The big picture reveals a rare paradox: the stock market delivered its strongest rally of the year, while behind the scenes, systemic liquidity is stretched to the limit. The trading session on April 8, 2026 will go down in history with a 79.01-point surge (+4.71%), pushing the VN-Index to 1,756.55 points. But behind the euphoria, the State Bank of Vietnam (SBV) is grappling with a difficult equation: controlling inflation and the exchange rate without choking off capital flows into the market.

A Historic Session: Two Catalysts at Once

On the afternoon of April 8, the VN-Index exploded with 331 stocks advancing, 24 hitting the ceiling, and only 31 declining. Trading volume hit a record with over 1.23 billion shares exchanged, valued at more than VND 33,000 billion.Tiền Phong

The twin catalysts were unmistakable: FTSE Russell officially confirmed Vietnam's upgrade path to Secondary Emerging Market status effective September 21, 2026, and a 2-week ceasefire between the US and Iran eased Brent crude prices.VietnamNet These were the two catalysts the market had been waiting months for, creating the most powerful rally since the beginning of the year.

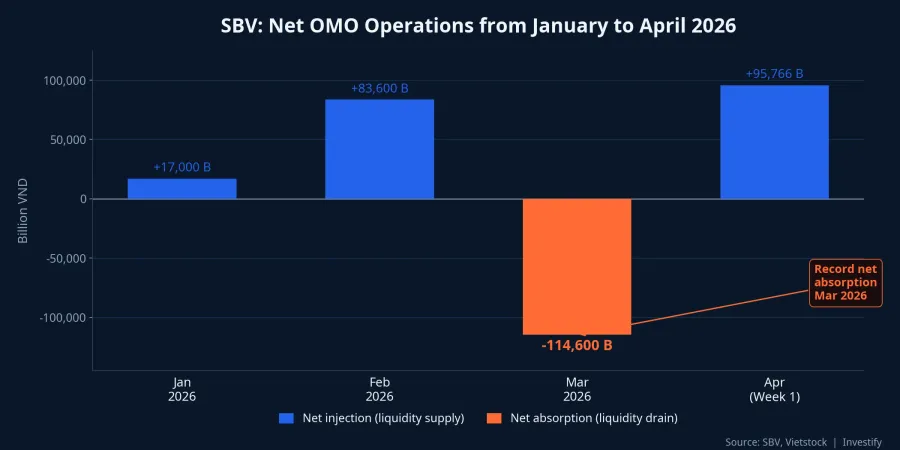

Behind the Scenes: SBV Drains 114,600 Billion in March

While investors celebrated, the SBV quietly executed its largest liquidity drain in over 2 years. In March 2026, the SBV absorbed approximately VND 114,600 billion net through open market operations (OMO).VietnamBiz

Specifically, the SBV injected nearly VND 491,300 billion through OMO channels at 7–56 day tenors with a fixed rate of 4.5%, but maturing OMO volumes reached over VND 605,800 billion. The result: outstanding OMO balances in the system dropped to approximately VND 290,000 billion, down 41% from the peak established in early February.VietnamBiz In the week of March 9–13 alone, the SBV absorbed VND 81,500 billion in a single week.Vietstock

Overnight Rates Spike to Double Digits

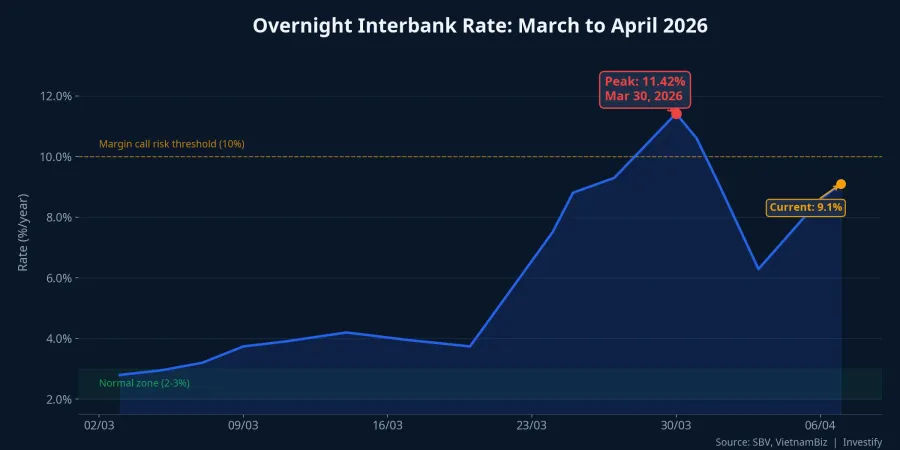

Capital flows are shifting dramatically within the interbank system. When liquidity was rapidly withdrawn, the overnight rate — the most sensitive gauge of systemic liquidity — surged to 11.42% on March 30, nearly 5 times the average 2–3% level of the preceding period.Vietstock

