The big picture reveals a rare paradox: in the same week, the US stock market posted its strongest rally in five months while American consumers hit the most pessimistic reading in the entire history of the survey. Capital is flowing on expectations, but real life is moving in the opposite direction. When these two worlds drift this far apart, investors need to ask: which side will have to catch up to the other?

S&P 500 Surges on US-Iran Ceasefire

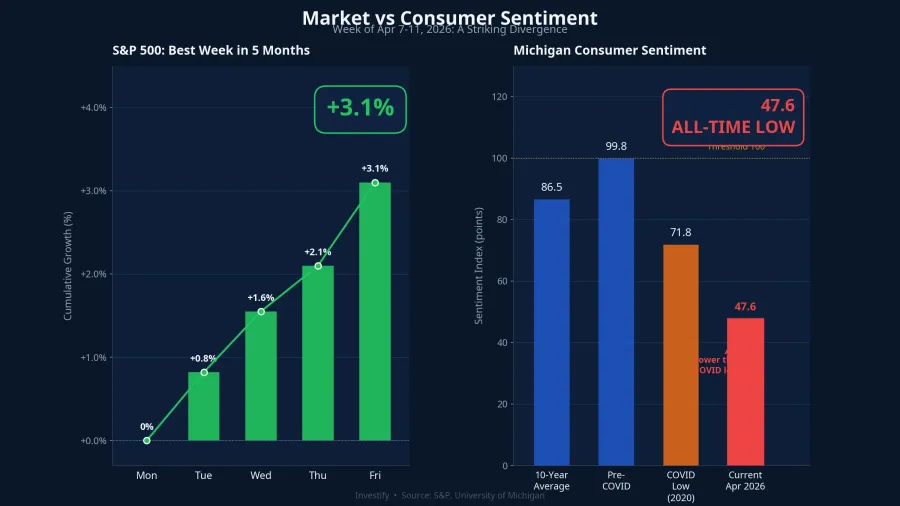

In the week ending April 11, 2026, the S&P 500 gained 3.1%, rising from 6,611 to 6,816 points, marking its best week since November 2025.CNBC On April 8 alone, the Dow Jones jumped 1,325 points in a single session, its strongest day in a year.CNBC

The primary catalyst was the US-Iran humanitarian ceasefire agreement, confirmed by the US State Department on April 10.MarketMinute The two-week deal, brokered through Oman and Qatar, aims to negotiate maritime security in the Strait of Hormuz and uranium enrichment issues.CNBC The immediate reaction: WTI crude plunged 16.4% to $94.41 per barrel in a single session, driving expectations of cooling inflation and giving the Fed more room to cut rates.

In other words, Wall Street is trading on the optimistic scenario: a sustained ceasefire, lower oil prices, easing inflation, and corporate earnings recovery over the next 6-12 months.

Consumer Sentiment Hits All-Time Low: 47.6 Points

But on the same day, April 10, the University of Michigan released its preliminary April consumer sentiment index at 47.6 points, the lowest in the survey's entire history, breaking the previous floor of 50 set during Biden-era peak inflation.CNBC Sentiment fell 11% in a single month and was 9% lower year-over-year.

Notably, 98% of interviews were conducted before the April 7 ceasefire announcement. American consumers were reflecting the reality they are living in, not the expectations Wall Street is trading on.

Specifically, one-year inflation expectations surged from 3.8% to 4.8%, the largest one-month jump since April 2025.Benzinga Long-term inflation expectations (5-10 years) also rose from 3.2% to 3.4%, the highest since November 2025. The decline was universal: every age group, income bracket, and political affiliation grew more pessimistic.

March CPI: Inflation Triples

The root cause lies in people's wallets. US CPI for March 2026 rose 0.9% month-over-month, triple the 0.3% reading from February.CNBC Annual inflation reached 3.3%, driven by a 10.9% surge in energy costs. Gasoline alone jumped 21.2% in a single month, a record increase, accounting for nearly three-quarters of the total CPI rise.

For ordinary Americans, these aren't numbers on a chart. They are the gas bill, the electricity bill, and a heavier grocery cart every week. Wall Street sees "CPI will fall once oil cools down"; Main Street feels "this month is more expensive than last month."

What Does History Say When These Two Worlds Diverge?

Divergence between consumer sentiment and the stock market is not uncommon, but the current magnitude is extreme. According to Morningstar's analysis, when consumer sentiment hits deep lows, stocks tend to rise over the following 12 months, because economic damage has already occurred and the market has "moved ahead."Morningstar Low sentiment, by this logic, serves as a contrarian indicator.

