While Vietnamese media this past week revolved around two big stories — Hormuz tensions pushing Brent crude back near $100 a barrel, and FTSE upgrade euphoria sending the VN-Index up a record 79 points on April 8 — in another corner of the global capital map, $15.3 billion quietly flowed into a place almost no Vietnamese retail investor was watching: Japanese Government Bonds (JGBs).

This was not instinctive "flight to safety" capital. The big picture shows a global repricing of risk, and it tells a very different story from what we have been reading every morning. When the world's largest funds simultaneously change direction within a single week, it is often a leading indicator of bigger moves in emerging markets like Vietnam.

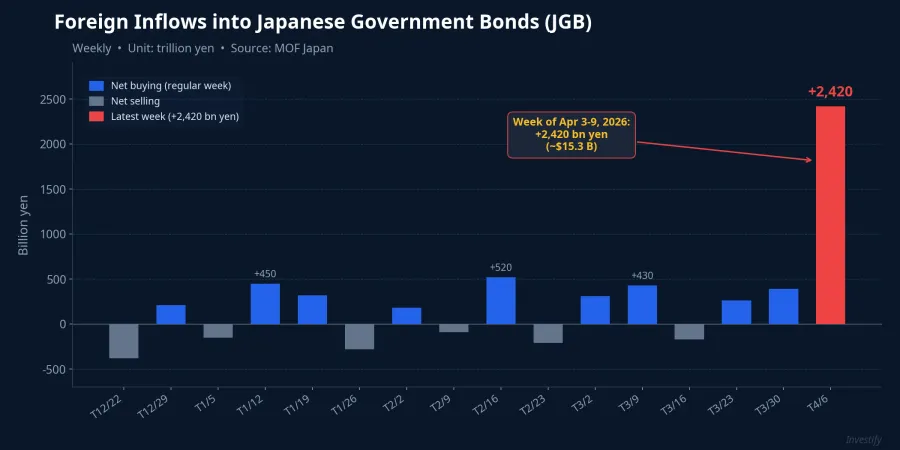

$15 Billion: The Largest Weekly Net Buying in a Year

According to preliminary data from Japan's Ministry of Finance released in early April 2026, global funds net-bought roughly 2,420 billion yen of Japanese government bonds — about $15.3 billion — during the week of April 3-9, the largest amount since April 2025.Japan Times What stands out is that just one week earlier, these same funds had sold a similar amount — meaning capital flows reversed entirely within seven trading days.

This reversal coincided with the week of escalating Hormuz tensions. Brent crude closed on April 9 at $98.08 per barrel, up 3.51% in a single session, after diving 13.29% the prior session when markets had priced in a possible ceasefire. But instead of piling into gold or US Treasuries as the classic playbook would suggest, big money found its way to Tokyo. The last time a reversal of this magnitude happened in such a short window was April 2025, when markets were repricing global rate expectations.

Why JGBs, Not Gold or US Treasuries

The answer comes down to one word: yield.

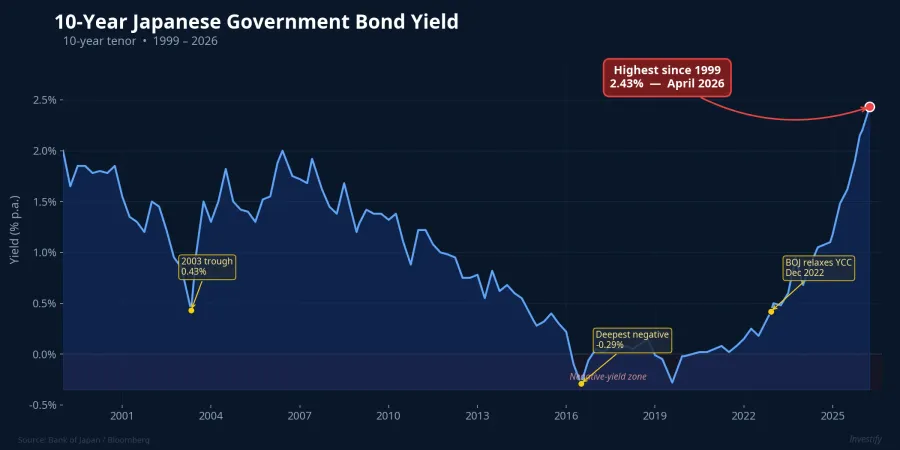

The yield on 10-year Japanese government bonds touched 2.43% in the first week of April 2026 — the highest since 1999, a 27-year peak. At the same time, 5-year JGBs hit a fresh record at 1.83%.Japan Times For an institutional investor accustomed to seeing the 10-year JGB hover around zero for an entire decade, this is a massive jump in real return.

More importantly, the US-Japan yield gap has narrowed sharply. While the 10-year US Treasury hovers in the 4.2-4.4% range, the 10-year JGB jumping to 2.43% has compressed the spread to just 180-200 basis points. For a USD investor with currency hedging, the hedged real return on JGBs has become significantly more competitive — for the first time in many years.

The result: capital chased JGBs not out of "war fear," but because pricing became compelling in a single week when other assets were swinging wildly. Gold remained anchored around $4,756 per ounce, but it was not the only destination for the money. The DXY dropped about 1% on the week to around 99, showing capital was not piling into the US dollar as it usually does during a geopolitical shock.

