The big picture shows that the April 8 session was far more than just a strong rally day. Behind the impressive +79-point VN-Index gain lie two fundamentally different forces: structural ETF capital flows driven by the FTSE Russell upgrade roadmap on one side, and a tactical reaction to the US-Iran ceasefire on the other. Investors who fail to distinguish these two currents risk making costly mistakes when deciding whether to hold or take profits.

April 8 Session: Every Metric Exploded

VN-Index closed at 1,756.55 points, up 79.01 points or 4.71% from the previous session. The exchange recorded 331 advancing stocks versus just 31 decliners, with 24 hitting the ceiling and only 2 hitting the floor. Trading volume exceeded 1.25 billion shares, signaling massive capital inflows.

Compared to the April 2 session, VN-Index rallied 61.73 points over just 4 trading sessions, a 3.64% gain from the 1,694.82 level. This marked the fastest recovery streak since the start of 2026.

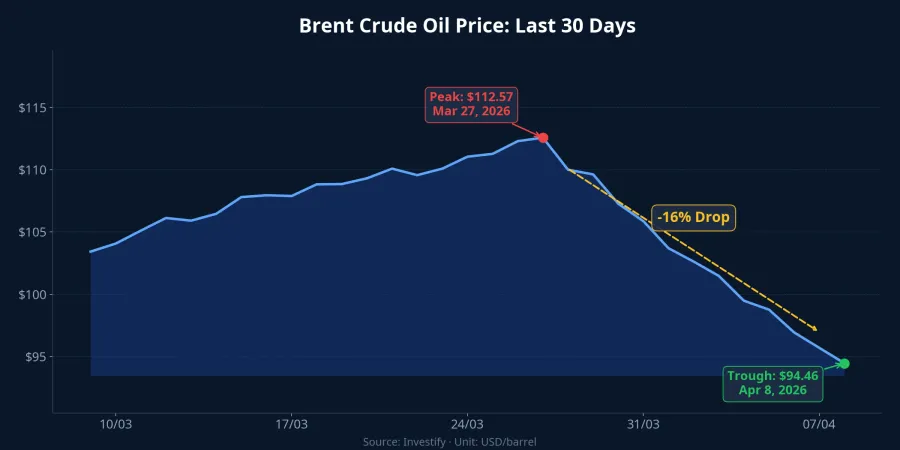

Two major events converged to produce this surge. First, FTSE Russell officially confirmed Vietnam's upgrade to Secondary Emerging Market status, effective September 21, 2026, after 8 years on the watchlist.The Investor Second, Iran confirmed a 2-week ceasefire with the US, sending Brent crude plunging from $109.27 to $94.46 per barrel, a 13.56% single-session drop.PLO

The critical question: which stocks rallied for which reason?

Structural Group: 28 Stocks Benefiting from FTSE ETF Flows

FTSE Russell confirmed Vietnam's upgrade from Frontier to Secondary Emerging Market through a 4-phase roadmap extending to September 2027.The Investor Phase 1 begins in September 2026 with Vietnam's initial inclusion in the FTSE Emerging Index, followed by weight increases based on liquidity assessments (March 2027), expansion into GEIS component indices (June 2027), and full 100% official weighting by September 2027.

Capital flows are shifting along a locked-in roadmap. According to reports from Mirae Asset and BSC, Vietnam will account for approximately 0.22% of the FTSE Emerging Index, translating to passive capital inflows of $500 million to over $850 million disbursed across 4 tranches.Vietnam News This is "mandatory" capital: ETFs tracking the FTSE index must buy according to assigned weights, regardless of market conditions.

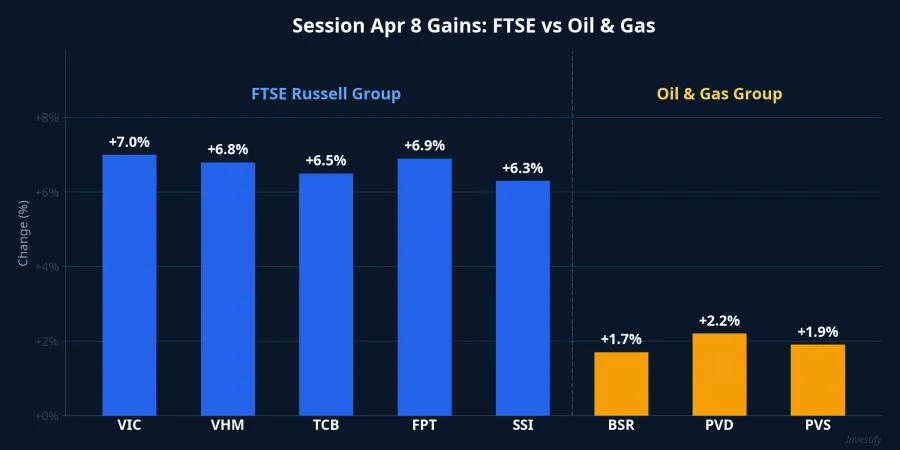

FTSE Russell has identified 28 stocks likely to enter the FTSE Global All Cap Index, including VCB, VIC, VHM, HPG, FPT, MSN, SAB, and VNM.Vietnam News On April 8, this group led the rally: VIC (+6.97%), VHM (+6.96%), TCB (+6.97%), FPT (+6.89%), and PNJ (+7.00%) all hit or nearly hit the ceiling; VCB (+3.79%), HPG (+4.48%), and MBB (+3.91%) posted strong gains as well.

