Looking at the numbers, Vietnam's six largest corporations hold approximately VND 305 trillion in bank deposits, equivalent to over USD 12 billion. This figure is not surprising but reflects vastly different financial logic across industries: insurance holds cash for regulatory reserves, technology holds cash awaiting M&A, and retail holds cash due to inventory turnover cycles. The pressing question now is: with Vietcombank announcing deposit rate cuts from April 13, 2026, which strategy is sustainable and who faces the biggest impact?

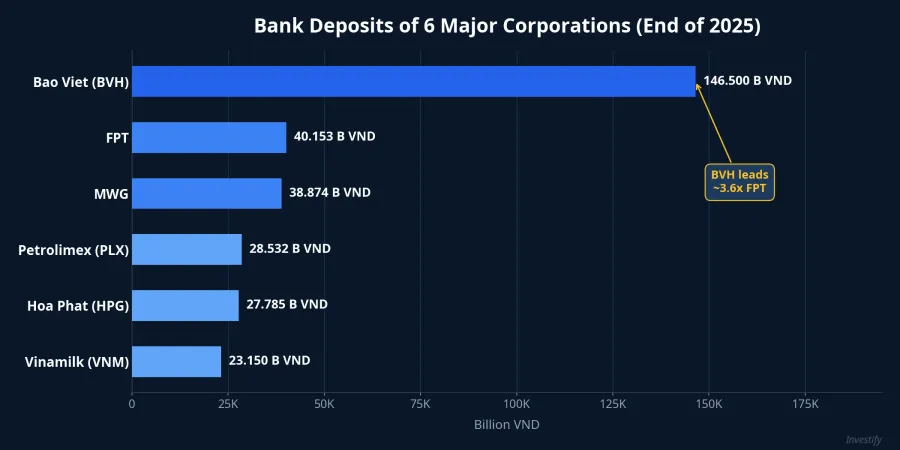

End-of-2025 deposit rankings

The 2025 financial reports of six corporations spanning six industries paint a diverse picture. Leading the pack is Bao Viet (BVH) with VND 146,500 billion, accounting for roughly 50% of total assets.Dan tri Following are FPT at approximately VND 40,153 billion (~46% of total assets), MWG at VND 38,874 billion (~46%), Petrolimex at VND 28,532 billion (~33%), Hoa Phat at VND 27,785 billion (~11%), and Vinamilk at VND 23,150 billion (~47%).Nguoi Quan SatDan tri

What stands out is not just the scale, but the deposit-to-asset ratio. Most corporations hold 33-50% of total assets in deposits. The sole exception is Hoa Phat: just 11%, as the steelmaker channels capital into production CAPEX rather than holding cash.

Bao Viet: when deposits become the business model

Bao Viet is the most striking case. With VND 146,500 billion in deposits, Vietnam's largest insurance group holds more deposits than the total assets of many small banks. Of this, short-term deposits reached approximately VND 119,624 billion (up 24% from end of 2024), while long-term deposits exceeded VND 26,951 billion.CafeF

Deposit interest alone generated VND 7,260 billion in 2025, up over 9% year-on-year, accounting for more than half of total financial revenue.CafeF The maximum rate BVH received was approximately 9% per annum for 3-12 month terms. This is essentially an interest rate arbitrage model, similar to how banks operate: collect insurance premiums, deposit them in banks, and earn the spread.

The insurance industry requires maintaining very large technical reserves. Premiums collected must be invested safely to ensure claims-paying ability, and bank deposits offer the highest liquidity with the lowest risk. However, precisely because of this dependence on deposit income, BVH is also the most vulnerable when rates reverse course.

FPT and MWG: liquidity buffers for two very different models

FPT maintained approximately VND 40,153 billion in deposits at end of 2025. In the first nine months, deposit interest reached VND 1,235 billion, equivalent to over VND 4 billion per day.Nguoi Quan Sat The technology giant is not holding cash for lack of investment ideas but is actively expanding its AI infrastructure and data centers, requiring significant capital for international M&A deals. Deposits serve as a "strategic reserve," ready to deploy when opportunities arise.

MWG deposited VND 38,874 billion, up nearly 14% from the start of the year. Financial revenue from deposits, lending, and bonds reached VND 2,912 billion, up 35% year-on-year.VietnamBiz The electronics retail sector demands very high liquidity: rapid inventory turnover and supplier payments (Apple, Samsung) that must be settled on time. MWG turns trade payables into an advantage: receive goods first, sell them, then pay suppliers, while the idle cash in between earns deposit interest.

Both cases demonstrate that deposits are a liquidity management tool, not an investment strategy. Deposit interest is a secondary benefit, not the primary objective.

Petrolimex and Hoa Phat: two industries, two capital equations

PLX maintained VND 28,532 billion in deposits at end of 2025, representing approximately 33% of total assets. Additionally, PLX invested roughly VND 3,300 billion in bonds.Tuoi Tre The petroleum industry requires substantial working capital for continuous import and distribution operations, especially amid oil price volatility.

