The big picture reveals a rare paradox: on the same night, two opposing forces emerged simultaneously. FTSE Russell officially confirmed Vietnam's upgrade to Secondary Emerging Market status, while the March FOMC minutes revealed that the Fed is leaning toward keeping rates higher for longer than expected. Capital flows are shifting in two opposite directions, and Vietnamese investors stand at a crossroads.

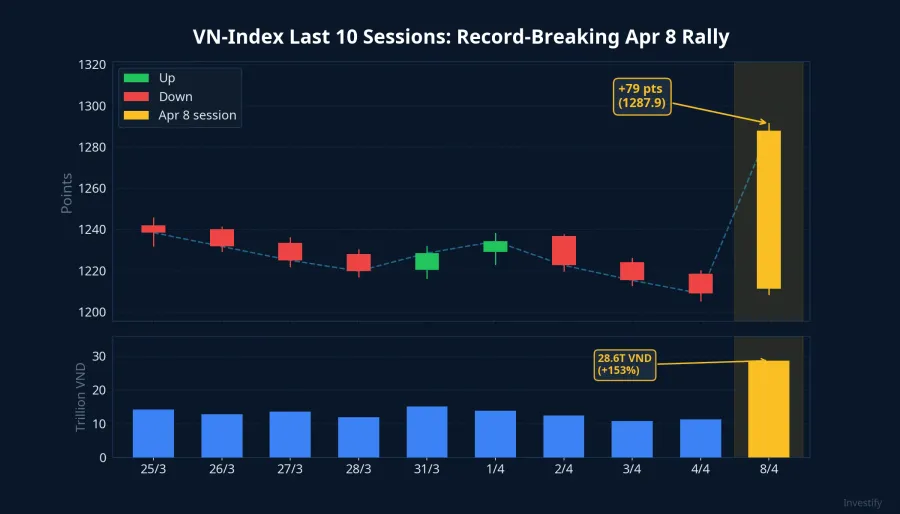

April 8 Session: A Historic Record for VN-Index

On April 8, 2026, VN-Index surged +79.01 points (+4.71%) to 1,756.55 points, marking the largest single-day point gain in the index's history.Dân Trí Trading volume spiked to nearly VND 35 trillion, more than 2.5 times the average of preceding sessions.DNSE Across the exchange, 297 stocks gained while only 25 declined — an overwhelming breadth showing capital spreading across the entire market, not just blue-chips.Dân Trí

That same night, Wall Street also surged on a 2-week US-Iran ceasefire deal. The Dow Jones rose 2.8% to 47,910 points, while Brent crude plummeted 16.9% to $90.76 per barrel.CNBC Global optimism combined with the upgrade news created a perfect storm for Vietnam's stock market.

FTSE Upgrade: A Four-Phase Roadmap

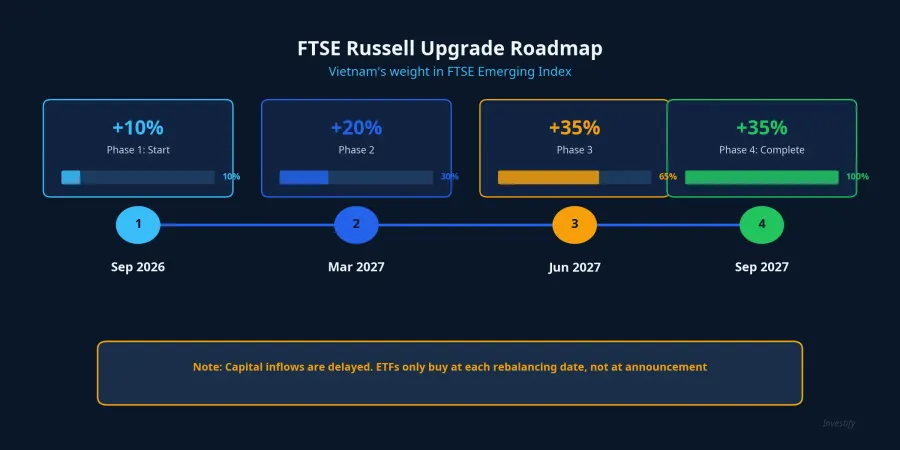

In the early hours of April 8 (Vietnam time), FTSE Russell officially confirmed Vietnam's placement on the upgrade path from Frontier Market to Secondary Emerging Market, effective September 21, 2026.The Investor After 8 years on the watchlist, the long-awaited moment has finally arrived.

According to FTSE Russell's official FAQ document, the transition will occur in four tranches: September 2026 adds 10% weight, March 2027 adds 20%, June 2027 adds 35%, and September 2027 completes the remaining 35%.FTSE Russell A preliminary list of 32 eligible Vietnamese stocks has been published, with the final list to be confirmed on August 21, 2026.The Investor

Vietnam is expected to represent approximately 0.35% of the FTSE Emerging All Cap index and 0.227% of the FTSE Emerging index.FTSE Russell Vietcap Securities estimates foreign capital inflows could reach $6–8 billion, with an optimistic scenario of up to $10 billion including both passive and active funds.The Investor

However, most mechanical (passive) capital will only be deployed when the upgrade takes effect — September 2026 at the earliest, stretching through September 2027. The period between now and then is primarily "seat-saving" by active funds, not a flood of real capital.

