The big picture reveals a rare paradox: the two central banks most influential on Vietnam's market are pulling monetary policy in completely opposite directions. The US Federal Reserve faces surging inflation, forcing it to hold rates tight. The State Bank of Vietnam (SBV), on the other hand, is pressuring the entire banking system to cut rates at all costs. This divergence puts Vietnamese investors in an unprecedented dilemma.

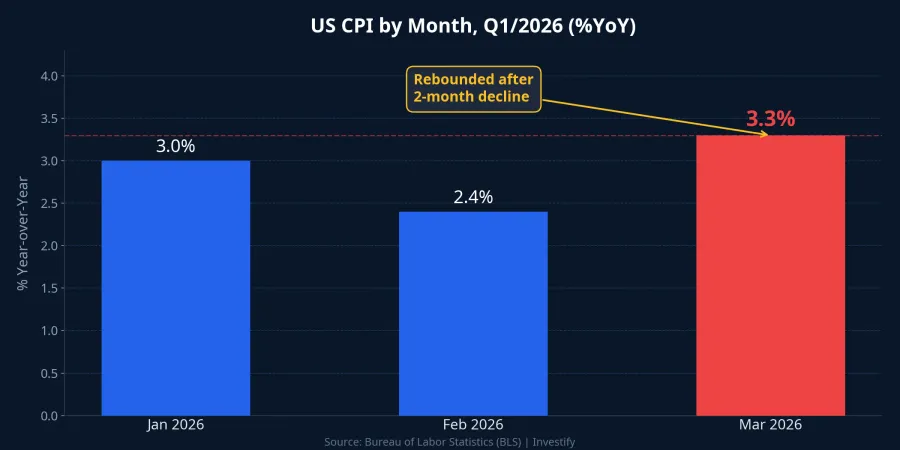

US CPI March: The 3.3% Shock from Energy Prices

Data from the Bureau of Labor Statistics (BLS) released on April 10 showed that the Consumer Price Index (CPI) for March 2026 rose 3.3% year-over-year, the highest level since May 2024.CNBC Just one month earlier, CPI was at 2.4%.CNBC On a monthly basis, CPI surged 0.9%, the largest increase since June 2022.CNBC

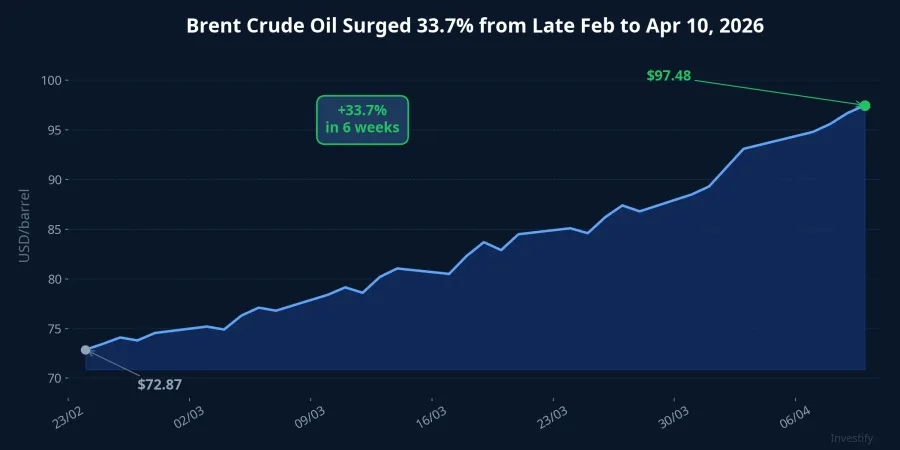

The primary driver was energy prices. The energy category surged 10.9% year-over-year, pushing US gasoline prices above $4 per gallon for the first time in over three years.CNBC The root cause is the conflict at the Strait of Hormuz, which controls approximately 20% of global crude oil shipments, driving Brent crude from $72.87 per barrel in late February to $97.48 on April 10 — a 33.7% increase in just six weeks.

The only positive note is that core CPI rose just 2.6% year-over-year, indicating that price pressures remain concentrated in energy and have not yet spread across the full consumer basket.CNBC However, the risk of cost pass-through from transportation to consumer prices is very real, and this is what markets fear most.

The Fed currently holds the federal funds rate at 3.50-3.75% since its March meeting.Fed According to the CME FedWatch tool, the market is pricing in approximately 95-98% probability that the Fed holds rates at its April meeting.CME FedWatch The probability of any rate cuts in 2026 has been virtually eliminated. Instead, the scenario of a rate hike — the first since 2023 — has reappeared on the market's radar.CNBC

SBV Pushes Rate Cuts: Growth at All Costs

While the Fed faces inflationary pressure forcing tighter policy, the SBV is moving in the completely opposite direction. Capital flows in Vietnam are following a different logic altogether.

On the afternoon of April 9, new SBV Governor Pham Duc An chaired his first meeting with leaders of 46 commercial banks, requesting consensus on cutting both deposit and lending rates.Tuổi Trẻ This was the strongest signal yet about policy priorities: supporting growth and reducing the interest burden on businesses.

Prior to the meeting, the SBV had injected VND 110 trillion through open market operations (OMO), helping interbank rates cool significantly.Znews Several major banks including Vietcombank, VPBank, and SeABank had already cut deposit and lending rates by 0.2-0.5 percentage points per their commitments at the meeting.VietnamNet

The context forcing the SBV's hand is clear: lending rates had been climbing as banks competed for deposits, pushing corporate borrowing costs higher at a time when the economy needs liquidity to sustain growth momentum. The last time the SBV organized a consensus meeting at this scale was in 2023, when the economy needed stimulus after COVID.

