The big picture shows that deposit interest rates have risen too fast, forcing the State Bank of Vietnam (SBV) to intervene through administrative measures rather than conventional policy tools. On the afternoon of April 9, 2026, new Governor Pham Duc An chaired a meeting with leaders of 46 commercial banks, requesting a consensus commitment to reduce both deposit and lending rates.Thời báo Ngân hàng

This was no routine meeting. Mr. Pham Duc An had just officially taken office on April 8 for the 2026–2031 term.PLO Summoning 46 banks just one day after assuming the hot seat signals the urgency of the situation. Earlier, the Prime Minister had directed banks to cool down interest rates to support businesses and production.CafeBiz

Capital flows are shifting in a direction regulators did not want. So what pushed rates to the point where the SBV had to resort to "administrative force"?

The Hottest Rate Race in 5 Years

Before the meeting took place, the deposit market had witnessed the highest rate levels since 2022.

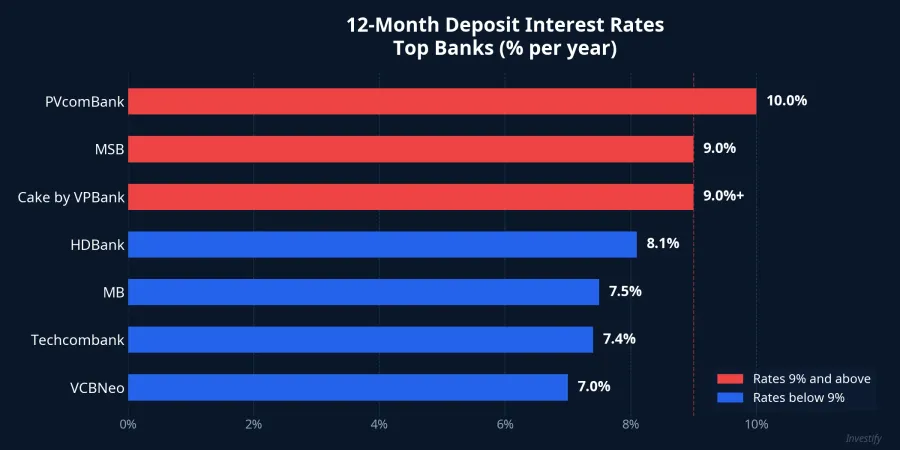

In the premium tier, PVcomBank offered 10% per year for 12–13 month terms, requiring a minimum balance of VND 2,000 billion. MSB applied 9% per year for new customers or auto-renewed deposits with amounts from VND 500 million. Cake by VPBank listed 7.7–7.9% per year plus promotional bonuses up to 1.1 percentage points, pushing the effective rate above 9%.24hMoney

The mainstream tier was equally competitive: HDBank listed 8.1% per year for 13-month terms, Techcombank 7.4% for 12 months, MB 7.5% for 24–60 months, and VCBNeo 7% for 6–60 months. Entering April, six banks had already raised deposit rates, including VietABank, NamABank, BaoVietBank, ACB, Techcombank, and VIB.24hMoney

Credit Growing Faster Than Deposits: The Fuse

According to a report by Monetary Policy Department Director Pham Chi Quang at the meeting, by the end of March 2026, system-wide credit had grown approximately 2.65%, reaching VND 19.08 quadrillion. The SBV set a 2026 credit growth target of 15%.Thời báo Ngân hàng

The core problem lies in the gap: credit is growing faster than deposits. When banks must ramp up lending to meet the 15% target but deposits cannot keep pace, this gap forces banks to raise rates to attract capital. The SBV acknowledged that some banks were competing in capital mobilization, pushing both deposit and lending rates higher.Thời báo Ngân hàng

When one bank raises rates to retain depositors, others must follow suit. This escalation spiral, where nobody wants to be the first to stop, creates a domino effect across the entire system.

CPI at 4.65% and the Impossible Triangle

Behind the interest rate race lies a fundamental contradiction in monetary policy management.

March 2026 CPI rose 4.65% year-on-year, the highest in five years.VnEconomy Month-on-month, March CPI increased 1.23%, mainly driven by fuel and construction material prices.Thời báo Ngân hàng Average Q1/2026 CPI rose 3.51% year-on-year.Tạp chí Công Thương

Meanwhile, the policy rate remains at 4.5%, lower than CPI itself. This means the real interest rate is negative when measured against the policy rate. For depositors, the mainstream 12-month savings rate of 7–7.5% per year still creates a positive inflation premium of about 2.5–3 percentage points; however, this cushion is shrinking rapidly as inflation accelerates.

The SBV faces an impossible triangle: keeping lending rates low to support businesses, controlling escalating inflation, and ensuring the banking system has sufficient liquidity with a 15% credit target. The April 9 meeting was an attempt to resolve this contradiction through "consensus commitments," an administrative solution rather than adjusting the policy rate.

Specific Commitments: "Cut" Without a Number

At the meeting, banks reached a high-level consensus to implement the government and SBV directive to reduce rates.Thời báo Ngân hàng Governor Pham Duc An emphasized the SBV would closely monitor rate developments, supervise rate disclosures on bank websites, stand ready to provide liquidity support, and intensify inspections with strict enforcement.