HPG held approximately VND 27,785 billion in deposits, just 11% of total assets and the lowest ratio in the group. Deposit interest in 2025 reached VND 1,263 billion, with rates ranging from 4.1% to 8.5% per annum depending on tenor.StockBiz The key differentiator: HPG is the only corporation whose borrowings far exceed deposits, at VND 92,100 billion by end of 2025.StockBiz The steel industry demands massive CAPEX (Dung Quat Phase 2 has just become operational), so HPG accepts higher financial leverage, using borrowed capital for growth rather than holding defensive cash.

Vinamilk maintained VND 23,150 billion in deposits (~47% of total assets), with deposit interest reaching VND 1,371 billion.Dan tri With very stable operating cash flows (dairy is an essential good), Vinamilk's deposits serve as "liquidity insurance" against imported dairy ingredient price fluctuations.

Vietcombank cuts rates: who faces the biggest impact?

On April 9, 2026, the State Bank of Vietnam met with 46 commercial banks, requesting lower lending rates to support the economy. Immediately after, Vietcombank announced deposit rate cuts effective April 13, 2026: the 24-month tenor was reduced by 0.5 percentage points to 6% per annum, with all tenors capped at 6%.PLOStockBiz

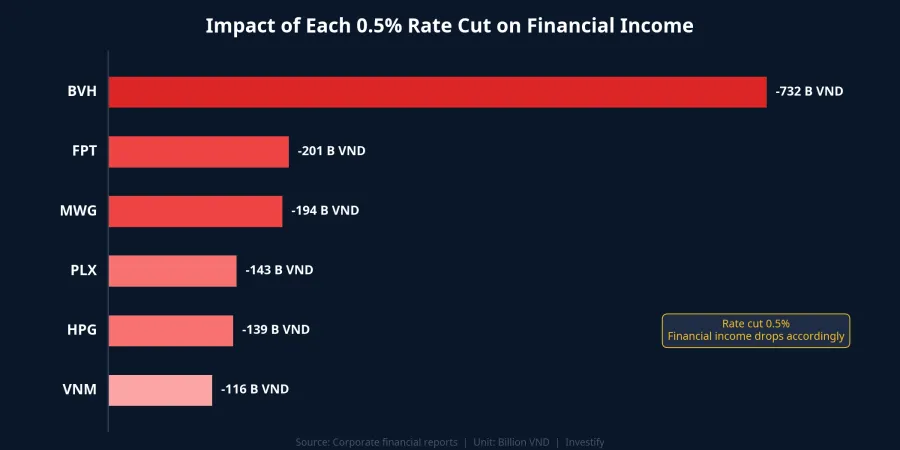

As other banks follow suit, deposit rates could decline by an additional 0.5-1 percentage points in coming months. Sensitivity analysis reveals sharply different impacts across the six corporations.

Bao Viet faces the largest absolute impact: each 0.5 percentage point rate cut translates to approximately VND 732 billion in lost financial income per year. FPT and MWG each lose roughly VND 200 billion, equivalent to 2.5-2.7% of net profit. PLX has a smaller deposit base but also lower net profit, making the relative impact significant as well.

HPG is the least sensitive, given its low deposit-to-asset ratio (11%) and profits driven primarily by steel production. Moreover, if lending rates decline in tandem, HPG with its VND 92,100 billion in outstanding borrowings would benefit from lower capital costs, creating a positive offset effect.

Three strategy groups, three sensitivity levels

Looking at the numbers, three distinct groups emerge:

Group 1: Deposits as a business model (BVH). Bao Viet has turned deposits into its primary revenue source, with VND 7,260 billion in deposit interest comprising over half of financial revenue. This is a disciplined model aligned with insurance industry characteristics, but also the most sensitive when rates reverse.

Group 2: Deposits as liquidity buffer (FPT, MWG, PLX). These three corporations hold high cash levels due to industry requirements, not market views. As rates decline, they may shift portions into bank bonds or longer-tenor certificates of deposit to maintain yields.

Group 3: Deposits as operational insurance (VNM, HPG). Vinamilk and Hoa Phat use cash as "insurance" against raw material volatility and industry cycles. Financial income represents a small share of total profit, making both relatively insensitive to rate movements.

Lessons from "smart money"

When major corporations hold 30-50% of assets in deposits, individual investors might wonder: "Smart money is being cautious; should I follow suit?" However, a clear distinction is necessary: corporations hold cash for operational needs and industry-specific reserves, not based on market outlook. Bao Viet must hold cash due to insurance regulations, FPT holds cash awaiting M&A, and MWG holds cash because of inventory turnover. None of them are "betting" on deposits as a pure investment strategy.

With deposit rates set to decline (VCB capped at 6% per annum), capital allocation strategies deserve reassessment: can traditional deposits still beat inflation, or should investors consider complementing them with higher-yielding alternatives?

Factors to watch

Three factors worth monitoring in the coming weeks. First, the rate-cut trajectory: if deposit rates fall by an additional 0.5-1%, BVH and MWG will see the clearest impact on financial income. Second, the shift toward bonds: corporations may redirect portions of deposits into bank bonds or government securities to maintain yield, and Q1/2026 financial statements will provide the first signals. Third, the offset effect at HPG: if lending rates decline in tandem, Hoa Phat with its VND 92,100 billion in outstanding debt stands to benefit significantly from lower capital costs, potentially exceeding the loss in financial income.