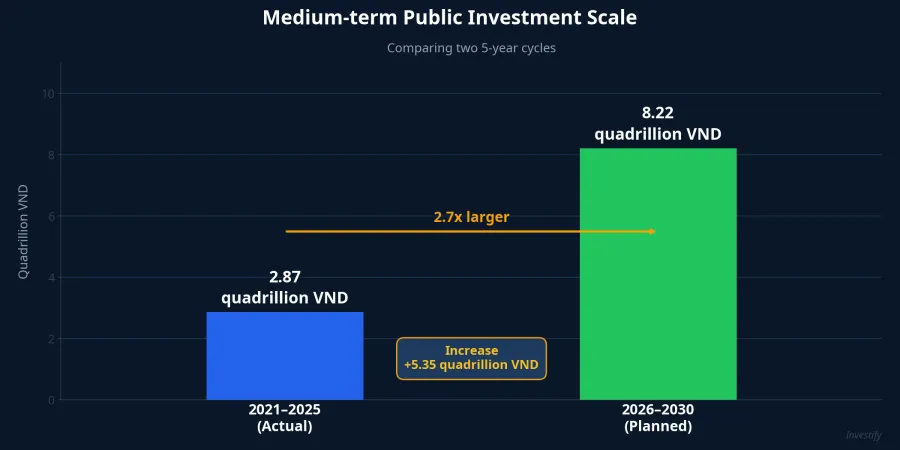

On the afternoon of April 9, 2026, Minister of Finance Ngo Van Tuan, on behalf of the Prime Minister, presented the National Assembly with the Medium-term Public Investment Plan for 2026-2030, proposing a total of 8.22 quadrillion VND — 2.7 times the previous five-year execution.VnExpress This is the largest public investment program in Vietnam's history.

Looking at the numbers, the real question isn't "which group benefits." The correct question is: which group benefits in fundamentals, and which is merely trading on expectations? VN-Index closed today down 19.87 points at 1,736.68, yet a cluster of public investment stocks rallied against the tide. A single-session reaction is never a reliable signal, so I placed the two-day announcement performance next to the three-month trailing return — and the data tells a story very different from the one on the ticker boards.

How is 8.22 quadrillion VND allocated

According to the report submitted to the National Assembly, the proposed capital structure includes 3.8 quadrillion VND from the central budget, 4.22 quadrillion from local budgets, plus a general reserve of about 10%.Tap Chi Kinh Te Tai Chinh The disbursement target is set above 95% of assigned capital, while reducing the number of projects by roughly 30% compared with the previous period to concentrate resources on large-scale works.

The allocation focuses on three axes: transportation (a 5,000 km expressway target by 2030, the North-South high-speed railway, Hanoi and HCMC metros), energy (transmission grid, renewable absorption infrastructure), and urban infrastructure (ring roads, Long Thanh Airport Phase 2).

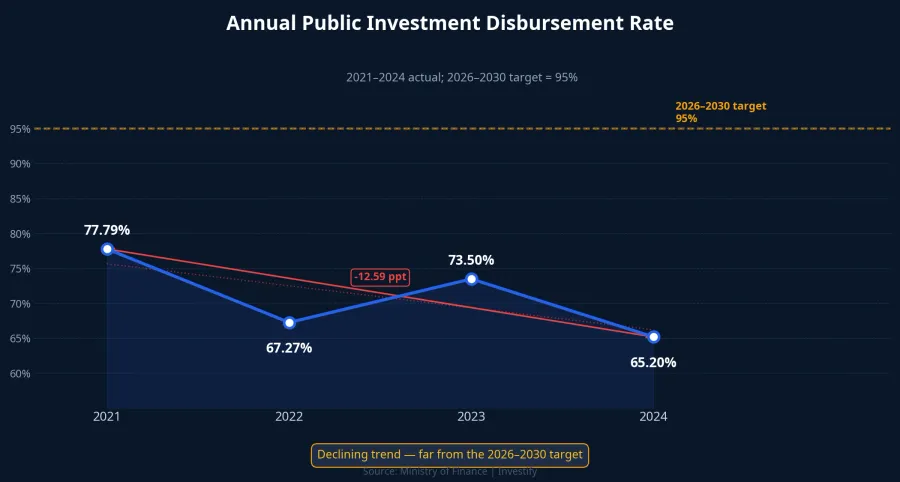

The disbursement lesson: Planned isn't delivered

This is the point investors routinely miss when chasing headlines. In the previous cycle, the disbursement rate was approximately 77.79% in 2021, then slipped to 67.27% in 2022,Bao Chinh Phu recovered to 73.5% in 2023,Bao Chinh Phu and dropped to just 65.2% of the Prime Minister's assigned plan in 2024.VCCI Total public investment capital for the entire 2021-2025 period reached about 2.87 quadrillion VND — significantly below the original plan.Ministry of Finance

What stands out in four years of data is that the trend is not rising; it is falling. The 95% target for the new cycle sits nearly 30 percentage points above the 2024 reality. The amended Public Investment Law, Land Law, and PPP Law (2024-2025) are expected to ease bottlenecks in land clearance and investor capacity, but it will take another 6-12 months before results become visible. The implication for investors is concrete: 8.22 quadrillion VND is a planning ceiling, not an execution floor. Valuing stocks on the assumption of full disbursement would be dangerous.