USD/VND Exchange Rate: Pressure Mounts as Rate Spreads Widen

When the Fed holds or even raises rates while the SBV pushes cuts, the interest rate spread between USD and VND widens. This creates direct pressure on the exchange rate.

The USD/VND rate on April 9 stood at 26,321 dong, up 1.06% from late February (26,045 dong). While the movement isn't dramatic yet, the upward trend has been clear and consistent over the past six weeks. Three main pressure channels are at play: the interest rate differential making USD-denominated assets relatively more attractive; FDI companies repatriating Q1 dividend profits in USD; and the tendency of import-export businesses to hold USD amid global uncertainty.

The SBV maintains sufficient foreign exchange reserves to intervene when needed, but if the Fed actually raises rates in the second half of the year, exchange rate pressure will intensify significantly and narrow the room for domestic easing.

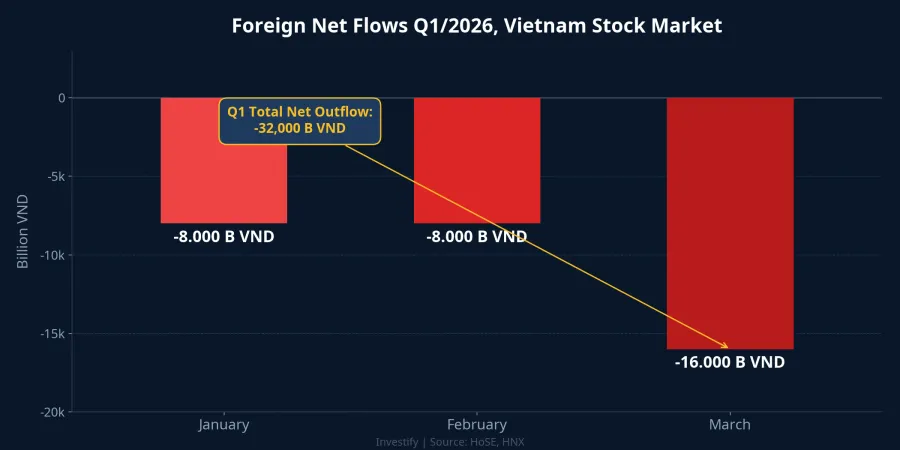

Record Foreign Selling Despite FTSE Upgrade

The biggest paradox right now: FTSE Russell has just confirmed Vietnam's upgrade to Secondary Emerging Market status effective September 21, 2026, yet foreign capital continues to flow out aggressively.CNBC

Foreign investors net sold over VND 32 trillion in Q1/2026, exceeding the VND 25.9 trillion in the same period of 2025.Người Quan Sát In March alone, net selling reached over VND 16 trillion across 18 out of 22 trading sessions.Vietstock The most heavily sold tickers included VIC (nearly VND 4.9 trillion), FPT (nearly VND 2.6 trillion), and STB (over VND 2.5 trillion).Người Quan Sát

The reason for foreign selling despite the confirmed upgrade: a strengthening USD makes emerging market assets relatively less attractive compared to US bonds. When USD interest rates are high, international capital tends to retreat to safer assets. The medium-term outlook remains positive, with FTSE estimating approximately $6 billion from passive funds flowing in when the upgrade takes effect, with long-term potential reaching $25 billion by 2030.Vietnam Briefing But the actual timing of disbursement depends heavily on USD interest rate levels: if the Fed maintains or raises rates, FTSE-related capital flows could arrive later than expected.

Brent Oil: The Variable That Determines Every Scenario

Capital flows are shifting according to oil prices, and this is the key variable. Brent crude rose from $72.87 per barrel in late February to $97.48 on April 10 — a 33.7% surge in six weeks — driven by the Strait of Hormuz conflict.

If oil prices continue to hold above $90, US inflation will struggle to decline, the Fed will have to hold or raise rates, the USD will remain strong, and pressure on VND and foreign capital flows will persist. Conversely, if Hormuz tensions ease and oil drops back below $80, the entire picture reverses: the Fed could return to its rate-cutting trajectory, VND stabilizes, and FTSE capital flows arrive on schedule.

VN-Index Recovers but Risks Remain

The VN-Index closed at 1,750 points on April 10, up 13.32 points (+0.77%). The index has staged an impressive recovery from its 1,591-point low on March 23, rising nearly 10% in under three weeks. However, the VN-Index is still down 5.2% from its 1,846-point level at the start of March. Trading volume on April 10 reached nearly 962 million shares, an average level compared to the past week.

The Dow Jones also posted a recovery, reaching 48,185 points on April 10, up 3.6% in one week, indicating improving global market sentiment after the initial shock.

Where Should Investors Stand Between Two Currents?

Both the Fed and the SBV have legitimate reasons for their decisions. The Fed prioritizes inflation control; losing the inflation expectations anchor would be far more costly. The SBV prioritizes growth; Vietnam's economy needs affordable credit to sustain development. But this divergence creates both opportunities and risks across asset classes:

- Export stocks benefit from a stronger USD, as profit margins improve when revenue converts to more VND. Seafood, textiles, and wood products are prime examples.

- Banking stocks enjoy short-term benefits from credit expansion as the SBV pushes rate cuts, but non-performing loan risks will rise if businesses borrow inefficiently.

- VN30 stocks are positioned to attract FTSE capital flows when the upgrade takes effect in September, though disbursement timing could be delayed if the USD continues strengthening.

- Defensive assets such as government bonds, certificates of deposit, or fixed-income products are reasonable choices for the portion of capital seeking stability amid volatility.

The most important thing is not choosing "which side is right" but managing exchange rate risk. With two policy currents flowing in opposite directions, a balanced portfolio combining export stocks benefiting from a strong USD, large banks with solid capital bases, and a defensive asset allocation is the most appropriate strategy for navigating this period of uncertainty.