The key point: passive ETF flows do not depend on short-term news. Whether US-Iran negotiations succeed or fail, whether oil rises or falls, these funds must disburse according to their 4-tranche schedule starting September 2026. Once Vietnam is officially in the index, capital arrives on schedule, not on sentiment.

Tactical Group: Reacting to Oil's Ceasefire-Driven Decline

A 2-Week Ceasefire, Not Peace

Iran confirmed a 2-week ceasefire agreement with the US, brokered by Pakistan.Nhan Dan Formal negotiations are scheduled to begin April 10 in Islamabad.Mekong ASEAN However, just days earlier (April 3-6), talks had stalled when Iran refused to meet US officials.Bao Quoc Te The negotiations cover extremely complex issues: control of the Strait of Hormuz, uranium enrichment programs, and sanctions relief. The likelihood of a comprehensive deal within 2 weeks is very low.

Oil's Sharp but Fragile Reaction

Brent crude dropped from $109.27 to $94.46 per barrel on April 8, a $14.81 or 13.56% decline. Looking broader, Brent had peaked at $112.57 on March 27, meaning it fell a total of 16.09% in under 2 weeks. But history shows that every time negotiations break down, oil snaps back sharply — on April 2, Brent surged 7.78% in a single day.

Airlines Benefit, Oil & Gas Merely Bounced

Airlines benefited most from falling oil: HVN rose 6.07% to VND 22,700 (fuel costs account for 30-40% of operating expenses), while VJC gained 2.51% to VND 167,600. Meanwhile, oil & gas stocks posted only modest gains alongside the market: BSR (+2.19%), PVD (+1.71%), PVS (+2.14%). The 1.7-2.2% gain range is far below the FTSE group's 6-7%, and was essentially a technical recovery after sharp prior-session declines (PVS fell 6.44% on April 6, BSR dropped 4.74% on April 6).

The market clearly recognized that falling oil prices do not benefit oil & gas stocks. BSR, PVD, and PVS all depend on elevated oil prices for healthy profit margins.

Warning Signal from Foreign Investors

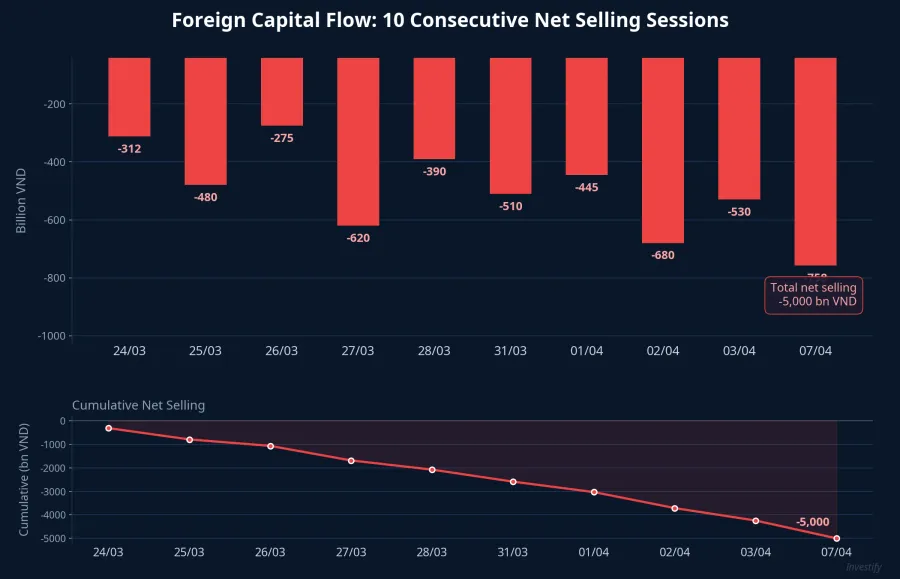

Despite VN-Index surging nearly 80 points, foreign investors still net-sold approximately VND 592 billion on April 8, extending their selling streak to 4 consecutive sessions. Over the past month, foreign investors have net-sold over VND 12,489 billion, averaging VND 543 billion per session.

This reveals an important truth: passive ETF flows tied to the FTSE upgrade have not yet begun disbursing — they won't start until September 2026 per the roadmap. Current foreign investors are taking profits and rebalancing portfolios ahead of the upgrade event, not buying in. This is a critical signal that retail investors should carefully consider when evaluating the real strength of this rally.

Two Scenarios Ahead

The outcome of Islamabad negotiations starting April 10 will determine the tactical group's direction.

If negotiations progress positively, oil could decline further to the $85-90 range. Airlines (HVN, VJC) continue benefiting, while oil & gas stocks (BSR, PVD, PVS) face deeper pressure. The FTSE group remains unaffected and maintains its structural uptrend.

If negotiations fail and tensions re-escalate, oil could snap back above $110 per barrel (as on April 2 when Brent surged 7.78% in one day). Airlines lose all ceasefire-driven gains. Oil & gas recovers but with limited upside. The FTSE group continues to be supported by long-term ETF flows.

Regardless of which scenario unfolds, the FTSE group holds a decisive advantage thanks to its long-term structural catalyst.

Distinguish Clearly, Act Wisely

The April 8 session was memorable, but not every ceiling-hitting stock rallied for the same reason. FTSE upgrade beneficiaries have a long-term capital foundation of $500-850 million to be disbursed from September 2026 across 4 officially confirmed tranches. Stocks rallying on the oil-decline ceasefire narrative are merely reacting to news, and that news could change within days.

Hold the structural group, exercise caution with the tactical group. A simple equation, but amid the euphoria, not everyone maintains the clarity to see it.