March FOMC Minutes: A Distinctly Hawkish Signal

On the same night Vietnam celebrated the FTSE upgrade, the Fed released the minutes from its March 17–18, 2026 FOMC meeting.Federal Reserve The content painted a far less optimistic picture than what markets had expected.

The Fed held rates steady at 3.50–3.75% for the second consecutive meeting, following three 25-basis-point cuts in late 2025. The most notable detail: 7 out of 19 FOMC members projected no rate cuts at all in 2026, a significant increase from the January minutes.Benzinga The median projection still points to one cut this year, but markets are only pricing in a single 25-basis-point cut, most likely in December.

Most officials emphasized that inflation risks remain tilted to the upside and that financial conditions have loosened too quickly. The March minutes were widely assessed as "distinctly more hawkish" than January, with the discussion shifting from "when to cut next" to "keeping rates higher for longer."

Two Opposing Forces: FTSE Pulls In, the Fed Pushes Out

Capital is shifting in two contradictory directions, and this is the core paradox that Vietnamese investors need to recognize.

The pull from FTSE: Estimated billions of dollars in passive capital will flow into Vietnam starting September 2026. Funds tracking the FTSE Emerging index are mechanically required to buy Vietnamese stocks once the upgrade takes effect. This is mechanical capital, independent of market sentiment — as long as a stock is in the index, these funds must hold it.

The push from the Fed: The high interest rate environment in the US (3.50–3.75%) keeps the dollar strong, and global capital tends to rotate back toward safe-haven assets. Foreign investors net sold over VND 32 trillion (approximately $1.2 billion) on Vietnamese exchanges in Q1/2026, continuing the net withdrawal trend that began in 2024.Người Quan Sát

The USD/VND exchange rate also reflects this pressure: from VND 26,102 at end of February to VND 26,334 on April 7, up about 0.9% in just over 5 weeks. Not yet alarming, but it signals that foreign capital is still flowing out.

Interest Rate Spread: The SBV's Dilemma

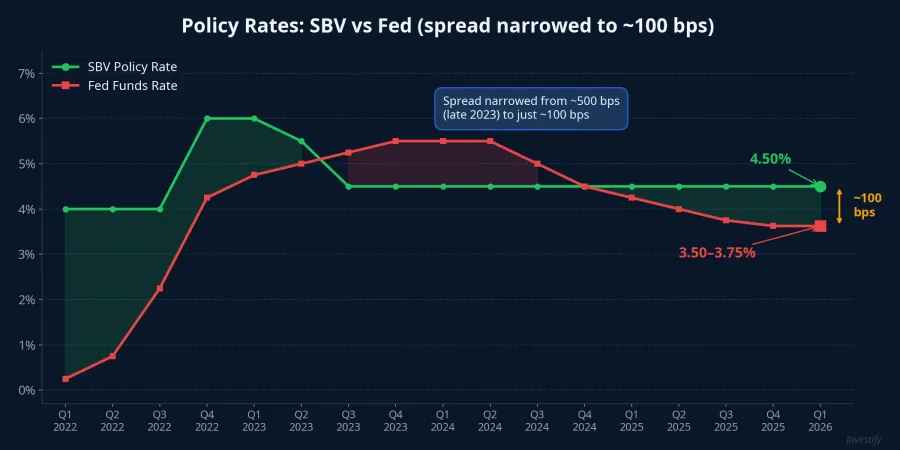

Domestically, March 2026 CPI reached 4.65%, the highest since January 2020. This makes it extremely difficult for the State Bank of Vietnam (SBV) to cut its policy rate (currently at 4.50%) to support the market, especially while the Fed maintains rates at 3.50–3.75%.

The Vietnam-US interest rate spread has narrowed to roughly 100 basis points, the tightest in years. If the Fed continues to hold rates high or even hikes, the SBV faces a dilemma: cutting rates to support growth would pressure the exchange rate, but holding steady means businesses continue bearing high capital costs. The last time the spread was this narrow was late 2023, when the Fed funds rate peaked at 5.5% and the SBV was forced to hold its rate unchanged for nearly two years.

Three Sobering Points After the Record Session

The April 8 session is now history. The more important question is whether the rally is sustainable, or merely a one-time reaction to news. Three factors investors should consider:

First, FTSE capital flows have a significant lag. The first phase (September 2026) only adds 10% weight. Real capital inflows are still 5–6 months away. Yesterday's session primarily reflected expectations, not actual capital deployment.

Second, the Fed minutes signal a long-term stance. 7 out of 19 members project no rate cuts in 2026. If the Fed keeps rates elevated through year-end, pressure on the exchange rate and foreign capital flows will persist, directly counterbalancing FTSE expectations.

Third, foreign investors are still withdrawing. VND 32 trillion in net selling during Q1/2026 shows the trend has not reversed, even though the upgrade has been confirmed. Mechanical capital from the upgrade needs time to offset these outflows.

Conclusion

The FTSE upgrade is extremely positive news for the medium and long term. Billions of dollars in mechanical capital will arrive — that is certain based on how index-tracking funds operate. But in the short term, the hawkish Fed minutes, elevated domestic CPI, and continued foreign net selling form three barriers that cannot be ignored. Post-record euphoria is entirely natural, but staying clear-headed about the difference between "expectations" and "actual capital flows" will help investors make better decisions in the sessions ahead.

Thanh Hà — Investify