However, when the divergence is prolonged and reaches historic levels like today, two scenarios emerge. The first is a rapid correction: markets drop 20-30% as consumption actually slows and corporate earnings take a hit. The second is extended sideways trading: stocks drift for years, waiting for wages to catch up with asset prices. The last time a similar divergence occurred was in the 1920s, before the Great Depression. The modern economic context is vastly different, but the warning signal remains worth considering.

Vietnam: A Smaller Version of the Paradox

Vietnamese investors are experiencing a scaled-down version of this paradox, with capital flows reflecting both sides simultaneously.

On the market side, the VN-Index rose 4.32% during the week of April 7-11, 2026, from 1,677.54 to 1,750.00 points. The April 8 session alone surged 4.71%, the strongest in months, fueled by the global ceasefire effect and expectations of FTSE Russell upgrading Vietnam. However, domestic capital drove the rally while foreign investors continued net selling approximately VND 3,000 billion during the week. The market rose sharply, but "smart money" was pulling out.

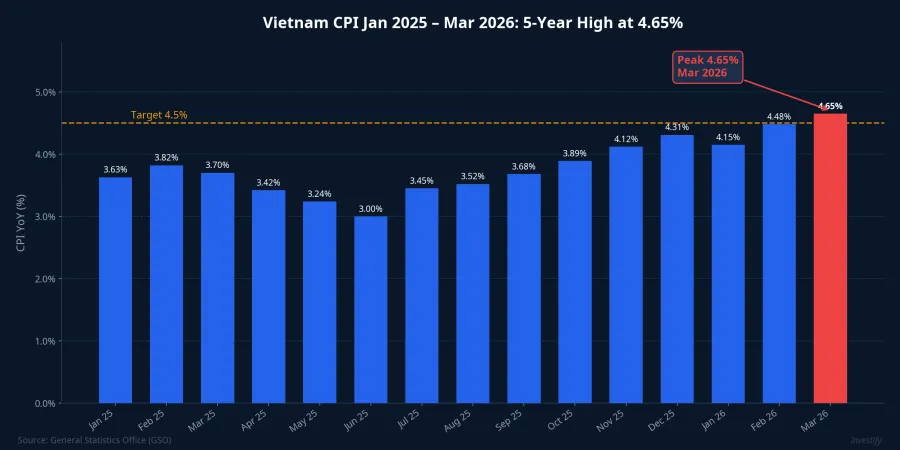

On the real-life side, Vietnam's March 2026 CPI rose 4.65% year-over-year, a 5-year high.CafeF Transportation costs surged 12.85%, contributing 1.28 percentage points to headline CPI.Báo Văn Hóa Vietnamese consumers feel the pressure clearly at gas pumps and supermarket checkouts.

A thought-provoking comparison: the VN-Index gained 4.32% in a week, but March CPI stood at 4.65%. Inflation is "eroding" investors' real returns if their portfolios don't grow fast enough. This is the trap many overlook: green brokerage accounts, but declining real purchasing power.

Lessons for Investors: See Both Pictures

The Main Street vs Wall Street paradox doesn't mean either side is completely wrong. Both are reflecting different parts of reality. Wall Street reflects expectations: a successful ceasefire will pull oil prices down, ease inflation, allow the Fed to cut rates, and restore corporate earnings. This logic holds, but only if the ceasefire truly lasts. Main Street reflects the present: gasoline up 21.2%, heavier bills, depreciating assets. People don't trade on 6-month expectations; they live on this month's income.

The greatest risk is when the gap between these two worlds grows too wide and lasts too long. If the ceasefire collapses, if inflation doesn't cool as expected, if consumption actually contracts, Wall Street will have to "catch up" to Main Street, and the correction could be severe.

For Vietnamese investors, four key takeaways. First, don't chase momentum without checking fundamentals: a 4.32% weekly gain in the VN-Index is impressive, but foreign investors are net selling and CPI is at a 5-year peak. Second, monitor real consumer spending: if inflation stays elevated, declining purchasing power will hit corporate revenues, especially in retail, F&B, and consumer goods. Third, diversify your portfolio: in a high-inflation environment, fixed-income investments yielding 8-11% annually can serve as a reasonable defensive component alongside growth equities. Fourth, plan for a ceasefire collapse scenario: if it happens, oil prices will reverse course and the VN-Index could give back the entire week's gains.

Wall Street or Main Street, who is right? The answer likely depends on your time horizon. For long-term investors, the current divergence may present an opportunity. For those living paycheck to paycheck, this is real pressure. The big picture shows: the further these two worlds drift apart, the higher the risk of a sudden convergence.