A notable signal: just before the meeting, VCBNeo proactively cut rates across all tenors. The 1–5 month term dropped 0.3 percentage points (from 4.75% to 4.45%), while the 6–60 month term fell 0.2 percentage points to 7% per year.24hMoney This is seen as the "opening shot" of a rate-cutting wave expected to spread next week.

However, the key caveat is that the meeting produced no specific numbers. There was no deposit rate ceiling, no mandatory reduction margin. The "consensus" commitment is more of an implicit agreement than a hard regulation, and actual implementation depends on each bank's seriousness.

Stock Market: Surge Then Pullback

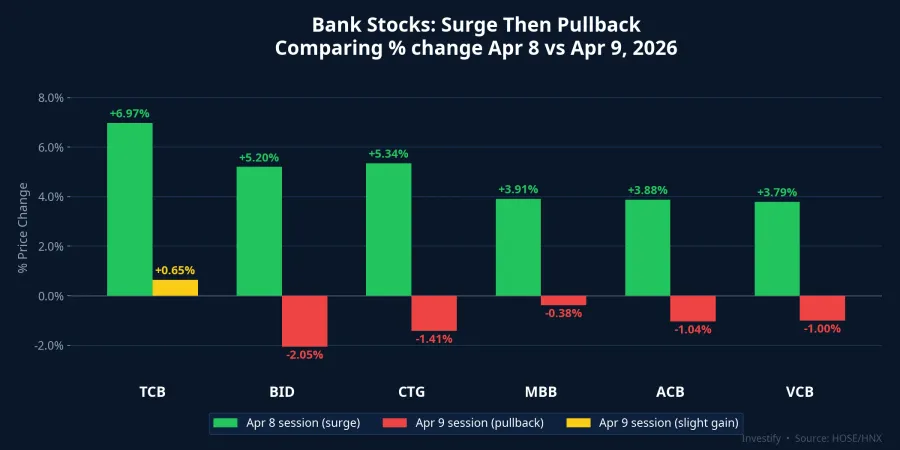

On April 9, VN-Index closed at 1,736.68 points, down 19.87 points or 1.13%. This was a correction after the April 8 explosion when the index surged 4.71% on the FTSE upgrade effect.

Bank stocks diverged sharply on April 9. TCB (Techcombank) was the only Big6 gainer at +0.65%, closing at VND 30,900. Meanwhile, BID (BIDV) fell the hardest at 2.05%, CTG (VietinBank) dropped 1.41%, ACB declined 1.04%, VCB (Vietcombank) lost 1.00%, and MBB (MBBank) slipped 0.38%.

Notably, in the previous session (April 8), banks were the pillars driving the market with impressive gains: TCB +6.97%, CTG +5.34%, BID +5.20%, MBB +3.91%, ACB +3.88%, VCB +3.79%. The April 9 session was more about short-term profit-taking than a negative reaction to the interest rate news.

What Should Investors Consider?

The High-Rate Savings Window May Close Any Time

If the rate-cut commitment is implemented, current 9–10% rates will not last. Those considering long-term deposits may want to "lock in" high rates before the floor drops. However, PVcomBank's 10% requires a VND 2,000 billion balance, and MSB's 9% needs at least VND 500 million. For everyday savers, the 7–7.5% range at Techcombank, MB, and OCB is more realistic.

Bank Stocks: A Double-Edged Sword

Lower deposit rates reduce banks' cost of funds, potentially improving net interest margins (NIM). This is a positive mid-term signal for bank stocks. However, if lending rates also fall proportionally, the NIM advantage is neutralized. Investors need to monitor the actual reduction gap between deposit and lending rates to assess the real impact.

Portfolio Diversification

With 4.65% inflation and potentially declining savings rates, investors should consider diversifying. Fixed-income products yielding 8–11% per year can provide balance, offering returns above standard bank deposits while being more stable than equities during volatile periods.

Outlook: Will Commitments Become Reality?

History shows that "consensus rate-cut" meetings do not always deliver results. In 2022–2023, the SBV repeatedly asked banks to reduce rates, but actual developments depended on market supply and demand for capital.

This time, two factors are different. First, new Governor Pham Duc An has staked his personal credibility on this commitment from day one. Second, the SBV pledged liquidity support; if banks lack capital, the SBV stands ready to inject funds through open market operations rather than letting banks attract deposits with high rates.

However, the biggest obstacle remains the 4.65% CPI and global energy prices. If inflation continues rising, forcing deposit rate cuts would deepen negative real rates, pushing money out of the banking system into alternative channels like gold or real estate. This is a risk the SBV must carefully weigh.

The bottom line: Investors should watch bank rate schedules over the next 1–2 weeks. If only VCBNeo and a few small banks cut while MSB and PVcomBank maintain their 9–10% levels, the meeting was merely ceremonial. Conversely, if the Big4 (Vietcombank, BIDV, VietinBank, Agribank) simultaneously cut 0.3–0.5 percentage points, that would confirm the interest rate peak has passed.