Three stock groups, three very different reactions

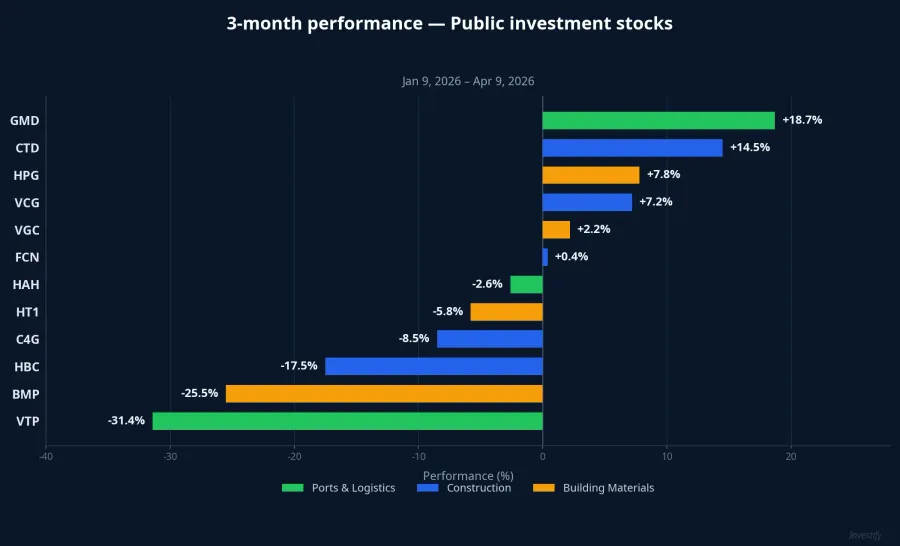

To separate "real beneficiaries" from "story beneficiaries," I placed the two-session reaction on April 8-9 against the three-month trailing return from early January 2026.

Infrastructure construction is the most news-sensitive group. VCG rose 3.37% on April 9 to 23,000 VND on top of a 4.22% gain the day before, and is up 7.2% over three months. CTD closed April 9 at 82,900 VND, and more importantly its three-month return reached +14.5% — the highest in the construction group. By contrast, FCN jumped 4.51% on April 9 to 13,900 VND but is nearly flat over three months (+0.4%); C4G hit the ceiling two sessions in a row yet is still down 8.5% over three months; HBC has lost 17.5% year-to-date. The distinction is clear: names with real backlog like CTD and VCG trend up; highly leveraged small caps merely bounce on news.

Building materials reacts more slowly, and with a narrower range. HPG rose 0.89% on April 9 to 28,250 VND, up 4.48% on April 8, and +7.8% over three months. With a market cap of 216.8 trillion VND, HPG is the only name in the group large enough to capitalize on a nationwide construction cycle. HT1 (cement) gained 2.98% on April 9 but is down 5.8% over three months. BMP (plastic pipes) fell 2.10% on April 9 despite hitting a record 6.99% gain on April 8, and has lost 25.5% over three months. VGC is nearly flat at +2.2%. The honest reading: the public investment narrative is not strong enough to reverse the commodity-cycle pressure weighing on HT1, BMP, and VGC.

Logistics is the group where the three-month number says the opposite of the two-session number. GMD fell 1.21% on April 9 to 73,600 VND, HAH slipped 1.60% to 55,500, VTP dropped 1.74% to 73,500 — no limit-ups, no fireworks. But extending the window to three months, GMD is up +18.7% (from 62,000 to 73,600), making it the top performer across all 12 public-investment stocks I track. Market cap of 31.4 trillion VND, low leverage, stable port business model. Conversely, VTP has lost 31.4% over three months — a reminder that the "public investment beneficiary" label cannot save a stock when its own corporate story is going the wrong way.

Four risks that could deflate the rally

The performance chart points to four things investors should watch in the coming quarters. First, disbursement pace: if 2026 stays below 70% as in 2024, expectations will cool quickly. Second, raw material prices: construction has thin margins, and a steel or oil price shock can vaporize profits even with a strong backlog, as HBC experienced in 2021-2022. Third, interest rates: 12-month deposit rates of 7-8% at smaller banks mean higher cost of capital for construction firms, with highly leveraged names (FCN, HBC, C4G) hit hardest. Fourth, money rotation once the news is out — this is exactly the scenario construction small caps typically run into.

Conclusion: Choose by time frame, not by headline

The numbers tell a clear story. Over 1-3 months, infrastructure construction reacts first — prefer CTD and VCG with real backlog; avoid chasing C4G, FCN, HBC on news alone. Over 6-18 months, HPG stands out thanks to its scale and ability to ride a nationwide construction cycle. Over 2-5 years, GMD is the most durable story with its port positioning and low leverage, fitting the logic that "as infrastructure completes, cargo volumes follow."

The biggest lesson from the 2021-2025 cycle still holds: a large plan doesn't translate into an immediate rally, and not every stock that hits the ceiling can hold those levels three months later. With 8.22 quadrillion VND stretched across five years, this isn't a sprint. It's a marathon, and three months of data is already enough to tell the long-distance runners from the news chasers.