The BOJ's Hand: Quantitative Tightening Has Changed the Rules

To understand how JGB yields can spike to a 27-year high precisely when foreign capital is flooding in, you have to look at the Bank of Japan's policy.

Since 2024, the BOJ has entered a phase of quantitative tightening (QT): monthly bond purchases have been gradually reduced from 5.7 trillion yen to roughly 2.9 trillion yen in Q1 2026, with the focus on cutting intervention in the 10-25 year tenors.ABN AMRO In other words, the market's biggest buyer is stepping back, and the market is being forced to demand higher yields to absorb new supply.

In parallel, the BOJ has held its policy rate at a 30-year high, with signals it could hike further given inflationary pressure from oil prices and a weak yen. USD/JPY around 158.82 shows the yen remains soft, a factor that both worsens imported inflation and pushes fuel costs higher. The result is an environment where JGBs are no longer the "no-yield asset" they used to be. With a 10-year yield of 2.43%, JGBs have become a real fixed-income asset class — and global funds are treating them accordingly.

Global Yield Map: Where Does Vietnam Sit

What stands out is that JGBs ran counter to the classic "safe haven" reaction. Normally, when geopolitical tension flares, government bond yields fall because prices rise on safe-haven demand. This time it was the opposite: JGB yields rose, but foreign capital still poured in, because what attracted them was not "safety" but good pricing combined with real yield.

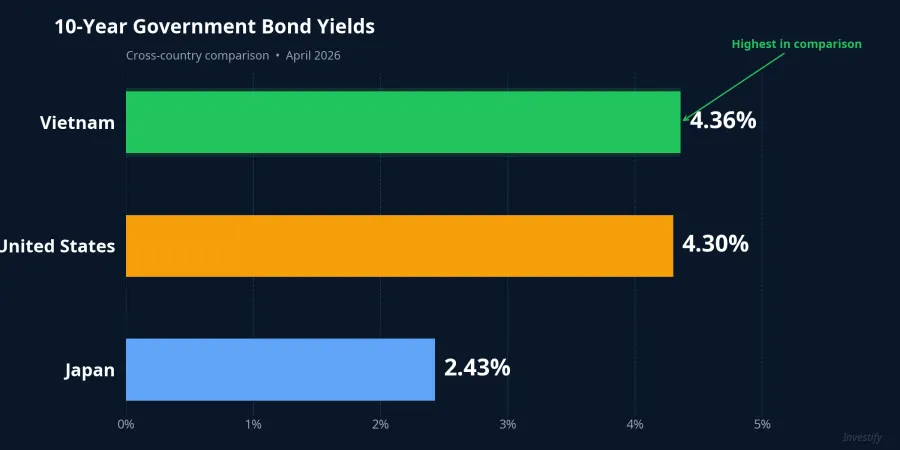

Side by side, three 10-year yields paint an interesting picture: Japan at 2.43%, the United States around 4.30%, and Vietnam at 4.36%. The yield on Vietnam's 10-year government bond stood at 4.36% on April 9, 2026, up roughly 120 basis points from a year earlier — the highest since March 2023.Trading Economics In other words, Vietnam's bond yield curve is also being repriced under the new rate cycle, just like JGBs but on a smaller and less-watched scale.

With 12-month deposit rates at major banks around 5-5.5%, and small/online banks at 7-8%, government bonds at 4.36% may look like they are "losing" to deposits at first glance. But the difference lies in three factors that depositors often overlook:

- Liquidity and tenor: government bonds can be sold on the secondary market without forfeiting all interest, unlike early-withdrawn deposits.

- Credit risk: Vietnamese government bonds carry a higher credit rating than the small commercial banks paying the highest deposit rates.

- Portfolio role: bonds are the defensive layer that reduces overall volatility when stocks correct — a role fixed-term deposits cannot fully replace.

Vietnamese retail investors can access government bonds through three main channels: retail distribution via commercial banks or on the HNX exchange at a face value of 1 million VND per bond; indirect exposure through open-end bond funds, the most suitable channel for newcomers given the low minimum capital and no need for valuation expertise; or fixed-income products via fintech platforms, which typically offer higher yields than bank deposits with flexible tenors.

The Takeaway: When Bonds Are the Lead, Not the Sidekick

The story of $15 billion flowing into JGBs is not meant to convince Vietnamese investors to "buy JGBs." That is impractical for most individuals, and not the main message anyway. The bigger lesson lies elsewhere: when yields become attractive enough, bonds are the lead actor in the smart money's portfolio, not a supporting role.

In Vietnam, that same week, the VN-Index went through a sharp ride: a record 79-point gain on April 8 to 1,756.55 points, then a 19.87-point drop to 1,736.68 on April 9. Two-digit moves on consecutive sessions show that the equity market is not the right channel for the "risk-intolerant" portion of any investor's portfolio, even when the VN-Index is riding upgrade euphoria.

In a 2026 backdrop where the VN-Index has set multiple historical highs, the Fed shows signs of holding rates higher for longer, and geopolitics remains full of unknowns, allocating part of a portfolio to fixed-income products — whether government bonds, bond funds, or fintech fixed-income — is not "missing out" but preparing for sessions when stocks no longer move in one direction.

Global institutional flows are telling us this in $15 billion a week. The remaining question for each retail investor: where is the stable portion of your portfolio sitting, and is it being paid fairly under the new yield cycle?