The big picture reveals an unprecedented reversal: the greenback is losing its safe-haven appeal precisely when geopolitical tensions are escalating. Capital flows are shifting, and Vietnam happens to stand at the intersection of the two most powerful forces in global financial markets this April 2026.

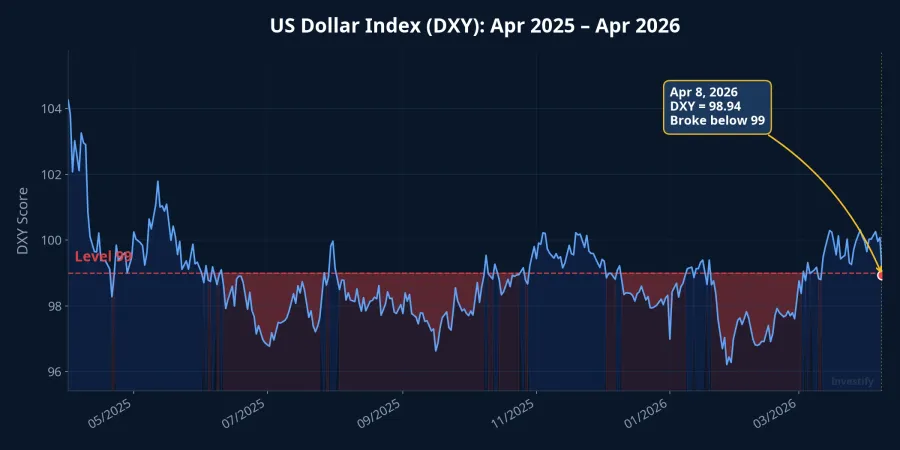

DXY Breaks Below 99: An Unusual Signal

For the past three decades, every time a crisis erupted, global investors shared one reflex: buy US dollars. From the 1997 Asian financial crisis, the 9/11 attacks, to the COVID-19 pandemic, the DXY index always surged during every episode of panic. But in April 2026, the script has flipped entirely.

On April 8, DXY plunged 1.14% in a single session, dropping to 98.94 points, breaking below the psychological 99 level and hitting a four-week low.Prokerala The surprising part: this weakness occurred while US-Iran tensions had only temporarily eased, and the global trade war continued to escalate.

In a longer context, the story is even more striking. From its peak of 108.32 in February 2025, DXY has lost 8.7% of its value as of April 8, 2026. Compared to the same date last year (102.90 on April 9, 2025), the index declined 3.8%. This is not short-term volatility; it is a structural trend.

Three Reasons the Greenback Is Losing Momentum

US-Iran Ceasefire Reduces Safe-Haven Demand

On April 8, President Trump announced a two-week postponement of threatened strikes on Iranian civilian infrastructure, in exchange for Iran reopening the Strait of Hormuz.WhalesBook Oil prices dropped sharply, inflation fears cooled, and the market began pricing in the possibility of Fed rate cuts this year. Safe-haven flows into USD reversed rapidly.

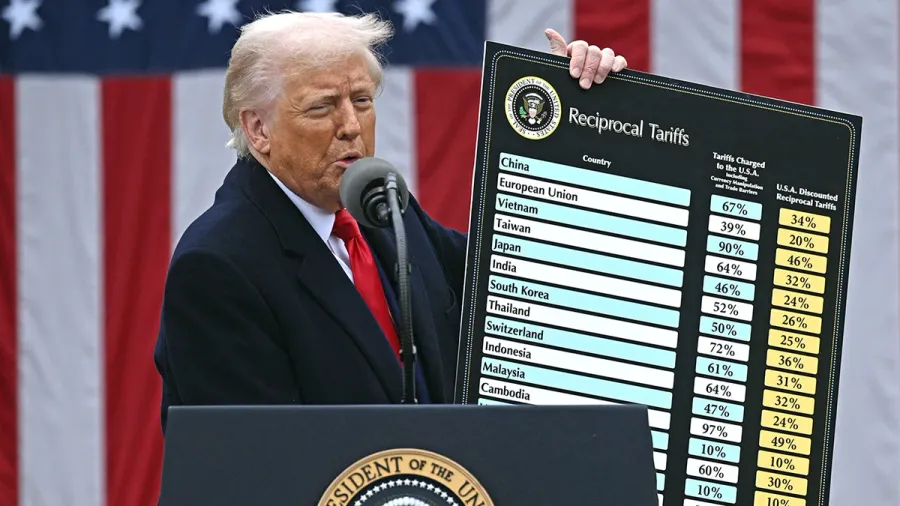

The "Sell America" Trade After One Year of Tariffs

One year after "Liberation Day," when President Trump imposed sweeping tariffs on dozens of countries in April 2025, global investors are repricing US assets.CNBC Average US tariff rates surged from below 3% to nearly 17%, equivalent to an additional $1,500 in taxes per American household in 2026.Tax Foundation

The consequence is clear: the Shanghai Composite, Korea's Kospi, and Japan's Nikkei have all outperformed the three major Wall Street indices since Liberation Day. Capital is leaving the US and flowing toward Europe, Asia, and emerging markets.

Rising Expectations for Fed Rate Cuts

As inflation cools thanks to falling oil prices, the market is increasingly pricing in Fed rate cuts. Lower interest rates erode the yield advantage of USD-denominated assets, pushing capital toward markets with higher growth potential. However, the March Fed minutes show 7 out of 19 officials still favor holding rates steady for all of 2026, so this remains far from certain.

Where Does Money Flow When the Dollar Weakens?

History shows that every period of USD weakness is typically accompanied by three distinct trends. First, gold surges: XAU/USD is trading around $4,722 per ounce as of April 9, 2026, up more than 50% year-over-year.TradingNews J.P. Morgan forecasts gold will average $5,055 per ounce in Q4 2026.J.P. Morgan In Vietnam, SJC gold bars traded at VND 175 million per tael on April 8, up VND 2.5 million from the previous session.