The SBV had to reverse course and inject VND 95,766 billion net during the week of March 30–April 6 to ease the shock, bringing outstanding OMO balances up to approximately VND 301,405 billion. However, the overnight rate remained elevated at 8.6–9.1% in early April, 3–4 times the normal range.VietTimes

The deeper cause: credit has overwhelmed deposits. As of late March 2026, deposit growth stood at just 0.1% compared to year-end 2025, while credit growth reached 1.5%. This mismatch pushed the loan-to-deposit ratio (LDR) at many banks above the 100% threshold.VnBusiness

Three Reasons the SBV Had to Tighten

Inflation Breaches the Target Ceiling

March 2026 CPI surged to 4.65% YoY, the highest since January 2023. For context: January 2026 CPI was just 2.53%, February was 3.35%. In just 3 months, inflation nearly doubled. The transportation group contributed the most with a 12.85% YoY increase, reflecting the direct impact of fuel prices. Core CPI also climbed to approximately 3.96%, indicating that inflation is spreading into basic consumer goods, not just energy-driven.

With CPI far exceeding the 4–4.5% ceiling set by the National Assembly, the SBV has virtually no room to maintain an accommodative stance.

Persistent Exchange Rate Pressure

The USD/VND rate rose from 26,102 dong (February 25) to 26,334 dong (April 7), equivalent to roughly 0.89% appreciation in less than 6 weeks. While not extreme, this occurred against the backdrop of the Fed maintaining a hawkish stance, with a senior Fed official even mentioning the possibility of raising rates again. As the VND-USD interest rate differential narrows, capital outflow pressure intensifies. The SBV needs to keep VND rates attractive enough to defend the exchange rate, and draining liquidity is one of the most effective tools.

Leverage Risk in the Stock Market

With the VN-Index jumping from 1,645 points (March 26) to 1,756.55 points (April 8) — a 6.8% gain in less than 2 trading weeks — margin debt across the market remains at elevated levels. The margin-to-equity ratio at several major brokerages including HSC, Mirae Asset, MBS, and KBSV is approaching maximum limits.CafeF When interbank rates rise, funding costs for brokerages increase, forcing them to either raise margin rates or tighten lending limits.

The Transmission Mechanism: From SBV to Your Margin Account

The chain reaction follows a clear sequence: SBV net absorption → systemic liquidity drops → interbank rates rise → brokerage funding costs increase → margin rates rise or limits tighten → capital flowing into the stock market decreases → forced selling pressure if the market corrects.

When the overnight rate exceeds 6–8%, brokerage funding costs start generating losses if margin rates remain unchanged. When rates exceeded 10–12% as in late March, many brokerages were forced to reduce disbursements or shrink limits. Every small shift in funding costs can amplify into significant selling pressure on the exchange, particularly among mid-cap and penny stocks that depend heavily on speculative capital flows.

The SBV's Dilemma: Tighten or Ease?

Recognizing the excessive pressure, the SBV reversed course and injected VND 95,766 billion net during the week of March 30–April 6.Vietstock However, rates have not fully normalized. This sends an important signal: the SBV is trying to balance two conflicting objectives. Controlling inflation and stabilizing the exchange rate demands tighter liquidity; maintaining systemic stability demands injections. There is no perfect solution to this equation.

The last time something similar occurred at this scale was late 2022, when the SBV raised policy rates from 4% to 6% and aggressively tightened liquidity to defend the exchange rate. The VN-Index fell from around 1,200 to below 1,000 points in Q4 2022.

What Should Investors Watch?

Three key thresholds to monitor weekly: the overnight rate (normal zone 2–3%, warning above 6%, margin call risk above 10%); weekly net OMO (if the SBV resumes net absorption after the early April injection, that signals further tightening); and April CPI (if it remains above 4%, the SBV will have little room to ease).

In terms of specific actions, investors should keep margin utilization below 50% of available room to avoid unexpected margin calls when borrowing costs rise. Prioritize stocks with strong fundamentals and high liquidity, as mid-cap and penny stocks will face the most pressure when speculative capital contracts. Maintain a higher-than-normal cash allocation: the market may continue rising on FTSE momentum, but volatility will increase while systemic liquidity remains unstable.

Conclusion

The +79-point rally is a well-deserved reward after years of waiting for the FTSE upgrade. However, behind the scenes, the SBV is facing a triple challenge of 4.65% inflation, exchange rate pressure, and a banking system stretched on liquidity. The 114,600 billion dong net drain in March — the largest in over 2 years — was no accident: it was a necessary policy response to an overheating economy.

The VN-Index rally may continue on foreign capital expectations from FTSE, but the liquidity foundation underneath is thinner than most investors realize. Smart investors will look not only at the price chart, but also at where the real money is actually flowing.