The big picture reveals a textbook commodity cycle unfolding before our eyes: global coffee prices have tumbled from historic highs to an 8-month low, while Vietnam — the world's largest robusta producer — confronts the painful paradox of exporting more but earning less.

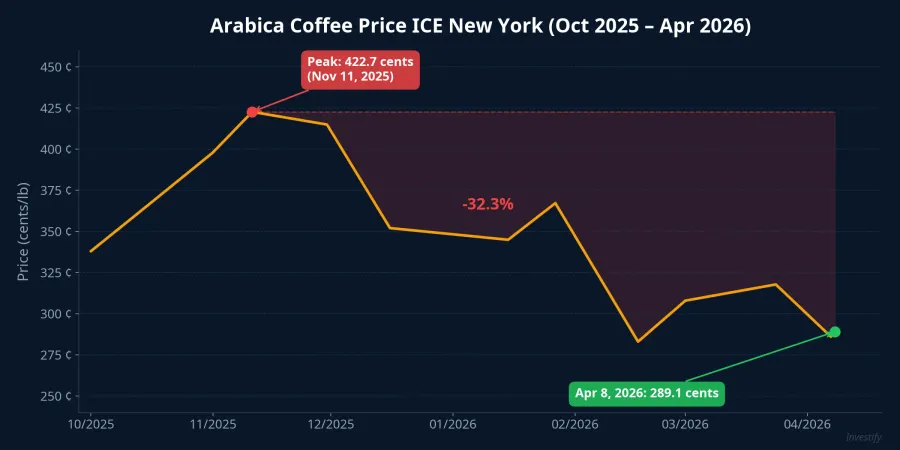

From 422 cents to 289 cents: five months of value erosion

On April 8, 2026, domestic coffee prices in Vietnam's Central Highlands dropped 4,000 VND/kg in a single session, falling to 84,700–85,300 VND/kg.VOV Meanwhile, London robusta May 2026 futures lost 133 USD/ton (-3.85%), sliding to 3,315 USD/ton — an 8-month low.NLD

But this was no surprise selloff. Capital has been rotating out of coffee since the historic peak in late 2025. Arabica on ICE New York reached 422.70 US cents/lb on November 11, 2025 — its highest level in years. By April 8, 2026, the price had fallen to 289.13 US cents/lb, a roughly 32.3% decline in just five months.

The price path was not a straight line down. After dropping sharply from the 422.70-cent peak to 352.10 cents by mid-December 2025, a technical bounce lifted prices to 367.25 cents by late January 2026. However, selling pressure quickly returned, pushing arabica to a trough of 283.10 cents in mid-February. Another relief rally to 317.85 cents in late March — driven by a stronger Brazilian real — also failed to reverse the overall downtrend.

Brazil forecasts a record crop: the source of oversupply pressure

The root cause lies in the production outlook for Brazil's 2026/27 coffee season. Since early 2026, international forecasters have released one record estimate after another:

- Conab (Brazil's official crop agency): production expected at 66.2 million bags, up 17.2% from the prior season.Thời báo TCVN

- Marex Group: forecast as high as 75.9 million bags.StockPil

- StoneX: estimated at 70.7 million bags, up 13.5%.HedgePoint

At the global level, Rabobank — the world's leading agricultural bank — forecasts total world coffee production to hit a record 180 million bags in the 2026/27 season, up approximately 8 million bags year-on-year. More significantly, the market is expected to see a surplus of 7–10 million bags — the largest in many years.Nasdaq

The key driver is above-average rainfall in the Minas Gerais growing region, which has erased drought concerns from the previous two years. Additionally, the 2026/27 season coincides with the arabica "on-year" — a natural high-yield cycle, with Brazil's arabica output projected to rise 23–29% depending on the forecast source.

Vietnam's paradox: selling more, earning less

This is the most painful — and most instructive — aspect for Vietnam's coffee industry. Q1/2026 export data reveals a stark paradox: volume up, revenue down.

Specifically, Vietnam exported 577,300 tons of coffee in Q1/2026, a 12.6% increase from Q1/2025. Yet revenue reached only 2.71 billion USD, down 6.4%.Vietnam.vn The average export price fell to 4,696.8 USD/ton, a 16.9% year-on-year decline.Xaluan News

Put simply, every ton of Vietnamese coffee sold on the world market brought in nearly one-fifth less revenue than a year ago. Central Highland farmers shipped more, traders transported more, but the cash flowing back was thinner. Key export destinations remain Germany (16.4% market share), Italy (8.6%), and Spain (7.6%), with shipments to Italy showing signs of decline.Vietnam.vn

Central Highland farmers: shrinking profit margins

In the Central Highlands — the growing region responsible for over 90% of Vietnam's coffee output — farmgate prices hovered around 84,700–85,300 VND/kg.VOV Compared to the 130,000+ VND/kg seen during the late-2025 peak, farmers have lost approximately 35% of their per-kilogram income.

With average production costs of 40,000–50,000 VND/kg, current prices still ensure a positive margin. However, profitability has narrowed sharply from the "black gold" era of late last year. The greatest pressure falls on households that borrowed to expand planting area when prices were at their peak; their cash flows are now under reverse pressure as prices have fallen faster than expected.

Coffee stocks: a dead end for investors

Unlike oil or steel, Vietnam's coffee sector has very few listed companies of meaningful size. VCF (Vinacafé Biên Hòa) is the sector's largest stock at 300,000 VND per share with a market cap of roughly 8,000 billion VND, but it focuses on instant coffee and is therefore less directly exposed to raw material price swings. Pure-play names like CFV (21,000 VND) and CPA (9,000 VND) have market caps under 300 billion VND and near-zero liquidity.

In practice, while global coffee prices swing dramatically, Vietnam-listed coffee stocks barely react due to thin liquidity and low free floats. Investors seeking to play the coffee theme through Vietnamese equities essentially have no liquid options.

H2/2026 outlook: oversupply pressure persists

According to Rabobank, arabica could trade in the 250–300 US cents/lb range in the second half of 2026, significantly below the 350+ cents/lb average seen in 2025.Nasdaq

Four factors to watch closely in the coming months: Brazil's harvest progress (favorable weather could push actual output above even the most bullish forecasts); ICE inventory trends (already at a 3.5-month high); the Brazilian real exchange rate (a weaker real would incentivize Brazilian farmers to sell more); and weather risks (El Niño or unexpected drought in Brazil or Vietnam is the only factor that could reverse the downtrend).

For Vietnam, the goal of exceeding 8 billion USD in coffee exports for 2026 faces major headwinds as average selling prices have dropped sharply.Sở CT Đồng Nai The most likely scenario is continued volume growth driven by abundant robusta supply, but revenue may fall short of targets unless prices recover.

Lessons from the commodity cycle

The coffee price story of 2025–2026 is a textbook illustration of commodity market dynamics: high prices stimulate investment in expanded production, output surges create oversupply, and prices reverse sharply. Vietnam's position as the world's number-one robusta producer grants market-share advantages but also means complete dependence on world prices.

The bigger question for Vietnam's coffee industry remains unanswered: when will the country develop enough deep-processing capacity to escape the cycle of "selling more, earning less"? While awaiting that answer, investors should track London robusta prices and Brazil's harvest progress as the two most critical indicators.