Second, Asian currencies strengthen. EUR/USD hit 1.17 on April 8, up 1.29% in a single session. Meanwhile, USD/VND remained stable around VND 26,335, showing that the State Bank of Vietnam maintains firm control over exchange rate fluctuations.

Third, and most important for Vietnamese investors: capital flows into emerging markets. When the USD weakens, the opportunity cost of investing outside the US decreases. Global investment funds begin reallocating capital toward markets with compelling growth stories.

FTSE Upgrade Meets Dollar Weakness: A Dual Catalyst

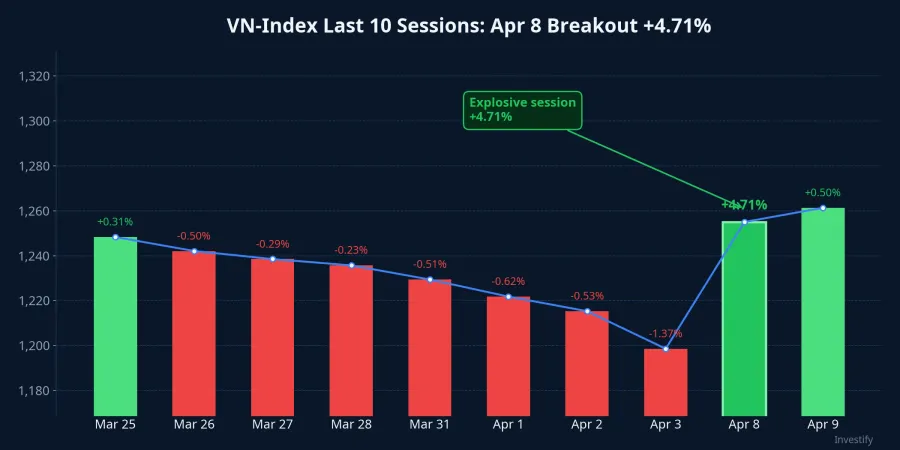

On April 8, 2026, FTSE Russell officially confirmed Vietnam's upgrade to Secondary Emerging Market status, effective September 21, 2026.CNBC The inclusion process will be split into four tranches extending through 2027, with 32 stocks qualifying. SSI Research estimates passive inflows from global ETFs tracking FTSE Emerging Markets at approximately $1.67 billion, while HSBC estimates total flows (passive + active) could reach $3.4 to $10.4 billion.The InvestorVietnamNet

The market reacted immediately: on April 8, the VN-Index surged 79 points (+4.71%) to 1,756.55 points, the strongest gain since the start of 2026, with turnover exceeding 1.23 billion shares. 297 stocks advanced versus only 25 decliners. The following session (April 9), the VN-Index cooled by 19.87 points (-1.13%) to 1,736.68, a perfectly normal correction after a record-breaking rally.

When the USD weakens simultaneously with Vietnam's upgrade, the two forces create a powerful resonance effect. The FTSE pull force compels passive funds to buy Vietnamese stocks to match the index, while active funds also increase allocations for reputational reasons. At the same time, the weak USD push force drives capital away from the US in search of new destinations; a newly upgraded emerging market with stable exchange rates is an ideal choice. USD/VND hovering around VND 26,335, barely moving despite the sharp DXY decline, helps reduce currency risk for foreign investors entering Vietnam.

Holding USD? Time to Reconsider

Many Vietnamese investors still maintain the habit of holding a portion of their assets in USD as a defensive play. But with the DXY down 8.7% from its February 2025 peak, this strategy is being seriously challenged.

A quick comparison of investment channels in early April 2026: SJC gold rose approximately 1.3% in just the first two weeks of April; the VN-Index jumped 4.71% in a single session on April 8; while USD deposits in Vietnam yield near 0% per the State Bank's regulations, plus added exchange rate risk if VND continues to strengthen. The greenback is not always the best hedge. When the dollar loses momentum, investors may consider diversifying into gold, stocks with strong fundamentals in the FTSE basket, or fixed-income products to optimize the stable portion of their portfolio.

Risks to Watch Closely

Despite the positive outlook, shifting capital flows do not mean there are no counter-currents.

The US-Iran ceasefire lasts only two weeks: if negotiations collapse, oil prices could surge again, reversing rate-cut expectations and supporting a USD recovery. This is the largest and most immediate risk in the near term. Additionally, Q1/2026 data shows foreign investors still net sold approximately $1.1 billion in the Vietnamese market despite the FTSE expectation; real capital inflows will only arrive when the upgrade officially takes effect in September.

The Fed has also not committed to cutting rates: the March minutes show 7 out of 19 officials want to hold rates steady for the entire year. And domestically, the State Bank of Vietnam just conducted its largest liquidity absorption in over two years, signaling that the central bank does not want excess liquidity flooding the system before foreign capital actually arrives.

Conclusion: A Historic Opportunity That Demands Vigilance

The weakening of the US dollar amid geopolitical tensions is an unusual signal, reflecting a profound shift in how global investors perceive American assets. The "Sell America" trend is no longer a short-term story but is becoming a structural flow, especially after Trump's tariff policies shook confidence in US economic stability.

For Vietnam, this is a rare opportunity: the FTSE upgrade creates a mandatory pull force, a weakening USD creates a natural push force, and stable exchange rates provide a safe foundation. These three converging factors create one of the most favorable backdrops for foreign capital inflows into Vietnam since the stock market's inception. However, opportunity always comes with risk. Investors should closely monitor the US-Iran ceasefire developments, signals from the Fed, and actual foreign capital flows, rather than simply chasing expectations.