposit rates at banks in April 2026 show a clear upward trend. The Big4 banks raised their 6 to 36-month deposit rates to 6 to 6.5%/year. Many smaller banks pushed rates significantly higher: some foreign banks listed up to 7.6 to 8%/year for online deposits.VietnamNet PVcomBank even listed 10%/year for deposits starting from 2,000 billion VND.VietnamNet

What does this mean for the bond market? When savings rates already exceed 7 to 8%/year, the spread between bank bonds (6.5 to 8%) and deposits is virtually zero. Investors buying bank bonds are no longer meaningfully compensated for the lower liquidity risk compared to deposits.

Meanwhile, real estate bonds still offer 11 to 13.5%/year, creating a spread of about 3 to 6 percentage points above deposits. But that spread isn't a "reward" for smart investors. It's the market's price for real credit risk: the risk that companies cannot repay on time. The 2022 to 2023 period showed clearly that high spreads don't guarantee safety.

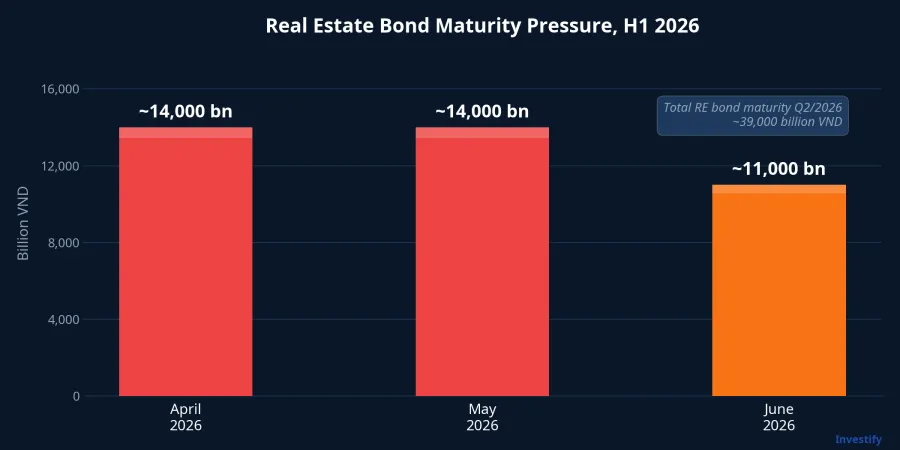

141 Trillion VND Maturing: Q2 Stress Test for Real Estate

Total real estate corporate bonds maturing in 2026 are estimated at approximately 141 trillion VND, up 81% from 2025.CafeF The pressure concentrates in the first half, with principal repayment obligations for the non-bank sector in the first 6 months expected at 76,100 billion VND, of which 68.6% belongs to the real estate sector.Journal of Economics & Finance

The peak is Q2/2026, with each month seeing approximately 11,000 to 14,000 billion VND coming due. Companies facing the greatest pressure include Van Truong Phat (10,000 billion), Hai Dang (6,650 billion), Truong Minh (5,500 billion), and R&H Group at approximately 5,000 billion.CafeLand

The positive news: the bond default rate in Q1/2026 dropped to near 0%, compared to 0.2% in the same period last year.VietData However, with maturity pressure mounting in Q2, this figure could change rapidly. This is the period investors need to monitor most closely.

New Decree in April 2026: The Rules Are About to Change

The Ministry of Finance is finalizing a decree amending private corporate bond issuance regulations, expected to be submitted to the Government in April 2026.VnEconomy The new decree will replace all three existing decrees (Decree 153/2020, Decree 65/2022, Decree 08/2023), focusing on expanding issuance conditions, enhancing transparency, developing bond investment fund systems, and applying credit ratings to direct capital toward high-quality bonds.

If the decree is issued on schedule, it will be a significant catalyst for the corporate bond market in the second half of 2026. However, retail investors should note that regulatory reforms typically take time to show results; expecting immediate change is unrealistic.

Where Do Retail Investors Stand?

The real risk is that many investors look at the 3.8 quadrillion VND figure and assume this is an open playing field for everyone. It is not.

First, approximately 90% of corporate bonds are still issued through private placement, reserved for professional investors (investment portfolio of at least 2 billion VND maintained for 180 consecutive days, valid for 3 months). Most of the corporate bond market remains beyond the reach of retail investors.

Second, bonds are not a single asset class. Government bonds and bank bonds carry low risk but yields only match deposit rates. Real estate bonds offer higher interest but come with real maturity and credit risk. There is no "high return, low risk" in this market.

Third, with savings rates already exceeding 7 to 8%/year, retail investors can access fixed income through multiple channels: bank deposits (deposit insurance up to 125 million VND), publicly issued bonds, or fixed-income investment products packaged by financial platforms. Each channel has its own characteristics regarding liquidity, risk, and capital protection.

The 3.8 quadrillion VND bond market is growing, but growth does not equal safety. With 141 trillion in real estate bonds maturing in 2026 and the spread between bank bonds and deposits virtually eliminated, this is the time investors need to be more clear-headed than ever: understand what you're buying, who issued it, and what risks lurk beneath those impressive growth figures.